More sponsors appear to be urging GPs to structure currency hedged share class in markets with severe currency fluctuations.

Written by Matheus Zani

_________________________________________________________________________________

When investing in emerging markets, currency volatility in long-hold funds is always going to be a concern for Limited Partners (LPs or institutional investors). However, these concerns tend to be ignored by their General Partners (GPs), who often deem managing currency risk too expensive and time consuming. This approach has proven to be inadequate, especially when it comes to delivering risk adjusted returns in distressed market conditions. We’re now seeing many institutional investors better understand not just the impact currency fluctuations can have on their investments but how it can be mitigated.

As such, many are now demanding their GPs begin providing foreign hedged share classes in response. After all, if LPs entrust their investments to GPs, they can rightly expect these managers to take on the responsibility of managing their currency risks too.

This demand is also being driven by a combination of increased market volatility and decreased hedging costs (Fig 1), meaning currency hedging is simultaneously more vital than ever while also being the most accessible it’s ever been. As a result, we’re seeing LPs of various funds asking fund managers to provide hedged share classes to ensure investments remain insulated from abrupt currency value changes, particularly in the case of close-ended funds.

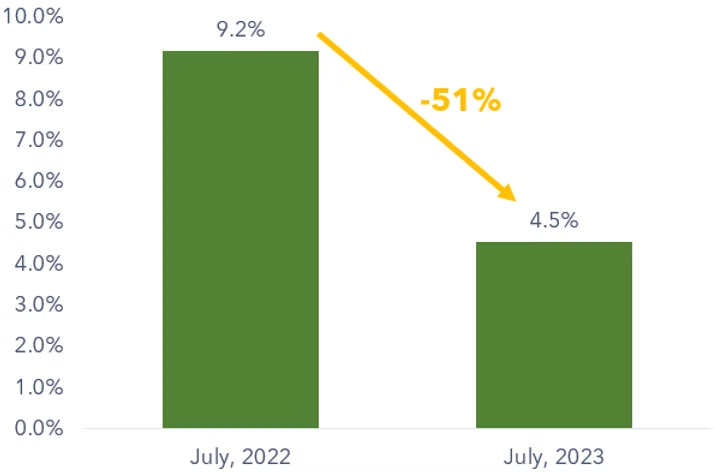

FIGURE 1: HEDGING COST FOR BRAZILIAN REAL (USDBRL)

Source: Bloomberg. The portfolio manager will pay the interest rate differential (IDF), often referred to as carry between USD and BRL.

When investing in emerging markets, currency volatility in long-hold funds is always going to be a concern for Limited Partners (LPs or institutional investors). However, these concerns tend to be ignored by their General Partners (GPs), who often deem managing currency risk too expensive and time consuming. This approach has proven to be inadequate, especially when it comes to delivering risk adjusted returns in distressed market conditions. We’re now seeing many institutional investors better understand not just the impact currency fluctuations can have on their investments but how it can be mitigated.

As such, many are now demanding their GPs begin providing foreign hedged share classes in response. After all, if LPs entrust their investments to GPs, they can rightly expect these managers to take on the responsibility of managing their currency risks too.

This demand is also being driven by a combination of increased market volatility and decreased hedging costs (Fig 1), meaning currency hedging is simultaneously more vital than ever while also being the most accessible it’s ever been. As a result, we’re seeing LPs of various funds asking fund managers to provide hedged share classes to ensure investments remain insulated from abrupt currency value changes, particularly in the case of close-ended funds.

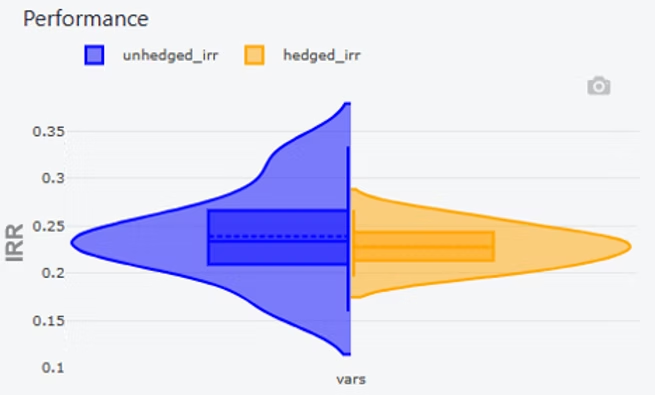

FIGURE 2: COMPARISON BETWEEN UNHEDGED AND HEDGED SHARE CLASSES

Source: Deaglo. Investment cash flow with a horizon of 6 years.

For GPs to offer hedged vehicles for long-hold funds (with a horizon of 3-10 years), they should consider an active overlay approach, aided by an adaptable and innovative counterparty. These strategies are designed to dynamically adjust the hedge ratio applied to currency exposures over time. This provides downside protection by minimizing the risks associated with unhedged currency exposures, while also enabling upside participation to capitalize on favorable currency movements. For this purpose, positions are commonly established using Forwards/NDFs and Options contracts.

The active overlay strategy not only aims to reduce currency exposure volatility related to the underlying assets but also strives to enhance portfolio returns by actively participating in favorable foreign currency movements through hedge ratio adjustments. To facilitate this approach, sophisticated counterparties offer innovative solutions such as historic rate rollover (HRR) and option premium deferment. These solutions allow GPs to avoid drawing down on capital commitments to settle an 'out-of-the-money' FX hedge and paying upfront premium costs. As a result, GPs can eliminate any potential cash drag on IRR performance in a fund’s early stages.

Escalating demand for hedged share classes from LPs, volatile markets and cheaper hedging costs, means it’s easier and more essential than ever that GPs take proactive measures towards the intricacies of currency volatility in long-hold funds and recognize the critical importance of robust currency risk management. Embracing hedged share classes not only addresses the growing need for stability and security in investments but also establishes GPs as dependable and forward-thinking partners to existing and future LPs. By responding to this demand, GPs can strengthen their position in the market, bolster investor confidence, and pave the way for successful and resilient investment journeys.

Matheus Zani

Head of FX Risk Management

mz@deaglo.com