South Africa's economic outlook for 2024 remains uncertain, shaped by persistent power outages, high inflation, and sluggish global growth. The country's GDP grew by a modest 0.4% in Q2 2024, mainly driven by the services and mining sectors. However, frequent load shedding continues to dampen economic activity and erode business confidence.

Inflation surged to 6.8% year-on-year in August 2024, well above the South African Reserve Bank's (SARB) target range. The increase is primarily due to rising food and energy costs, coupled with a weaker South African rand (ZAR). Core inflation, which excludes volatile food and energy prices, also climbed to 5.4%, indicating more pervasive price pressures. Despite this, recent declines in oil prices have eased inflation expectations, with the five-year breakeven rate dropping to 4.43%, below SARB's target of 4.5%. This trend has boosted sentiment around South African Government Bonds (SAGBs), leading to strong inflows at recent bond auctions, where demand has exceeded supply fivefold.

Global economic uncertainties also loom large. Higher-than-expected US core CPI data for August 2024 has bolstered expectations of a modest 25-basis-point rate cut by the Federal Reserve, leading to higher US Treasury yields and reduced capital flows to emerging markets (EMs). Initially, the ZAR strengthened but later lost ground as EM currencies faced downward pressure due to a capital flight to safer assets.

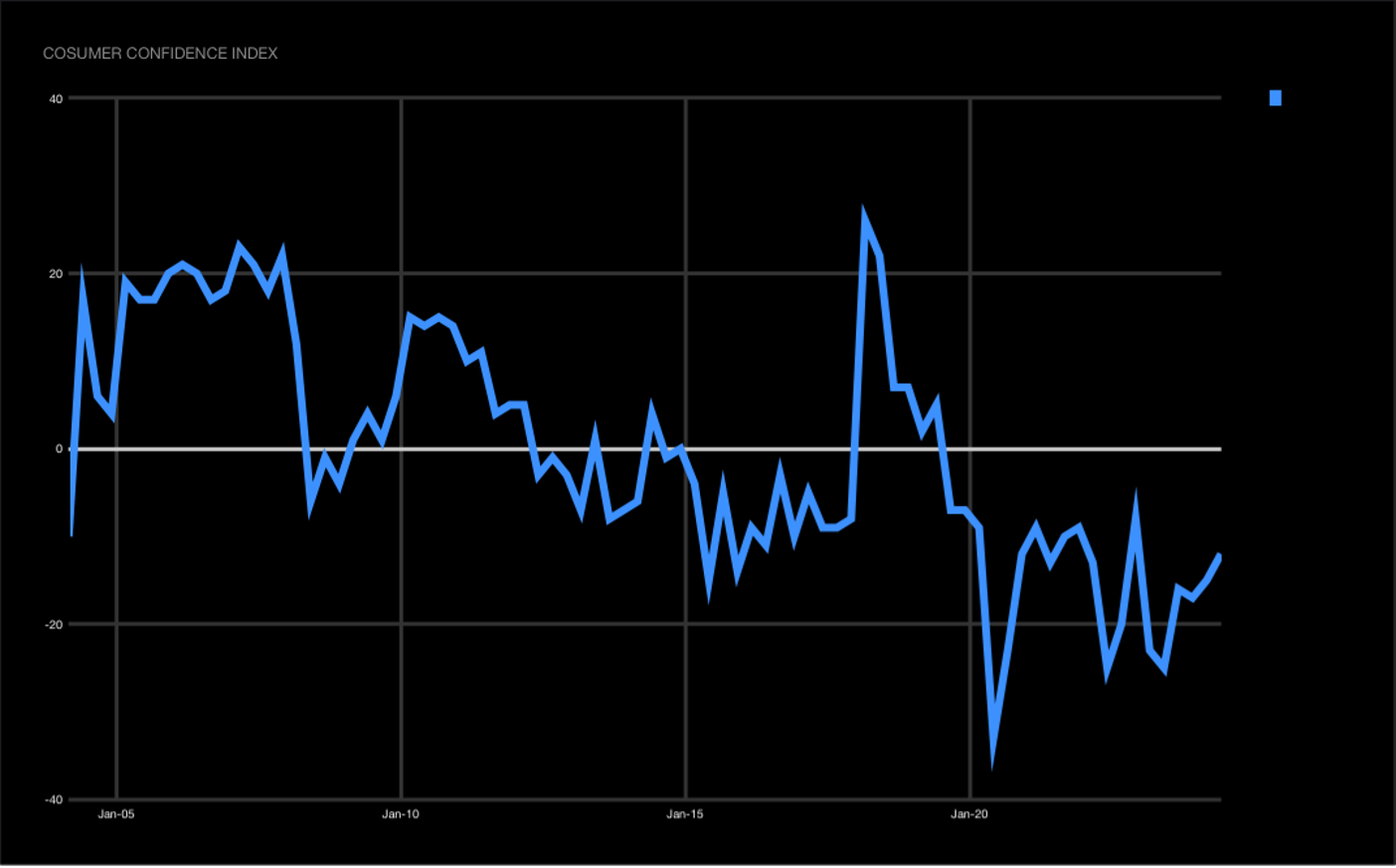

Consumer Confidence: Persistent Concerns Among South Africans

The FNB/BER Consumer Confidence Index (CCI) shows a slight recovery from -25 index points in Q2 2023 to -16 in Q3 2023. However, it dropped marginally to -17 in Q4 2023. Despite this improvement, the index remains significantly higher than the record lows experienced in early 2023. The latest reading, however, marks the lowest festive-season consumer confidence level in over two decades, reflecting ongoing economic concerns among South African consumers.

