Economic outlook

India has confirmed more than 450,000 cases of COVID-19 so far, making it the world’s fourth-worst-hit country. Delhi and Mumbai are particularly badly affected, with hospitals struggling to accommodate critically ill patients. India’s COVID-19 cases have surged in early December, with the Supreme Court (why are they involved??) warning that the situation could worsen further if authorities did not effectively deal with the pandemic.

Economic reforms should support some medium-term growth, although the most recent efforts to reform farm price supports is under strong attack. It's expected that Modi and his ruling party to stay in power until its scheduled term in 2024. Tensions with China and Pakistan will remain high but will (hopefully) not lead to a large-scale conflict.

The economy is projected to decline in FY 2020 (April 2020–March 2021) as stringent Covid-19 containment measures do the damage we've come to expect. The ongoing spread of the virus and potential snap-back of lockdown measures, coupled with fiscal stimulus measures falling well short of the mark(see below), continue to pose downside risk. Analysts are projecting GDP to fall 9.3% in FY 2020, and increase between 6.9-9.2% in FY 2021 (we found multiple estimates). That basically leaves 2020 as a lost year, but not much worse.

Government and Central Bank

In November, the government outlined the third installment of stimulus, focusing largely on credit growth, job creation and infrastructure. Total spending on Covid-19 relief amounts to roughly 6% of GDP so far. That is pitiful compared to Japan (21%), US (13%) and even Turkey (12%), and will likely have a limited impact on the recovery and fiscal health.

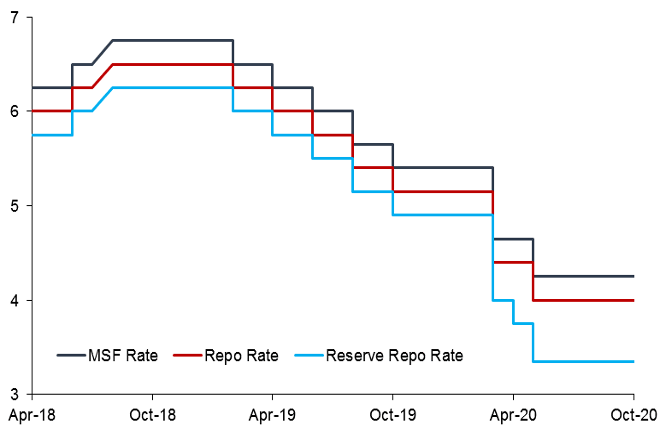

At its monetary policy meeting ending on December 4th, the Reserve Bank of India (RBI) kept the Bank’s policy rates unchanged ( meeting market expectations.) The RBI left the reverse repurchase rate, the repurchase rate and the marginal standing facility rate at 3.35%, 4.00% and 4.25%, respectively.

At its monetary policy meeting ending on December 4th, the Reserve Bank of India (RBI) kept the Bank’s policy rates unchanged ( meeting market expectations.) The RBI left the reverse repurchase rate, the repurchase rate and the marginal standing facility rate at 3.35%, 4.00% & 4.25%, respectively.

Source: Reserve Bank of India (RBI).

FX

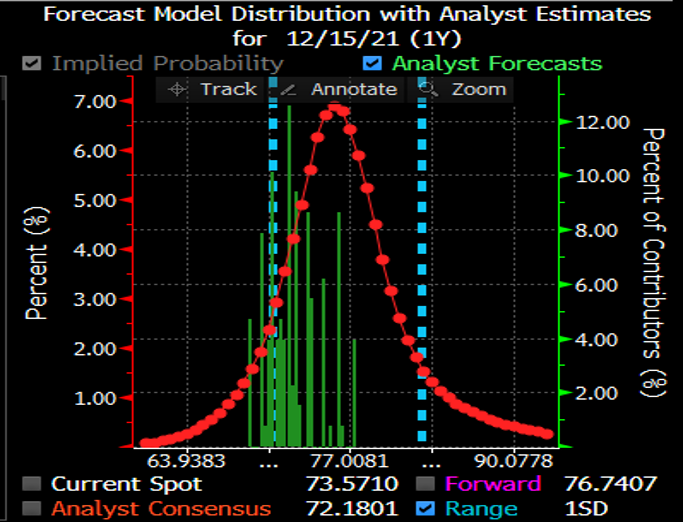

INR has been on a very long-term depreciating trend, as seen here in this 10 year chart (INRUSD, non-ISO). It's lost almost 50% of its value in that time. However, it's been a slow, steady process, and so the volatility is actually not very high, at only 6.5%/annum.

