It’s a strange time to be a private market fund in an emerging market. A volatile economic situation in the US, where the majority of competitor funds are located, has seen the dollar’s safe haven status thrown into doubt. As a result, a number of emerging market currencies, especially in Latin America (LATAM), have rallied as investors look for alternative markets and opportunities. Despite this, many offshore investors are still wary of the impact currency volatility can have on returns, retreating instead to the perceived comfort of domestic funds and mature markets. This isn’t without good reason, says Matheus Zani, Head of FX Risk Management at Deaglo. “It’s not that fund managers in emerging markets aren’t able to deliver 20 or 30% returns on their investments, it’s that when they’re translated back into dollars or euros, the returns are significantly less. To stay competitive globally, emerging market managers must deliver similar or higher returns to attract investment.”

This isn’t a new problem. Zani wrote a piece in 2020 exploring how LATAM Private Equity (PE) funds were reconsidering how to mitigate currency volatility across the region, with many opting for ‘natural hedges’, i.e. investments where revenues and liabilities don’t present a currency mismatch, or generate USD revenues. Not only is this not particularly effective, it narrows the field of investment opportunity considerably.

Private market funds in LATAM are dealing with a very different landscape today than 2020. South America’s major currencies, the Brazilian real and Colombian peso, have stabilized, inflation is coming under control and the investment markets have matured considerably. But PE investments take a long time to mature, while Venture Capital (VC) backed companies are staying private for longer than ever. This inevitably means that investments often outlast governments and periods of stability or volatility.

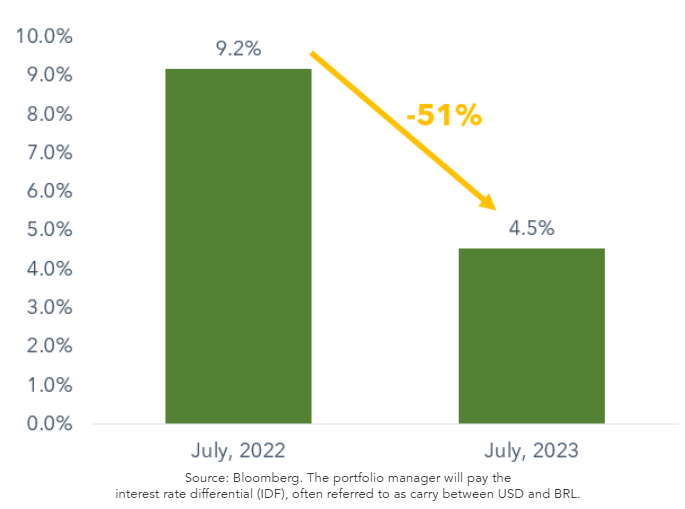

Perhaps in an attempt to make hay when the sun is shining, it’s within this relative stability that some LATAM fund managers are taking action towards hedging. This is made easier, says Zani, as hedging prices have dropped. “The Brazilian and Colombian central banks have reduced interest rates just as the US is increasing its own. This has made hedging much cheaper."

Brazilian Real (USD-BRL)

Concerns around the costs of hedging – and its perceived complexity – have long been a deterrent, especially in LATAM, explains Vagner Perez, Partner at Reinvest, a global-focused firm based in the US. “In Latin America, General Partners (GPs) simply don't address the issue. Either because it's too complicated, too expensive, or too cumbersome. Or they believe that LPs are mature enough to understand the effects of currency, and therefore they should be hedging in themselves."

Reinvest is in its early stages but Perez and his team have already started thinking about hedging. As it will feature a number of multi-currency portfolios, Reinvest is planning to offset the risk by hedging investments against a basket of currencies, likely six or seven to begin with. This approach can be complex, but allows for more accurate hedging.

“We had some internal conversations at Reinvest,” he says, “about what we should say in our pitch to investors. Will returns be in dollars or the local currency or then you can take care of that currency hedging? I strongly believe that we should take on this responsibility.”

This is a trend Zani and the Deaglo team are seeing more frequently. “We’re now seeing LPs of various funds asking fund managers to provide hedged share classes to ensure investments remain insulated from abrupt currency value changes, particularly in the case of long-hold and close-ended funds,” he explains. There are a number of hedging routes that funds can take as well as hedging against a currency basket – a strategy more suited to multi-currency portfolios – such as an overlay strategy which is built around forward options contracts which allow funds to secure favorable exchange rates for a set period of time.

While the goal of many GPs is using hedging as a route to stay attractive to overseas LPs, there are additional benefits, says Perez. In emerging markets, “executing hedging is not common practice among this type of asset class. There will definitely be a competitive advantage for any firm that can do it.” It also opens up more opportunities for investment in a wider geography of funds and companies, especially those that have previously been deemed too risky. “For example, Africa has been getting a lot of attention from investors. But African currencies, as in Latin America, due to political turmoil etc, are volatile,” he explains. Hedging allows investors to “lower their risk perception” and take advantage of all the “interesting opportunities and potential” in the region.

However, perhaps the most important benefit, suggests Perez, is that it allows emerging market funds to offer investors new levels of transparency and trust. “I mean, it's a matter of delivering what is being promised. If GPs are saying that they’re going to be delivering 30% IRR, they cannot then justify a poor performance based on currency risks and currency fluctuations.” If a fund is built around hedged asset classes, the rate of return is based on the fund’s success and nothing else.

This is especially important if VC and PE funds are looking to attract new investors, especially those used to public markets. “For this type of investor, it's paramount to put together a structure that is transparent,” he adds.

Reinvest’s approach, while still relatively rare across many emerging markets, is becoming increasingly popular in LATAM, especially in Brazil and Colombia where a perfect storm of economic stability, forward thinking fund management and sheer market size is creating a template approach for GPs elsewhere, says Zani.

“With a forgiving hedging environment but a tough fundraising one, LPs in other markets should take note.”

Find out more about Deaglo’s innovative approach to hedged share classes in our recent paper LPs take comfort in currency hedging.