As the world has become smaller and the search for yield has become more difficult, funds have benefited from increased exposure to international investments and foreign investors. However, even the most optimistic market projections point to a scenario of uncertainty, which could bring even more volatility to the markets.

Why consider a hedged share class

FX rate changes are to a great extent unpredictable and the market horizon is fraught with risks that could trigger even bigger movements than we are seeing today in currencies. The FX historic volatility in Emerging markets is at all time high (15-18%) with a wide range of economic growth rates and increased geopolitical tensions, has meant volatility is well and truly back.

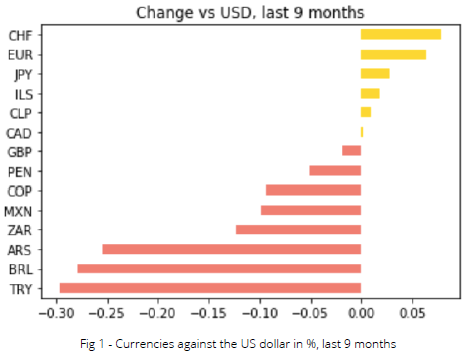

Over the last 9 months (Fig 1), the BRL has been the worst hit in LatAm, weakening 37%, while the Mexican Peso was down 16%. In eastern Europe, the Turkish lira has plunged approximately 30% since January. It is movements of this magnitude that are fading fund returns and therefore becoming a serious cause for concern. Fund managers can take proactive measures to mitigate the risk of exchange rate variation in their portfolios.

These measures contribute to reducing the exposure of foreign capital by minimizing the impact of exchange rate variation on the portfolio's return.Deaglo has created a simple and transparent way of determining, implementing, and executing FX risk. Substantially reducing risk for foreign investors and their international investments.

Types of Share Classes

Unhedged

In unhedged share class foreign currencies are left to move freely against one another. As a result, an unhedged investor may suffer losses or gains due to foreign exchange movements. Investors in this class should be comfortable with unhedged currency exposure, and be aware that there is both potential to profit from FX fluctuations in their favor, as well as experience currency-based losses. Often investors will take on the concept of “reversion to mean”, in the hope that markets will balance themselves out over time.

Hedged

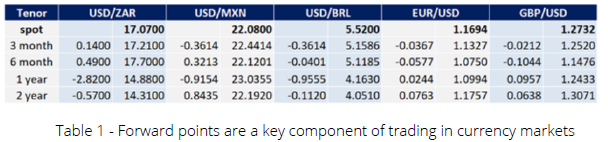

For an alternative manager raising capital overseas and distributing globally, there are two main types of FX exposure. Deployment phase: to eliminate functional currency depreciation risk. Harvest phase: to eliminate local currency depreciation risk.There can be a major benefit to hedging both phases. Usually, there is a cost associated with placing a hedge on a currency (Bid/Ask +/- Forward Points, see Table 1) however there can be benefits to hedging currencies depending on the direction. In some cases, interest rate differentials will favor the hedger and these discounts can partially offset the costs associated with the other side of the hedge (we call this roundtrip hedging).

There are numerous hedging methodologies available to a manager (layered hedging, fire and forget, rolling hedge, etc.), as well as different derivative tools (futures, forwards, vanilla options, swaps, etc.) that can be implemented. All should be considered along with their risks and rewards. It is therefore extremely important that the hedging firm’s risk appetite is clearly defined to ensure an expedited decision-making process and investor buy-in.

Currency Impact on Hedged vs Unhedged

Hedged share classes are capable of shielding investors’ returns against foreign exchange variation that can result in substantial losses. Thus, it allows General Partners to reduce considerable uncertainty in regard to the performance of a fund.

These are the main benefits:

1. Sharpe ratio of the hedged share class can be higher than unhedged share class;

2. Can achieve similar (or better) IRR;

3. Reduce or neutralize returns volatility.

On the other hand, unhedged share classes are fully exposed to positive and negative market movements. For those foreign investors looking for diversification from their home currencies or those with a strong predilection to the currency pair, an unhedged share class may be attractive. Our analysis takes the viewpoint on a U.S. based fund who has euro-based investors. The fund lifecycle is 6 years and the investors are investing Euro (EUR) in a U.S dollar (USD) based fund.

