Offshore banking is often regarded as a complex and cumbersome part of a cross border transaction and can deliver considerable headaches to CFOs and their financial teams. However, with proper planning and innovative service providers and solutions, finance leaders can enable a quicker and more effective investment process. Below we explore some of the key points to keep in mind when considering a banking partner for your next foreign investment.

1. Jurisdiction

For years we have chosen offshore jurisdictions such as the Cayman Islands, BVI and Luxembourg. Each of these has a unique way of protecting foreign investors against less favorable onshore tax regimes. It is vital that you seek advice as to which jurisdiction is most suitable for your situation. Remember when it comes to actually setting up the bank accounts, your current bank may not have local branches or expertise in these jurisdictions, or you may be unfamiliar with the enhanced KYC or on-boarding requirements. This can lead to a lot of back and forth with compliance and tax attorneys.

One interesting example came up when we had a Bangladeshi and Indian investor that was interested in our client. We determined that Mauritius was actually a better fit in this instance rather than the BVI entity, due to a tax break. Finding a suitable banking partner in Mauritius was extremely difficult; however we were able to find a solution through one of our alternative banking providers.

2. Entity type

The jurisdiction, investor and investment type will ultimately determine the entity you will need to open. Make sure you are familiar with the tax benefits/burdens of each (to both you and your investor) before going through the formation. There are a number of legal and advisory firms that specialize in these types of company/partnership formations. Select a firm that can help you locally and introduce you to the most suitable partners as and when you need them.

3. Forming the entity

Without an entity formed you will not be able to get a bank account. Once you have decided on the type of entity you wish to open you will need to put together the application and file for the entity in the locale of choice. The fees are relatively transparent and shouldn’t be too costly. Remember you will need certain KYC and supporting documentation to complete the account opening process, so it's vital that this stage is complete before moving on.

4. Payment process

It's important that you determine the payment process early, as this can have a major effect on the provider you choose. If you need online access and multi-level approval or payment authorization you may not be able to work with certain banks. What’s more, if there is a need for an escrow agreement or any holdback clauses this can add costs and time. Either way, you need to make sure that the transaction process is spelled out and everyone knows each other's roles in the payment process to avoid delays.

5. Choosing a provider

Once the entity is formed most CFOs will go to their current banking partner and begin the bank account opening process. However, as I am sure you are aware this seldom goes smoothly or more importantly quickly. If they are able to open up in the required jurisdiction your newly formed entity simply does not have the necessary supporting documents required to open up the account. We have found that in most circumstances that a traditional bank account is not necessary. Most of our clients use segregated multi-currency accounts, which can be set up in a matter of days. These accounts act as de facto subscription and redemption accounts providing an immediate place to pool investor capital safely and efficiently. They can even provide alternative hedging facilities at reduced collateral demands.

6. KYC

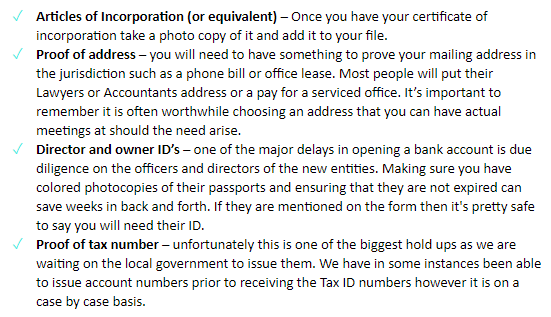

I advise my clients to create a folder on their computer for each new entity that they are opening and follow this simple checklist when opening up a new bank account.

Offshore banking is no longer just for the banks Over the past 12 years, we have handled billions of dollars worth of cross border transactions for investors, investment managers and companies all through alternative banking partners and service providers. Not only have they made the structuring and payment process more efficient, but they have also been specifically created for these types of transactions.

Have an upcoming cross border transaction? Our consultants are always available for a conversation.