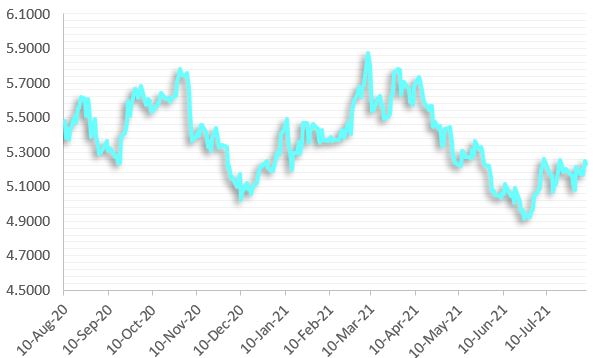

Uncertainty is a strange thing – Now more so than ever for Private and VC funds navigating their way in emerging markets. Foreign investors and fund managers tend to ignore what they do not know, out of fear. It just so happens that Foreign Exchange “FX” rate is like exploring the unknown. Let’s pick the Brazilian Real (BRL) against the U.S. dollar for example. Over the last 12 months, the currency dropped by 15% and registered a frightening annual volatility of 21.5% (Fig. 1). This is why foreign investors are afraid!

Figure 1. Historical Spot Rate USDBRL Chart. Source: Bloomberg

As a reference to FX risk management in LatAm, Deaglo is aware that existing hedging strategies do not work properly to reduce currency risk when cash flow amounts and timing are less predictable. Therefore, for Private Equity and VC funds, Deaglo has designed new hedging tools and new ways of thinking. This article underlines one very common case that fund managers face through our own experience - CAPITAL CALL IMPACTED BY CURRENCY FLUCTUATION – and highlights potential hedging solutions available.

Background

The Brazil-based VC Fund (“Fund”), which has raised U.S. dollar (USD) capital, submits a bid for a Brazilian asset priced in BRL. The bid is accepted on Aug 9th, 2021 and will be funded 20 to 30 days later. Typically, VC funds send out a letter to their LPs saying: “We have decided to invest in X company and we are investing Y% of the fund, please send us Y% of your commitment.” Fund managers usually give their LPs a period to send the capital committed (usually the same period cited below 20-30 days). Then, anytime during this period, these investors send the money to the VC investment vehicle and it is sent to the company the VC fund invested in.

The Challenge

Under this dynamic, the amount of USD needed will change between the bid acceptance date and the date the transaction is funded. Thus, the Fund will face two potential scenarios:

- If the BRL appreciates, more USD will be needed as the price is fixed in BRL. As a result, the Fund would need to call for more USD capital to close the transaction. This is an undesirable situation, as investors will have paid more for the asset than originally negotiated, eating into the internal rate of return (IRR) and other investment performance metrics.

- If the BRL depreciates and capital was made on the bid acceptance date, capital will need to be returned, as fewer USDs will be needed for the acquisition. This is also an undesirable situation, as having to give capital back presents an administrative and operational burden which most times represents additional costs.

For a fund, it’s always important to be efficient with capital!

Approach

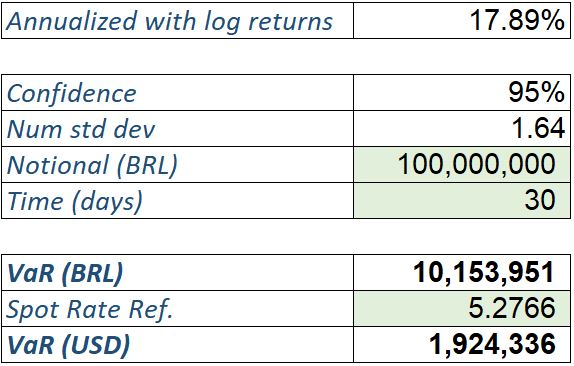

Value at Risk (VaR) is the methodology used to provide a single number which summarizes the total risk of financial assets (maximum possible loss), or in other words, it quantifies the FX risk. It has become widely used by fund managers (Fig. 2 and 3).

Project details

USD/BRL spot reference: R$5.2766 (09-Aug-21)

Notional Bid: BRL 100M

Time frame: 30 days

The current annual volatility for the USD/BRL pair is over 17.9%, which is extremely high related to other EM and major peers.

To illustrate how the currency risk could affect the capital call (BRL 100M), the 1-month VaR at 95% confidence level is BRL 10M. This means that with 95% probability the loss in 1 month will not exceed BRL 10M. But this also means that there is a 5% chance of losing more than USD 10M in this 30-day period.