Pension Fund Withdrawals: A New Challenge for South Africa's Economy

A recent change in South Africa's pension sector may add to economic uncertainty. Following the enactment of a new law that facilitates easier access to pension funds, the South African Revenue Service (SARS) received 161,607 tax-directive applications between September 1 and 10, 2024, amounting to 4.1 billion rand in requested withdrawals. These withdrawals are primarily related to savings withdrawal benefits, such as divorce settlements, transfers to retirement funds, and personal withdrawals. While this development could stimulate short-term consumer spending, it may also reduce long-term savings and impact the domestic investment environment, posing potential challenges to future economic stability.

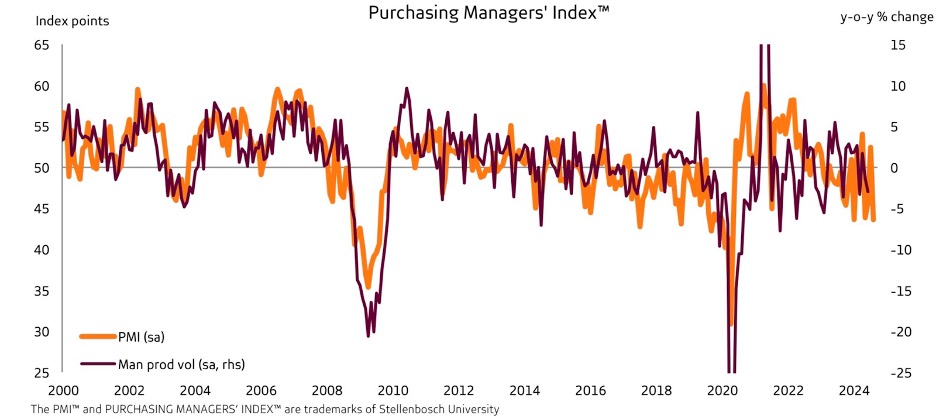

Purchasing Managers' Index (PMI): Manufacturing Sector Contracts

The South African Purchasing Managers' Index (PMI) fell below the critical 50-point threshold, dropping from 51.1 in July to 49.5 in August 2024. This decline signals a contraction in the manufacturing sector, driven by challenges like supply chain disruptions, high input costs, and ongoing load shedding, which have all contributed to reduced business activity and weaker demand conditions.

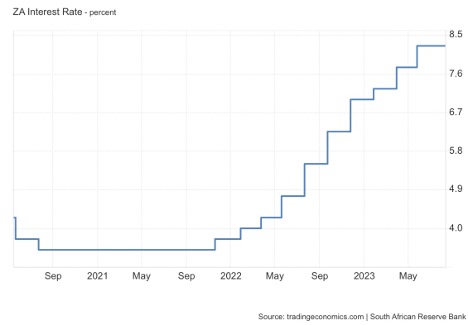

South African Reserve Bank (SARB): Another Rate Hike to Curb Inflation

The SARB raised its repurchase rate by 25 basis points to 8.5% in its September 2024 meeting, marking the fifth consecutive rate hike. This decision aims to curb inflation, which remains stubbornly above the central bank's target. The SARB's future moves will depend on global economic developments and the inflation trajectory.

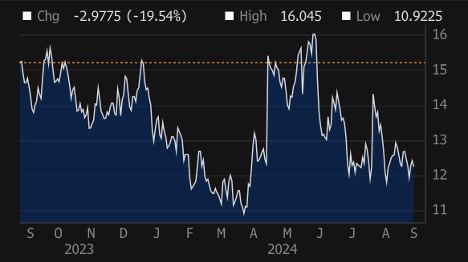

FX Market and Hedging Costs: Volatility Persists

The ZAR has experienced fluctuations driven by both domestic and international factors. Following the release of the US CPI data, which increased expectations of limited rate cuts by the Federal Reserve, the ZAR initially strengthened but subsequently lost ground. This trend reflects a reduced appetite for riskier EM assets. Currently, the 10-year generic rand bond yield stands at 10.4%, and the 5-year Credit Default Swap (CDS) spread is at 190.77 basis points, highlighting ongoing risk concerns.

Volatility in the ZAR market also impacts hedging costs. The forward curve remains relatively flat, indicating consistent hedging costs across different tenors within a year. The 5-year CDS spread has shown slight improvement, suggesting cautious optimism among investors regarding South Africa's creditworthiness. The USDZAR 1Y ATM volatility remains a key indicator for hedging strategies.

Conclusion

South Africa's economic outlook for 2024 is marked by both challenges and opportunities. While inflation remains high and economic growth sluggish, there are signs of optimism in bond markets and a cautious recovery in consumer confidence. However, the volatile FX market and potential economic impacts from pension fund withdrawals highlight the need for prudent economic management and strategic planning in the months ahead.