In a world of uncertain prospects for established economies, investors are looking for alternative markets and opportunities of growth. The traditional home for foreign direct investment (FDI) – the US dollar – has seen its recent position of strength weakening significantly in 2023. The U.S. dollar index appreciated over 12% in 2022, hitting a two-decade high in September 2022, however, by April 2023 the USDX had the dollar down by 10%, making it the worst performing currency in the G-10.

The reality now is that the factors that had proved so supportive of the dollar earlier in 2022 have since inverted. Coming out of the pandemic, the aggressive tactics of the Fed positioned the dollar for a confident position, but with ongoing supply chain challenges, a looming Fed banking crisis and UK mortgages in flux, investors are understandably worried about a potential credit crunch.

In typical fashion, emerging markets typically perform well when the dollar is weaker – opening the door for other economies to surge ahead as traditional markets slow. Here we examine the US’s closest continental neighbor, Latin America, where currencies are significantly undervalued in respect to their fair valuation estimates and what this means for overseas investors.

The LATAM picture

In 2023, Latin America is coming from a long period of sluggish growth, with the last decade in which the region’s annual growth rate has averaged only 0.9%, while being hit hard by the global pandemic.

However, in 2023, we are seeing the conditions for a major rebound in economic growth.

As accelerating inflation and aggressive U.S. Federal Reserve tactics weighed on asset prices, exacerbated by the invasion of Ukraine, Latin American currencies have continued to outperform on monetary policy tightening cycles, taking advantage of low baselines after the region's economy and shifting investment trends.

These opportunities are closely tied to the fate of the dollar. In 2022, for example, currencies of Colombia and Chile contracted 22% and 8% respectively in the face of declining capital inflows, rising inflation and higher borrowing costs. This aligned with a sharp decrease in VC investment in the region, as growth stage financing in Q1 fell 84%

However, in comparison to the dollar, many LATAM currency returns have fared strongly in the first half of the year, including:

- Colombian Peso: 18%

- Mexican Peso: 14%

- Brazilian Real: 10%

- Chilean Peso: 5%

Challenges still remain, namely a drop in global commodity prices, higher interest rates and China’s unsteady recovery, but Latin American economics have shown resilience and sound macroeconomic strategy and proactive monetary policy, with both poverty and employment mostly back to pre-pandemic levels, while average inflation, excluding Argentina, is expected to decline to 5.0 percent in 2023 after reaching 7.9 percent in 2022.

Regional analysis

Brazil

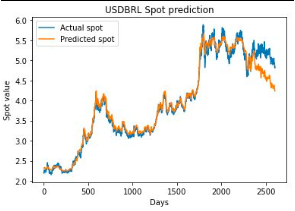

The Brazilian real has performed strongly in recent months, recovering from a slump in 2022 to jump by more than 13.9% from the lowest level this year.

In recent weeks, the actual value is now trending towards the predicted values in our own models, suggesting optimism for the currency in the second half of 2023 indicating a potential correction. Key factors indicate we might be entering a positive cycle include:

- Interest rates: After a surprisingly aggressive tightening campaign that added 11.75% points to baseline rates to fight inflation over 2021 and 2022, the central bank opted to keep its benchmark Selic rate at 13.75% in May and June, indicating the potential for cuts in future, potentially closing the year at 12.25%

- Inflation: Consumer prices in Brazil fellmore than expected in May, with 12-month inflation hitting its lowest level in more than two years and dropping below the 4% mark for the first time since late 2020.

- Growth: Growth prospects have increased rapidly, with annual economic output predictions in June rusing to 2.14%, up from 1.6% only a month before, boosted by booming agricultural exports.

This success is reflected in FDI, which more than doubled in 2022 compared to 2021, to $90.6 billion, its highest level in a decade, according to central bank data. While recent months have seen some contentious back and forth between President Lula and his central bank, the moderating influence of the current center-right congress indicates a stable base from which to focus on growth.

Chile

Chile has seen more uncertainty than other countries in Latin America, lagging behind other growth rates, with its heavy exposure to global metal prices and the arrival of a reformist government in 2022.

After dropping to a record low of 1,050 pesos per U.S. dollar in reaction to a sharp drop in the price of copper in 2022, combined with a contentious constitutional referendum, the peso has since stabilized at 800 pesos per dollar, and is predicted to remain at a similar level for the rest of the year on the back of returning Chinese demand for metals.

