LATAM economic growth is expected to regain momentum in 2020. Accelerating investment in Brazil, Chile, Mexico and even Peru is expected. Inflation is easing: Chile´s central bank slashed its benchmark interest rate to 1.75% from 2% on October 23rd, its third major rate cut since June; and Brazil’s central bank cut rates for the third time in as many months. Interestingly, Fintech startups are fueling part of this growth with cross-border investments from both outside and within the region. Huawei, Amazon and Stripe represent some of the former, and Alaya and IOVLAbs represent examples of the latter.

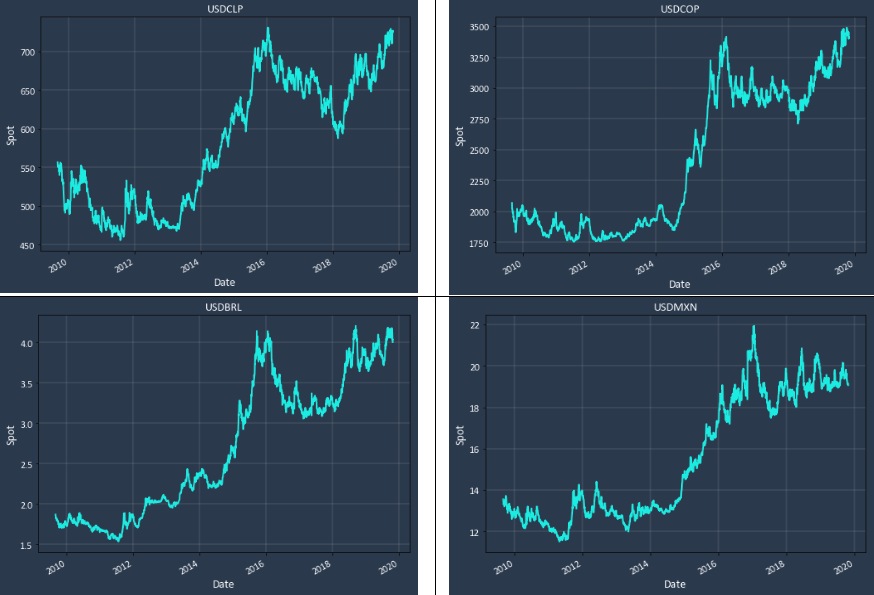

What all of these cross-border investments have in common is currency risk. When an investor or firm acquires an interest in a LATAM entity, the investor's home currency is converted to the local currency. Subsequent growth, revenue and dividends are valued in local currency during the investment period. At the end of the investment term, the value is converted back to the investors home currency. If the spot rate has moved adversely during this period, gains can easily be swamped by currency losses. LATAM currencies are particularly vulnerable to this effect - of the top seven most volatile currencies against the USD, five are LATAM (ARS, COP, BRL, and CLP). Here are the historical spot rates of the most common target investment currencies- they exhibit heightened volatility and trending depreciation:

An investment made with USD into Mexico in 2014 (spot rate 14) and redeemed in 2019 five years later (spot rate 19) has a 35% deficit to make up, reducing ROI by an annualized 6.2%. This high volatility creates significant risk that needs to be managed if investment goals are to be realized.

The classical tools for managing foreign exchange risk are forward contracts. These lock in a future conversion rate, eliminating risk. So far, so good...However, the forward rate is based upon differential interest rates (to prevent arbitrage) . This often means the forward rate is often worse than the current spot rate (3-4%/yr for COP, BRL), but sometimes is a few percent in the hedgers favor (CLP). Thus, picking a hedge ratio is an exercise in optimization.

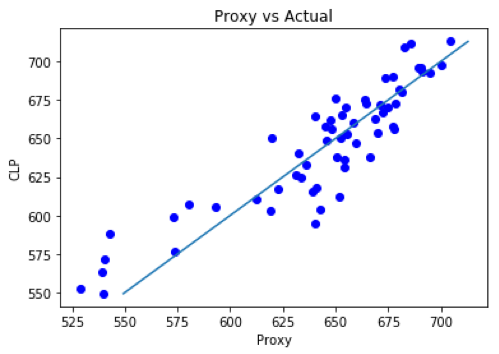

Given the expense of this insurance for some currency pairs, alternatives are sometimes employed. Proxy hedging - the use of a basket of more liquid currency forwards that track the target currency closely -is one common solution. Choosing the basket and the hedge ratios of its components is now done using machine-learning enhanced techniques to avoid the many pitfalls of linear regression.

Forwards are a safe and assured for managing predictable cash flows (dividends, interest rate payments on debt, corporate earnings). What happens if the cash flows are not at all assured? For example, the Uruguayan firm IOVLabs recently announced the acquisition of Taringa, an Argentine social media platform. Usually, during acquisitions, there is a due diligence period which may last 3-6 months. During that time the UYU/ARS spot may (will!) move significantly, representing a large valuation risk. Forwards are not an alternative for deal-contingent hedging because if the deal unwinds, the hedge must as well; and forward contracts are not able to be cancelled.

Options might be a choice if both currencies are liquid/fungible; not exactly the case here. In situations like this, using a basket of currencies that has been selected to minimize volatility between the two target currencies (buyer and seller) may be an alternative. The buyer exchanges the purchase price into the basket of currencies. At the end of the due diligence period the buyer has a choice- they may convert the basket to the seller's currency and complete the deal; OR if the deal has unwound, they can convert back into their home currency. Conversion optionality over a lengthy and uncertain due diligence period can be achieved. Again, machine learning and constrained optimization techniques may be used to select the minimal volatility basket.

Taking advantage of LATAM's accelerating growth and abating inflation makes sense for investors within and outside of the region. Chile, Columbia and Peru all are expecting GDP growth of nearly 3%, and Bolivia nearing 3.7%. However, currency fluctuations pose one of the larger risks to such cross-border investment.

Fortunately, many tools are available to the investor to manage this risk: forward contracts where reasonable, proxy baskets otherwise. Contingent deal risk - always a challenge - is also manageable without going to the expense of options. Advances in algorithms, machine learning and AI have enhanced the ability of hedgers to manage risk and enjoy safe returns from investing in LATAM.

If you would like to learn more about how Deaglo Partners can assist you, then please reach out and set up some time with one of our team today.