Background:

Managing FX risk generated in first world countries is readily effected with a deep and liquid set of hedging alternatives. However, investment funds doing business in emerging markets face a double challenge - emerging market currencies (e.g. BRL, MXN, CLP) are typically more volatile, and hedging instruments are often non-existent or prohibitively expensive. When the risk must be managed, the only choice is to use a proxy.

When hedging currencies, it is very difficult to identify a single currency proxy with a useful level of correlation. When the correlation is poor, the portfolio variance and basis risk will be high. Using a "basket" of three to four proxy currencies can improve performance. However, common practice using linear regression) has produced mediocre results and unnecessary basis risk.

Deaglo has taken a more robust and novel approach. New machine learning algorithms such as Ridge and Bayesian Regression overcome many of the limitations of the traditional approach. They are less sensitive to noise, less likely to over-fit and make the most of available data (through train/test splits and k-fold cross-validation). They are computationally intensive but produce excellent results.

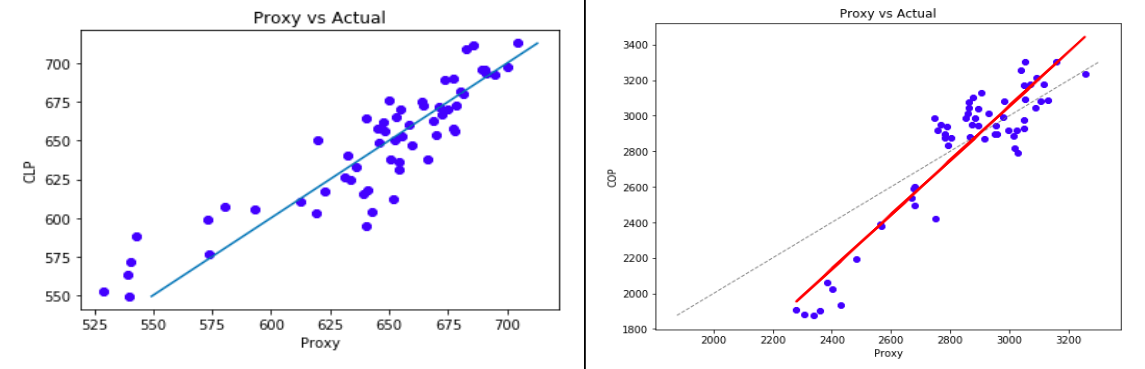

The machine learning approach works very well for numerous EM currencies. Fig 1 shows two examples, hedging USDCLP (Chilean peso) and USDCOP (Columbian peso) with four proxies.

The results are strong- the correlation between both synthetic NDFs and the target asset is above 0.91. Mean errors are in the few percent range.

Operationally, proxy hedging is the creation of a synthetic NDF (non-deliverable forward). An NDF creates a gain or loss in the base currency which offsets any loss or gain between the base currency and the target asset.

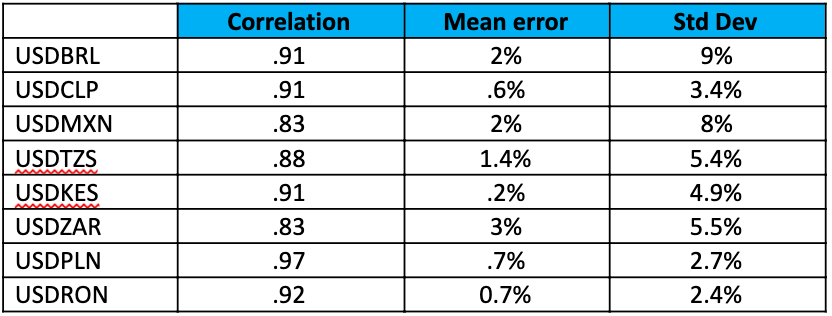

Many different currencies have been tested using this approach, using both Ridge and Bayesian regression. Table 1 shows some highlights of that testing across LATAM, African and eastern European currencies:

Efficacy during market dislocations

When the markets are smoothly functioning, the error is clearly minimal, and basis risk low for many EMs. But what happens when a Lehman Bros happens? The correlations aren't as strong, as each economy reacts differently. However, using data from the period of 2007 to 2012, we found that the mean error is very similar, but the std deviations increased materially, generally by about 50%. This would have the effect of reducing the optimum hedge ratio.

Start hedging what you need to

Proxy hedging is a useful strategy when hedging currencies whose hedging instruments are either unavailable/illiquid, or are prohibitively expensive (forward points). This has prohibited many investments in otherwise lucrative markets.

Deaglo's new EM proxy hedging capabilities can now protect these investments. The results for many EM currencies are excellent - the correlation between the asset and synthetic proxy is high (85% - 95%), and prediction errors are very low (average error 2-3%). This makes the hedging of African, Asian and LATAM currencies practical and affordable.

As always, using a proxy hedge offers no ironclad guarantee of efficacy; there will always be a basis risk. When there is no choice but to use a proxy hedge, our machine-learning enhanced strategy vastly reduces your risk.