Hedging BRL: a Case Study into the ways in which to hedge USD/BRL risk and the potential costs.

Interested in Growing with Overseas Investment? Don’t let currency fluctuations stand in your way.

The challenge

A Brazilian asset management firm (the client) with an existing USD share class was hedging using BRL/USD futures. They were confident that they would be growing the share class substantially and were interested in looking at alternative hedging products to help market to the growing US investor community. The client mostly trades in local Brazilian specialist private credit.

Brunel Advisors is a Latin American specialist advisory and capital raising boutique that works with diverse investment funds (including the client) to raise money offshore. Brunel Founding Partner Daniel Rummery says that for local Brazilian investment managers (particularly credit and similar yield focused strategies), currency risk or the cost of hedging is one of the principal obstacles faced by managers looking to raise money offshore. As yields remain compressed in the US and Europe, institutional investors continue to look further afield for attractive investments more abundant in emerging markets like Latin America. Nevertheless, a cost-effective hedging solution is crucial to ensure that the high local currency return remain attainable for international investors in USD.

The client’s request was three-fold:

- Help analyze the current hedging solution they have in place and quantify the costs of converting the initial subscriptions from USD to BRL and then hedging the class back to USD.

- Simulate alternative solutions to hedge on unintended gain and loss in the currency of the fund for comparison.

- Implement the new solution simply and efficiently.

The Process

Deaglo Partners suite of hedging solutions is primarily used to protect a company or investor against negative FX movements. Deaglo has substantial experience in identifying common issues and prescribing/recommending specific solutions across client types (investors), investment vehicles (private equity to hedge), and companies (multinationals). For this specific client, Deaglo followed this process:

- A risk assessment including flows and timings, value at risk and expected shortfall simulations.

- Comparative analysis of hedge alternatives to stabilize the returns, including a quantitative evaluation of hedge efficacy, Monte Carlo simulations and graphical presentation of results. Importantly, an evaluation of the financial costs of setting up each structure is included as well.

- Guidance on setting up both the onshore and offshore bank accounts to handle the subscriptions and redemptions.

- Implementing a separate credit facility that allows the fund to book contracts without tying up precious investor funds thus maximizing investor returns.

- Acting as a de facto escrow account while the due diligence on the investors is being completed.

- Converting the USD subscriptions into BRL and sending the funds over to the master account.

- Locking in the exact value of the Investment Managers base currency makes reporting far easier for the manager while still giving the investor a fixed USD return.

Risk assessment

Quantifying the risk is the essential first step. If the volatility of returns as represented in the share class is immaterial related to anticipated fund returns, hedging is not indicated.

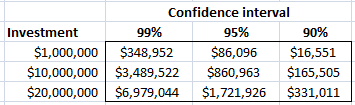

In this case study, USDBRL is quite volatile: the monthly volatility is 4.4%, which equates to 7.6%/qtr and 15.2%/annum. The following table shows Value at Risk (VaR) as a function of investment and confidence interval:

When VaR is of the same magnitude as the anticipated annual return hedging should be strongly considered.

Comparative Analysis

The first part of the solution – the in-depth analysis of current practice – required a thorough understanding of the client’s goals, existing fund structure and current hedging process. Below is a snapshot of the key discussions:

Current Process

The client had been using Futures to hedge their current BRL exposure and they were interested to see whether it made sense commercially to use NDF’s or options to hedge the BRL amount back to the USD. When Deaglo consulted with the client, an intense due diligence process took place – examining their investment parameters and weighing up the costs of execution against the cost of collateral.

Strategy return expectations = 17%

AUM in share class = $20m

Hedging product = Futures

Initial Deposit = 20% / $4m

Client

- Average Spread = 0.148%

- Average Cost = $33,559.51

- Total Cost = $234,916.58

- Estimated Annual Costs = $402,714.14

- Cost of collateral = $420,000

- Total Annualised Costs = $822,714.14

Deaglo

- Average Spread = 0.14%

- Average Cost = $31,700

- Total Cost = $221,900

- Total Execution Savings = $13,016.58

- Annualized Execution Savings = $22,314.14

- Total Savings with 0% facility = $442,314.14

After running a transaction cost analysis we determined that despite the client receiving tight pricing on their futures, there were a number of procedural nuisances created by using this type of contract over an NDF and that the options contracts would not satisfy the board's passive stance on hedging.

Futures (current solution)

Trading on the futures market has several advantages, including very low execution costs, the liquidity and safety of exchange-based trading, and price transparency. However, exchange-based trading only allows trading in fixed amounts, making it difficult to match exposure size. Worse, exchange rules require a daily mark-to-market, which is work intensive and requires the maintenance of a "slush" fund to meet M2M calls. Lastly, credit requirements demand the posting of initial margin.

Forwards (specifically NDFs)

Forwards are very similar in concept to futures, but are an OTC market, which obviates the futures disadvantages - notionals can be exact (in either currency), and margin requirements (both IM and VM) are negotiable. Gains/losses can be rolled at the end of each month.