Foreign investment in Chile rose 12% in 2022, reaching US$17.1 Billion, 36% higher than the five-year average of US$12.617 billion and 23% higher than the average for the 2003-2022 historic series (US$13.921 billion).

The indications are that the fundamental drivers in the economy are pulling back on appreciation, with conditions favorable to stability, but not real growth. Recent indicators point to the likelihood of central bank rate cuts as the cenbank looks to incentivise growth, with much of the future of the peso hinging on Chinese economic policy and appetite for Chilean exports.

Argentina

The chief outlier in the LATAM region, Argentina is experiencing its worst economic crisis in years, with sky-high inflation (130%) making the Argentine peso the worst performing emerging market currency in 2023. Meanwhile, the central bank’s benchmark interest rate sits at an eye-watering 97%.

The government has so far resisted officially devaluing the currency, attempting to use other financial strategies to control the plummeting value of the peso. The current situation has been exacerbated by a severe drought affecting crop production, rising parallel FX pressures and political uncertainty as incumbent President Fernandez has stated his intention not to run for reelection in October.

While steps such as introducing a new 2,000-peso bill may ease the physical demands on wallets in a country where half of all commercial transactions are still carried out in cash, it is likely that until more drastic action is taken, likely devaluation, the slump in value is likely to continue.

Mexico

Mexico has found its currency on a roll this year, with the peso reaching its strongest level in more than five years at the end of Q1 and cementing it as the best performing EMFX currency of 2023.

Part of the success lies in following the aggressive fiscal policy of its neighbor the USA, matching the Fed hiking cycle to keep inflation under control.

In doing so, the country has also benefited from a range of stable and growing currency inflows, including:

- Strong flows of remittances back to the country from the US, standing at $5bn per month, accounting for 4 per cent of the country’s GDP.

- Growing interest in nearshoring the production of goods closer to America, including in its attractively priced auto sector.

- Foreign direct investment in Mexico hit $35.3bn last year, the highest level since 2015, according to economy ministry data. Transport manufacturing accounted for 12 per cent of that.

Mexico’s FDI 48% in the first quarter from regular flows recorded during the same time last year, as businesses invest in production closer to US markets, with multiple key mergers (Grupo Televisa SAB and Univision Holdings Inc. and the restructuring of Grupo Aeromexico SAB) alongside which were not counted in official figures. The spread over the Fed’s fed funds target rate has grown from 3.75 per cent to 6.25 per cent, making it an attractive currency for emerging market carry trade investors.

Colombia

In a notable exception to markets’ traditional fear of uncertainty, the looming specter of a change in government has recently driven the peso to a 10-month high against the dollar.

Incumbent President Gustavo Petro is under threat from a potential corruption scandal, derailing market reforms that had put off investors and international market participants. Aside from the proposed changes to health, pensions and the labor market, Colombia benefits from sound fundamentals that have driven peso gains of 13% year to date, surpassing even the Mexican currency.

Colombia has established one of the best fintech hubs in the region alongside key markets like Brazil and Mexico bringing massive amounts of FDI into the country reaching $3.9 billion in December 2022 alone, – nearly as much as it received in the entire first half of 2021. Investments in technology and innovation have tripled in Colombia in the last two years, making it the third largest technology ecosystem in the region.

Combined with robust positioning from the central bank, there is confidence for carry trade investors to deal in Colombian pesos on a par with the BRL, reflecting the solid foundations of both countries.

What does this mean for FDI?

Despite the diversity in the region, LATAM regions have shown themselves to be attractive, fiscally sound and balanced in their approach to maintaining their currency, with the current exception of Argentina.

As global trade revives post-pandemic, there is a greater market for the commodities, services and workforce that the continent can provide, boosted by increasing infrastructure investment and sound fundamentals.

With the ongoing weakness of the dollar, LATAM countries have the opportunity to reposition themselves as a favorable vector for currency movement and growth.

The long term value of this approach will depend on how the region’s government deal with the challenges and opportunities presented to them. The World Bank has suggested that countries in the region should preserve their resilience and take advantage of the opportunities presented by nearshoring and green industries to boost economic growth.

Massive flows of VCs and Fintech driven businesses in key markets such as Mexico, Brazil and Colombia, have established attractive hubs of innovation, tech and growth. While some funds have pulled back on investment, Q1 2023 nevertheless saw $129M of VC dollars deployed into 100 startups hailing from the region.

In a world where the dollar has lost some luster as the safe haven currency, LATAM could arise as a valuable new harbor for investment.