Currency hedged share classes and cross border fund distribution

When approaching cross-border distribution, especially in Europe, the dynamics of the marketing authorisations versus the private placement regimes available - for instance - are topics which gathered attention the most in the recent past. This at least since the AIFMD was introduced. However, there are also other ingredients to successful cross-border distribution, more technical and product-specific in nature, which sometimes might end up overlooked by fund promoters. In this case we are talking about currency hedged share classes. This brief post aims at describing briefly some of the main EU regulatory considerations on currency hedged share classes and offer some technical considerations on the mechanisms involved in the practice of currency hedging.

The Background and the ESMA opinion

Whilst currency hedging is a mechanism that applies to all types of funds, currency hedged share classes came for the first time under the regulatory lens in Europe with regards to UCITS in January 2017. ESMA at that time had issued in fact a general opinion about share classes in UCITS funds (please find the text of the opinon here). One of the incidental conclusions of the ESMA opinion, which had a broader scope and was concentrated on the concept of share classes under UCITS, was that the only type of hedging practice acceptable at share class level in a UCITS was the one related to currency risk. The reason was that currency hedged share classes did not contravene to the principle that a sub-fund within a UCITS has to have a common investment objective.

Of course, in order to fully understand the opinion issued by ESMA, it helps to clarify its intended background. ESMA wanted to create some homogeneity with regards to the use and creation of share classes, with a view to to ensure that share classes were not used to pursue goals better achieved by separate sub-funds within a UCITS. The opinion from ESMA goes further into distinguishing UCITS funds or compartments and share classes, the latter recognised only in passing and for marketing related purposes under the UCITS directive, and creating some high- level principles to be followed by fund managers and promoters when creating share classes.

In a nutshell, currency hedged share classes are the only type of hedged share class deemed acceptable by ESMA. The currency hedging mechanism adopted in fact allows for investors to be able to mitigate currency risk and invest in funds with a different base currency. More broadly, currency hedging is seen as a mean to support a single market in Europe, whereby not all member states have adopted the Euro currency or have the same currency.

Now the technical part

Currency hedged share classes are also useful to US fund managers who may need to create share

classes in different currencies in order to attract capital from outside their home country. For example, a US fund manager willing to offer its offshore fund in the EU market might come up against the issue of having to create a Euro-based share class, with an inherent currency translation risk. The USD-valued assets, in fact, may appreciate as expected, but any depreciation of the Euro or appreciation of the same against the US Dollar during the investment period may materially affect the net returns for those EU investors. This unwanted volatility takes away from the pure returns of the funds.

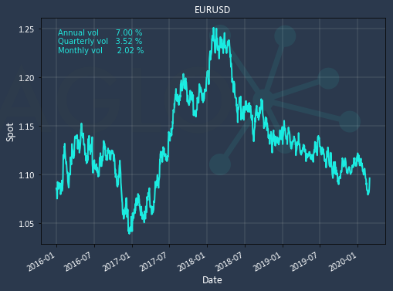

For example, an investor committing to a fund with a 10% annualized local return at the beginning of 2018 might expect a return of compounded 21% over two years. However, the EUR USD exchange rate in just two years has seen swings of nearly 14%, with a monthly volatility of 2% and an annualized Value at Risk 95% of 11.6%.

In this example, had it not been hedged, the share class would’ve materially added to the returns. However, significant gains in currency often raises flags with investors who wish to take the volatility out of their earnings. Also, most of the time investors decide not to invest in fund with a base currency different than their own. Thus, fund managers are more likely than not to hedge share classes in a currency different than the base currency of the strategy.

The cost of hedged share classes

In order to manage effectively currency hedged share classes, fund managers must consider several factors, the most important being the cost of hedging.

There are three components to the cost of currency hedged share classes to consider:

- Forward points - can work for or against the fund manager. In this case, hedging US Dollars back to Euro (ie selling USD forward) will be a cost for the hedger.

- Credit considerations - posting collateral for forward contracts can significantly reduce the amount of deployable capital for that particular share class.

- Spread and roll fees - the fees associated with placing these hedges can vary significantly across providers, with no correlation with the size of transaction or total AUM of the fund.

Tenor costs

The current lowest costs for hedging USD exposure for EUR investors is approximately 1.9%/annum (1-month tenors rolled at the end of each month). This is the preferred method for many managers as it tends to track the NAV of the fund more closely. However, rolling via this method usually means the client is paying “roll fees” 12 times a year (bid/ask plus provider spread), which often works out far more expensive than rolling longer duration contracts.

Credit costs

Also, forward contracts typically can go up or down in value and attract a credit risk. To minimize this risk, banks often require an initial margin deposit, which can be as much as 10-15% of the notional value of the hedge. Additionally, if the mark-to-market (instantaneous valuation) moves against the client more than a certain percentage, variation margin may also be required. These margin requirements can significantly impact the funds' cash position during the hold period. The manager must maintain a cash account to cover these margin calls, reducing the net EUR return further.

Spread costs

Lastly, the FX market is the largest unregulated market in the world and typically managers only have one banking relationship to hedge their exposures through. The lack of ability to compare pricing with an alternative provider often leaves clients in a poor situation from a negotiation standpoint.

Opening up a new banking relationship may be unnecessary, using an FX broker or an advisory firm could go a long way in helping those fund managers sharpen up bank’s pricing and significantly reduce share classes hedging costs.

Final considerations

For a US fund manager intending to offer a EUR share class for its USD based strategy, it makes tremendous sense to hedge that share class for currency risk. The volatility and the VaR is significant (11.6%), the hedging itself costs just over 2% /annum, and with the right provider, the credit costs can be minimized or even eliminated.

Guest author

Attilio Veneziano

Created in 2019 by Attilio Veneziano, World Gondola works in strategic partnership with best-of-breed law firms and industry service providers in Europe and across the globe.

Attilio Veneziano is a dual-qualified lawyer with more than 15 years experience, spanning from European extradition cases through the handling of complex pan-European fund distribution projects for European and US-based fund managers and financial institutions.

Attilio Veneziano is a veteran of the Square Mile and founder of Veneziano & Partners, London based leading regulatory boutique specialized in European Fund Distribution.

Founded in 2013 in the aftermath of AIFMD implementation, Veneziano & Partners works with some of the finest boutique fund managers and assists them in the pan-European distribution endeavors of their investment funds.