As 2020 nears its end, most of us will be happy to see the back of it. The year has been plagued by the global coronavirus pandemic, political instability in many countries, some expected some not countless natural disasters worldwide. There's no shadow of a doubt, 2020 has been a difficult year.

A year that the Federal Reserve's performance was essential not only to support the American economy, but also as a guide to international markets. A situation that led the Fed to respond strongly to the economic crisis caused by Covid-19 by cutting and maintaining interest rates at historically low levels, as well as launching various fiscal and loan programs to support the U.S and foreign companies operating in the country. Since then, the Fed's main mission has been to revive a fragile economy that has been hit hard by restrictive measures to combat the spread of the virus.

At the same time, during November, numerous advances in the development of vaccines against Covid-19 were announced. Hopes were buoyed that at the beginning of 2021 part of the at risk population may be vaccinated, and some statistics point out that by mid-July, the vaccine will be available to a large portion of the world population. In this scenario, the American economy should gain momentum as sectors such as hostelry, services and transportation that were hard hit by the crisis are recovering.

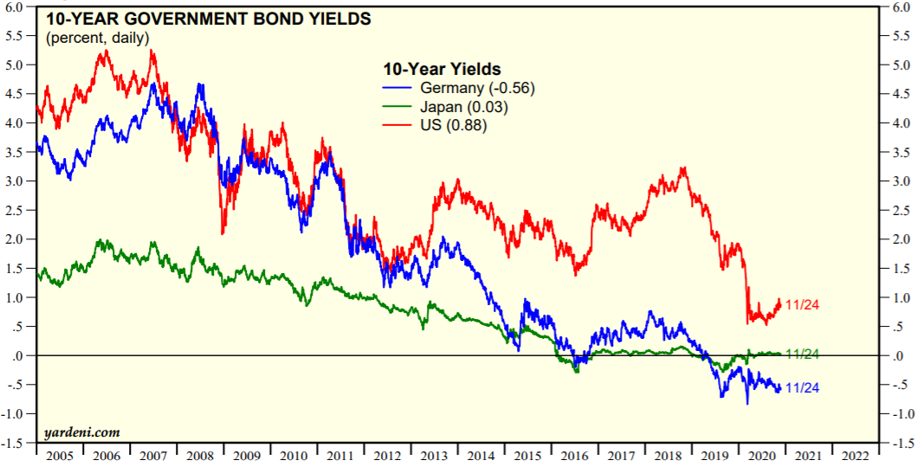

As a result of the combination of monetary stimulus and hopes of a cure for the virus, U.S bond yields increased much more than other economies such as Germany and Japan (Fig 1) during November, reflecting the prospects for real economic growth to recover at a faster pace.

Figure 1. 10-year government bond yields. Source: Yardeni Research

As fixed income strengthens and returns are close to 1%, this more positive scenario also creates an environment that favors the weakening of the Dollar against the main currencies (Fig 2). In line with the monthly report for November, the USD trades influenced by the effect of the US economy under President-elect Joe Biden’s administration.

Figure 2. Dollar Index. Source: TrandingView

After the go-ahead given by President Trump for the beginning of a peaceful transition of power, a period begins in which the U.S dollar will be priced under the perspective of the risks of an uncontrolled and damaging trade war that could occur under a second term of the Trump presidency would be greatly reduced. Furthermore, given the appointment of Janet Yellen to the United States Treasury Department, the changes to a second economic aid package in the first months of 2021 are even higher, due to its inclination towards the dovish stance.

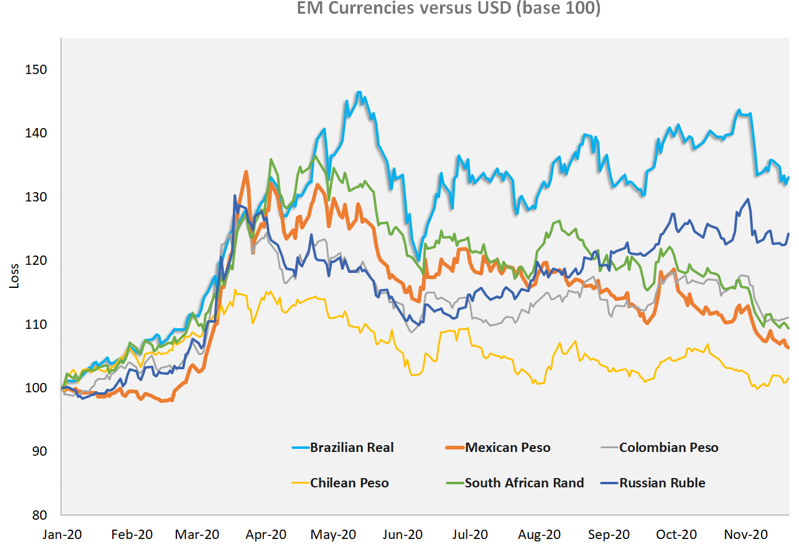

The preparation for a friendly presidential transition also echoed among the currencies of the main emerging economies, which saw their demand grow with the increase in the in-flow of foreign capital, contributing to the increase in investments and financing for current account deficits. The recent appreciation of currencies such as the Real and the Mexican Peso (Fig 3), should also gain an extra boost from the oil market, which also had its hopes renewed with the prospect of a more heated demand while the lockdown measures reduced and vaccines become widely available.

Figure 3. Emerging currencies versus the U.S dollar. Source: Bloomberg

The Euro and the British Pound are also expected to continue to gain ground against a weaker dollar, however the support of this appreciation will depend much more on domestic factors, such as economic recovery (Fig 4) and the curb of the second Covid-19 waves and above of all, if the European Union and the U.K will finally reach a final agreement for Brexit, which has a final date set for December 31.

Figure 4. IHS Markit Eurozone Composite PMI. Source: IHS Markit, Eurosat