In search for protection against the increased volatility of exchange rates, many companies have implemented hedge instruments.

However, implementing a hedge strategy can bring new challenges and even add unnecessary risk to companies if the strategy is not carefully analyzed and monitored.

In this sense, an unexpected negative variation margin of positions may introduce a new risk to the company's cash flow. Because, this is often accompanied by the need to post financial deposits (this requirement is also known as margin call) to cover negative positions, directly impacting the availability of the company's financial resources.

Although it is not possible to eliminate 100% the possibility of margin calls (except for long options), there are statistical tools that companies can adopt to estimate the likelihood of the occurrence of inconvenient margin calls in advance.

The statistical treatment, unlike market perspectives, is based on quantitative methods and provides more tangible results in the face of the uncertainties of the global economy. Thus, 4 advantages are highlighted so that companies know in advance the likelihood of encountering a margin call.

4 advantages of knowing the likelihood of a margin call occurring:

(1) Schedule cash flow in advance and comfortably;

(2) Adjust the provisioned capital supported by statistical evidence;

(3) Free up capital for investment in the core business;

(4) Request only the necessary credit from the bank or MSB;

In addition to the advantages listed above, knowing these numbers in advance can eliminate insecurity in the implementation of future new hedging strategies.

In order to understand the analysis of the estimated occurrence of the margin call, it is essential to know the mark-to-market mechanism, as well as how an unexpected negative variation margin can impact the companies' cash flow.

How does MTM work?

When operating with hedge instruments, it is necessary to understand that depending on market movement, the company will observe variations in the market value of its open positions, which can be negative or positive financial adjustments.

When this variation is negative, the company will be required to make a deposit to cover the negative mark to market in your account with the financial institution (if it does not have a credit line to operate).

Despite this mechanism being the main security factor for financial institutions, the margin call becomes a huge burden for many organizations, especially for those whose cash is illiquid.

The table below illustrates the operation of the daily adjustment mechanism.

In D+0, an FX exposure of $ 530,000 is hedged with a long derivative contract at a rate of 4.75;

In D+3, the position has a negative daily variation margin of $ 69,404.76, because the market is being traded below the fixed rate, so the company must deposit the amount of the negative variation with the financial institution;

In D+4, the position returns to a positive adjustment, so there is no margin call and the account balance is the positive variation margin plus the value of the margin call previously sent in D+3. The net account balance is $ 74,925.60 ($ 69,404.76 + $ 5,520.83).

How does variation margin impact companies?

However, the MTM has its disadvantages and inconveniences, especially for those companies that have cash flow with little liquidity or seasonal liquidity.

These categories of illiquid business can be farmers, hotels, tourism agencies, etc. In businesses like this an unexpected margin call in the off-season or out of season can have a significant impact on operating cash flow, requiring these companies to direct capital, previously allocated to core activities, to cover the negative variation margin.

Investment funds, be they private equity or venture capital, can have long-term investment projects (> 10 years) and, therefore, all the firm's capital is retained in the projects. The entity's cash flows are totally illiquid! To honor margin calls, the fund managers make provision for an amount that they believe to be sufficient or, at the worst necessary, withdraw invested capital from the project. In this way, the fund's return can be fully impacted by negative variation margin.

Lastly, companies must recognize hedge MTM today, even if the trade has future settlement. This accounting requirement can show virtual financial results that negatively impact the company's financials. Understanding Suzano’s case.

So, it is possible to estimate the likelihood of the margin call occurring? YES

Understanding the probability and the levels that will trigger margin calls will help organizations to optimize the resources provisioned or retained.

Deaglo developed a tool (mathematical model) using Monte Carlos simulations that makes it possible to estimate the probability of future margin calls.

Monte Carlo simulations are used to model the probability of different results in a situation that cannot be easily described in a closed equation.

The first step is to model possible movements in the foreign exchange market, featuring historical price movements with drift (a directional component, which can be zero) and a random component, characterized by a standard deviation (also known as volatility).

The simplest model is Spot (N+1) = Spot (N) * e (drift + random value)

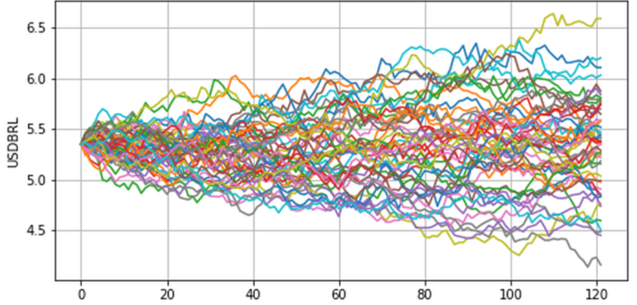

This will produce a subsequent random value based only on the previous value (a "Markov Chain"). This is repeated until an entire period has been modeled. These data points constitute a "path". The process is repeated many times (usually 10 or thousands of times) to generate a series of paths. See fig. 1, representing 90 days of price evolution with an annual volatility of 15% (100 out of 30,000 paths plotted).

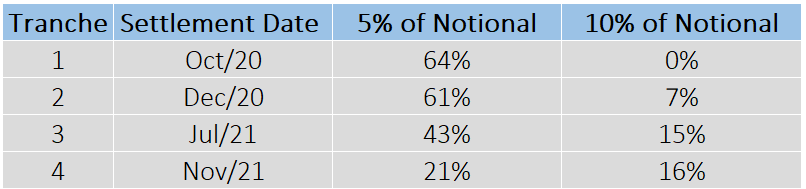

The next step is to use all the paths that the FX market can take until maturity and test them against the implemented hedge strategy (forwards, options, exotic options, etc.), this way we will have an estimate of how the strategy will behave throughout its term. The result of our analysis can be illustrated in a simple table:

The percentage reflects the fraction of the paths that triggered the margin call, at the two different trigger levels, 5% and 10% respectively.

As highlighted earlier, the results provide complementary inputs for managers to build effective planning and for smarter decision making.

Therefore, the analysis of margin variation is an essential item in the elaboration of any organization's hedge policy. Because, it is with responsible management and solid strategies, that companies expand results and architect the future of the business.