There has been substantial growth in direct lending deals across North America and LatAm in the last few years. Traditional banks' declining participation hinders the firm's ability to access capital in middle-market lending. As a result, various debt funds and alternative finance platforms are enabling agile and smart private credit investing for mid-size companies. Those funds cover different sectors of the economy, including renewable energy, healthcare, education, manufacturing, and so on.

However, in particular for Emerging Markets, there have been observed inefficiencies in these cross-border transactions from an FX standpoint. While foreign currency loans can be cheaper than local currency loans, they can expose firms to currency risk by creating a currency mismatch on their balance sheets.

Although fund managers are aware that a significant deterioration in the quality of foreign currency loan portfolios can expose them to earnings risk, they still pass over the currency risk to the borrowers. But, borrowers remain unhedged – this is particularly true when medium-size businesses don't have the expertise, creditworthiness, and resources to execute hedging strategies.

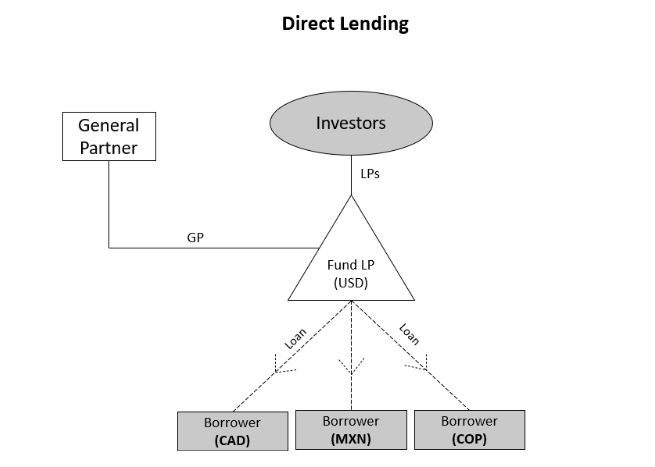

Fig. Typical Direct Lending structure

Against this backdrop, Deaglo has found that borrowers are more likely to implement (buy) an FX hedging strategy from their lender than from a traditional bank, and the reasons are obvious:

- Lower transaction spreads;

- More sophisticated hedging strategies;

- Lower or zero credit requirements;

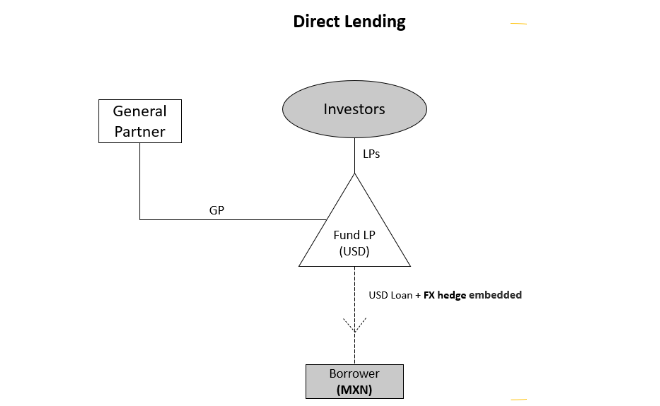

Taken together, this is only possible if the fund manager embeds an FX derivative into the USD loan. The lender typically enters into such FX derivatives with a hedging counterparty, and the hedging cost is embedded in the USD loan. The hedging arrangements that form part of a financial transaction will be dictated by the requirements set out in the facility agreement and the other financial documents.

Fig. Example of a USD loan with an MXN hedging embedded

At Deaglo, recent projects with U.S. credit funds show that previous lending relationships reduce the barriers to FX hedge, particularly for mid-size firms – eliminating the FX inefficient and bringing more comfort for all stakeholders: Investors, General Partners, and Borrowers.

Ultimately, USD loans backed by FX hedging allow U.S. credit funds to access multiple markets despite currency risks and achieve desired returns to their LPs.