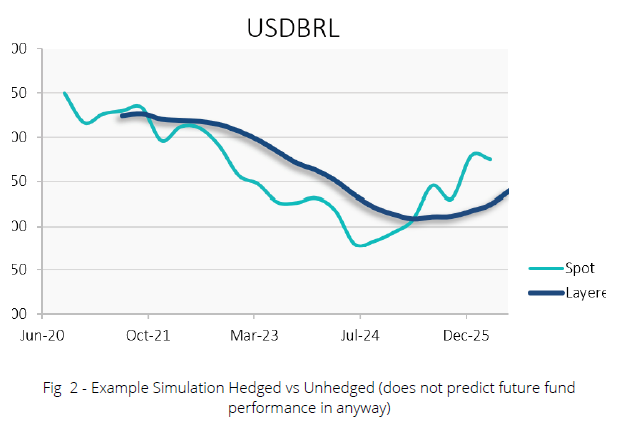

A euro-hedged share class is created for protecting the fund’s full lifecycle, which means, deployment and harvesting phases. The hedging strategy will smooth fluctuations in the EUR/USD exchange rate, reducing volatility (Fig 2). This strategy aims to give investors similar (or better) returns to the fund’s main ‘base’ currency returns with less risk.

The difference in the behavior of the two exchange rates, spot rate and hedged rate, respectively also highlights the effect it will have on the portfolio. With the layered hedging strategy, volatility is reduced between 60-80%. The effects of currency on the hedged share class performance has been clearly smoothed out compared to those of the unhedged class.

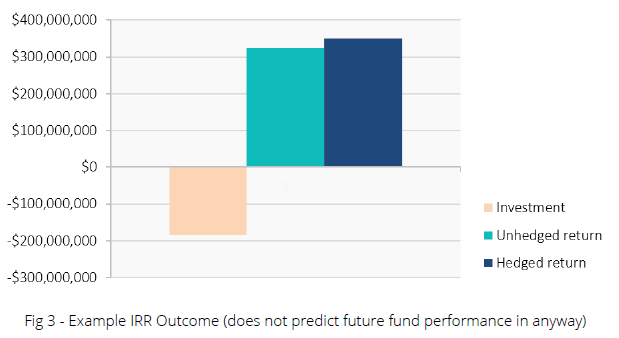

Below are the results of a simulation and analysis showing the performance of a roundtrip hedging strategy for a Brazilian PE Fund. The hedged share class had an IRR of 22.3%. Against an unhedged IRR of around 19.8% (Fig 3).

In this instance, the hedged share class reduced the volatility in currency pair by as much 75% and brought the Sharpe ratio up 4x higher.

Potential risks posed through a hedged class

- Interest rate differential - Hedging cost is priced on the basis of the spot rate and the difference between the interest rates on the two currencies, therefore forward points may increase or decrease and thus affect the moneyness of the strategy.

- Unrealised profit and loss (MTM, Mark-to-market) - When operating with hedge instruments, it is necessary to understand that depending on market movement, the fund will observe variations in the market value of its open positions, which can be negative or positive financial adjustments. Therefore, margin facilities are often required and collateral may need to be posted which can have a performance drag.

- Lack of forward contracts - Sometimes managing FX risk in emerging markets where currencies are more volatile, correlation to proxy currencies is poor, and hedging instruments are often non-existent or prohibitively expensive, the fund issuer must adopt more suitable hedging strategies such as proxy hedging.

- Costs - In a neutral market, the hedging costs will almost certainly negatively affect the performance of hedged share class compared to the unhedged. In some cases, the hedging costs may actually outweigh the expected performance of the fund.

- Additional risks - Investors in currency hedged share classes are exposed to the risk that the counterparty on the other side of the derivative contract defaults when payment is due.Mistiming between when an investment is made and when a hedge is applied can create temporary currency exposures

“An effective FX hedging strategy can help smooth out currency impact on investments and in some instances boost investor returns.”