One important decision is what tenor to use when hedging. Is it better to roll a hedge monthly, quarterly, or annually? The forward point curve is examined to determine optimum hedging tenors. From an examination of the table of rates, the annualized rate for rolling monthly is clearly the best alternative. We could also determine this from fitting an equation: points = .00005*months^2 + .0075*months + .0011. Because the second-order coefficient is positive, forward rates bend upward, again indicating it's best to roll shorter tenors.

This relationship needs to be monitored frequently, as the inflection and level can change quickly as a result of either FED or Banco Central do Brasil interest rate actions.

Options

Options are an interesting hedge alternative. They have the potential for upside, as well as protecting a rate (break-even). If the underlying is volatile, premiums are higher, making it more unlikely to realize upside. The most common strategy for optimizing the potential of options is to use them in combination (long/short, different strikes or tenors) to reduce or eliminate net premiums whilst leaving all protection in place, as well as some upside.

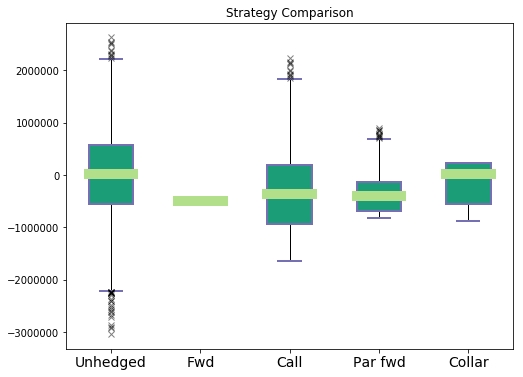

Evaluating different option strategies is complicated. Determining whether a collar or a participating forward is more beneficial is difficult. There is no close form math solution. We have found the best way to evaluate option strategies is to utilize Monte Carlo simulations. Evaluating each strategy over 10,000 market evolutions, and plotting the resulting distributions graphically makes it quite easy to compare them. Box plots showing the mean, 25th and 75th quartiles and the outliers instantly identifies which strategies are beneficial, and which are not.

Proxy hedging

Net strategy returns are impacted by the cost of hedging. Hedging costs using forwards is in the range of 2.5%/annum (table 2); which is about 1/7th of the projected return. Option premiums are quite prohibitive, resulting in positive outcomes in only a small portion of the distribution. There is another hedging strategy which, although not a perfect hedge, can be implemented at zero cost. This is proxy hedging.

When hedging currencies, it is very difficult to identify a single currency proxy with a useful level of correlation. When the correlation is poor, the portfolio variance and basis risk will be high. Using a "basket" of three to four proxy currencies can improve performance. However, identifying the basket using linear regression produces mediocre results and unnecessary basis risk.

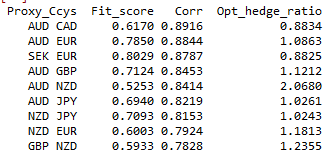

Deaglo has taken a more robust and novel approach. New machine learning algorithms such as Bayesian Regression overcome many of the limitations of the traditional approach. They are less sensitive to noise, less likely to over-fit, and make the most of available data (through train/test splits and k-fold cross validation). They are computationally intensive, but produce excellent results. Our programming can rapidly analyze many different combinations of two and three ccy baskets, identifying a few which are worthy.

From table 3, SEK/EUR is a strong candidate, with high fit and correlation. A Directional accuracy test is run, looking at historical gain/loss direction for the target and basket. From this we can see that out of 5 years of monthly data (60 data points), only 3 months did the proxy move in the opposite direction as the target.

Once the client has reviewed the pros and cons, and relative performance of each hedge alternative and made a choice, Deaglo helps in the actualization of that strategy

Conversion of subscriptions and fund movement

A multi-currency account was set up for both the US and offshore Cayman Feeder. Allowing the firms USD based investors to convert their funds into BRL at far more attractive rates. The accounts also act as an escrow account during the due diligence process. Once the subscription has been approved the funds are converted into BRL and released to the master funds local BRL account and the hedge can be immediately placed to protect the USD value.

Credit Facility

Deaglo worked with alternative banking providers to create a hedging facility away from their custodian bank. Posting both initial margin and variation margin on the client’s behalf freeing up valuable capital and eliminating frustrating daily M2M’s. The client is able to roll any gains or losses into their new contracts at the end of each month. Should they wish to crystallize a loss or gain into the fund earnings they are able to do so at their discretion. The facility is also able to grow with the fund as they add more subscriptions to the share class.

Conclusion

This client had garnered sufficient interest from USD based investors that warranted them opening a US share class. The fact that these investors all wished to price out a hedged version of this share class added complexity to the fund's current operation. However, this turned out to be a worthwhile exercise to grow the AUM. The decision to hedge was only part of the process though and it wasn’t until they were able to engage an expert like Deaglo capital partners that they were able to fully evaluate their current process. Deaglo helped them understand the true hedging costs above and beyond simple execution costs and forward points.

Our experts are more than happy to discuss your BRL exposure or any other cross border related question you may have.