Figure 2. Value at Risk (VaR)

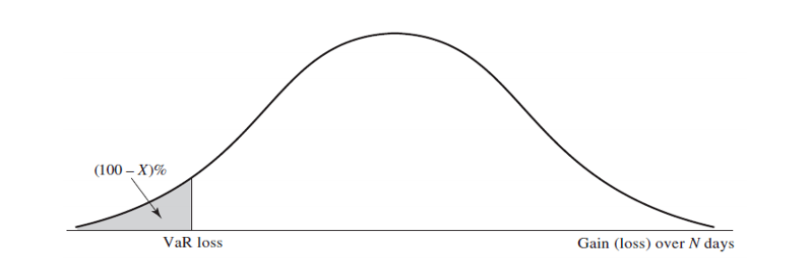

Figure 3. Calculation of VaR from the probability distribution of the change in the portfolio value; confidence level is 95%. Gains in portfolio value are positive; losses are negative.

Potential hedging solutions to protect the “Capital Call” stage against FX fluctuation

1. Using Forward Contracts

It might be the most frequently cited strategy for mitigating currency risk. According to EMPEA1 , amongst those who looks to protect the capital calls, 48% opt to use Non-deliverable forwards (NDF).

Trade details

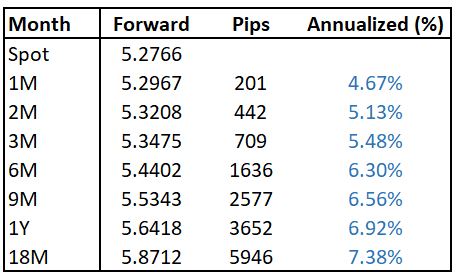

USD/BRL spot reference: R$5.2766 (09-Aug-21)

Direction: Sell USD / Buy BRL

Notional: BRL 100M

Tenor: 1 month

Contract Rate: R$5.2967

USD equivalent: $18.8M

Regardless of where the USDBRL pair should be trading on expiry date, according to the terms of the forward contract, (Fig. 4) the Fund will be selling USD18.8M in exchange for BRL100M to make the investment.

Figure 4. USDBRL forward curve. Source: Bloomberg

Specific points

- In the event the deal was to close earlier than expected, forwards may be drawn down or unwound early without penalty.

- A delay in the expected deal close date can be handled by rolling the forward for an additional week, month, etc. as required.

- An FX credit line or collateral posting is required to execute forwards.

2. Using Options

OTC options may be more useful as they incur fewer cash management burdens on the GP and there are several option strategies that combine buying and selling products to take a bullish, bearish, or neutral position on the currency pair in order to allow Customer to benefit from a further depreciation/appreciation.

In this situation, the main object of FX risk management is a reduction of upside risk, with the preservation of potential downside.

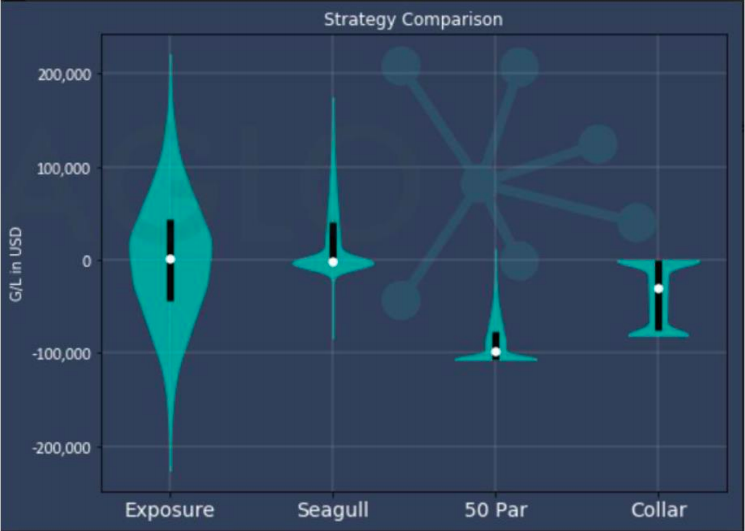

Deaglo uses Monte Carlo simulation techniques to evaluate option performance against the unhedged exposure (Figure 5). The results of the simulation are graphically displayed using "violin plots", which show the comparative distribution of G/L across 10,000 different simulations.

Figure 5. Strategy Comparison

Specific points

- An FX credit line or collateral posting is required to execute Short Options.

- Options OTM “Out-of-Money” can be affordable.

- Options strategies can be designed to protect against a worse case scenario rate (a USDBRL level that management fee would be impacted).

- Several option strategies that blend buying and selling products can be a zero-premium strategy, low risk, provides full protection (100% hedge) and participation in further appreciation/depreciation.

Conclusion

Hedging short-term cash flows, such as Capital Calls, is an important step in order to protect the fund metrics (IRR, Sharpe Ratios etc.) against the volatility of currencies. Although Forward Contracts are the most frequently cited strategy for mitigating short-term risk, it does not allow any potential participation, and analyzing the forward points curve and collateral posting could be a hurdle. Option strategies is an excellent hedging alternative to mitigate short-term risk and maximize the potential for gains. When using Monte Carlo techniques to model the range of outcomes, Deaglo is able to help the client visualize, understand and gain insight into the performance of various options hedge strategies and, ultimately helping them to select the one that met their needs best. Finally, Private Equity and VC funds should pay attention to short-term exposure and create a framework to quantify the benefits of an active approach.