Analysts forecasts for the next 12 months cluster around 70.5, slightly lower than the current spot rate of 73.57

Hedging costs

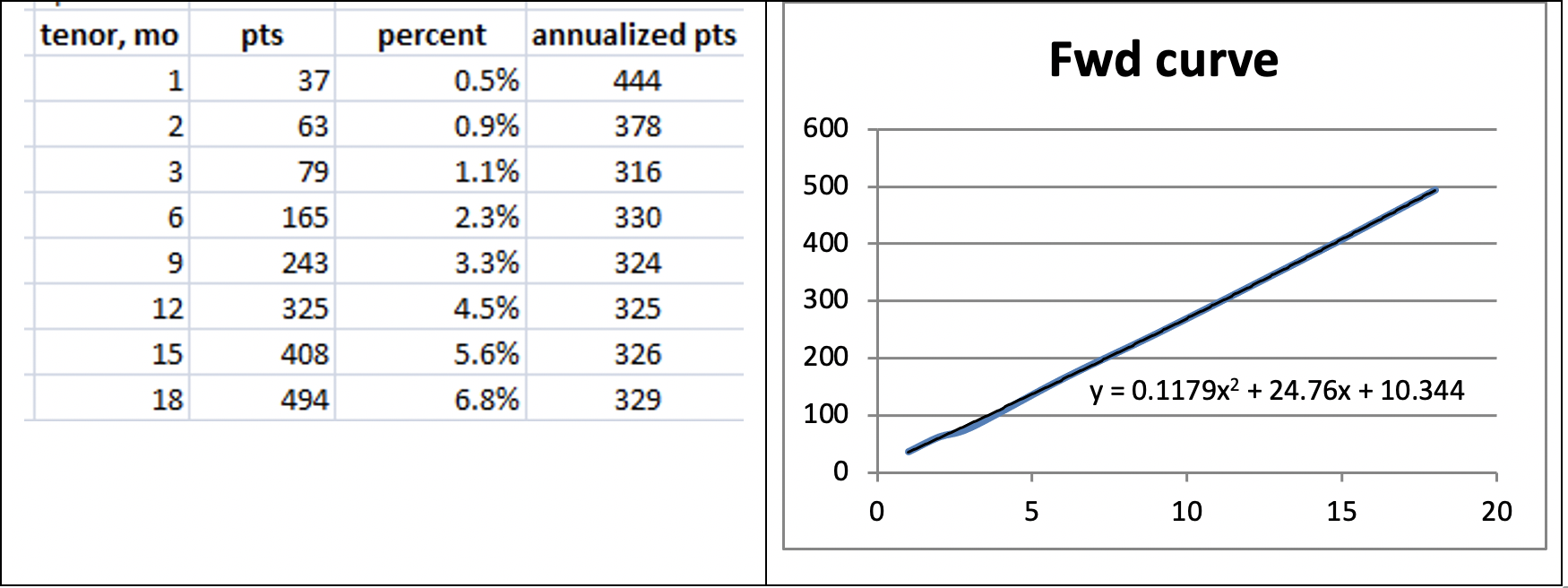

Fortunately, as central banks have been busily reducing rates in response to the pandemic, the cost of hedging has come down dramatically. Five years ago, forward points were more than double today's. Hedging costs using NDFs are about 4.5%/yr, favoring selling USD/buying INR. If rolling forwards, the curve favors long-tenors if selling INR, short tenors if selling USD.

Additionally, option implied volatility is also relatively low, at 7.2%. This results in a USD Call/INR put at the money premium of 5.9% for 12 months.