Introduction

Hedging the currency risk generated by a global business’s anticipated future cash flows can be a bewildering task. Uncertainties inherent in revenue and cost projections, as well as the complexity of the foreign exchange (FX) market and related derivatives, can all contribute to concerns about the efficacy of hedging strategies and their activities. Yet, a well-constructed cash flow hedging program is worth the investment of time and effort.

A corporation's valuation is based on the size and stability of its future cash flows, so if it can reduce its earnings volatility, it will increase its valuation and access to capital.

For global businesses, FX hedging of cash flows is the key to avoiding sharp swings in earnings, and companies that do a poor job of managing FX risk may suffer significant volatility as a direct result. Even among the largest corporations, it is not uncommon to hear a CEO or CFO blame the quarterly earnings miss on movement in the currency markets.

How it works

Well-managed companies forecast their consolidated revenues and expenses 12 months out or more (including intercompany arrangements and accruals, and significant tax bookings). This facilitates planning for growth, managing liquidity, and other basic business operations. To account for local currency (LC) income and/or expenses, the FP&A group must set a "planning rate" or "budget rate" - the rate at which the company expects to convert LC to its functional currency (FC). Obviously, FX rates are volatile, and a planning rate set today will be unusable the very next month, unless the company has a way to reduce the volatility of their effective rates.

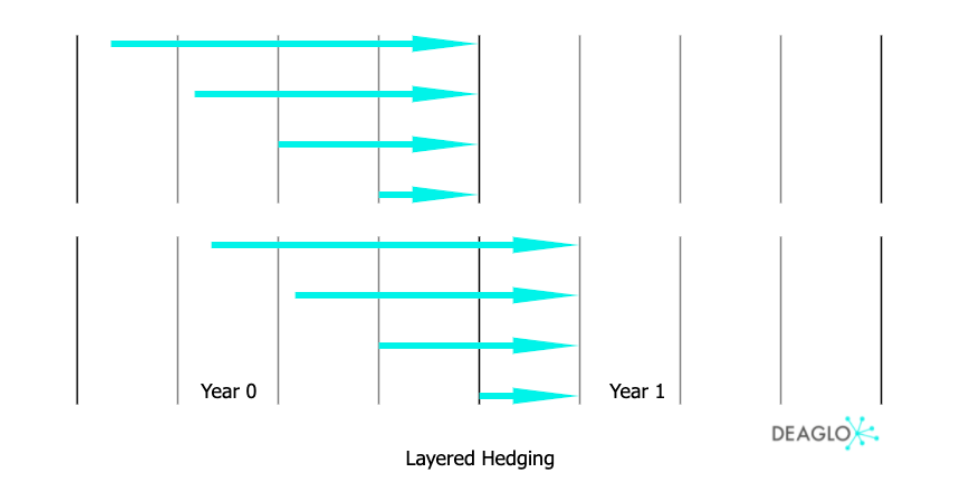

Entering a year’s worth of hedges at one time means all the transactions will be based on a single, potentially anomalous spot rate. Hedges established only at the beginning of the year cannot respond to changes in forecasts, and periodic evaluations of exposures and derivatives, as required by ASC 815/IFRS 9, could expose some hedge ineffectiveness as the year progresses.

By forecasting net LC out 12 or 18 months, and hedging the correct fraction of each forecast every month between the present and the expected cash flow, the effective rate for each period will be a smoothed average of the prior 12 or 18 months forward rates.

This is called "layered hedging". The effective reduction in volatility can be as dramatic as a 70% range reduction for a 12-month program in G-7 currency pairs. This allows a company to set planning rates confidently and know that its future cash flows as measured in FC are stable.

Additional advantages

Many firms eschew hedging because they do not feel that they can adequately forecast many months ahead. The very nature of layering means that the finance group will have 12-18 opportunities to adjust the forecast (and thus layer size) as new data becomes available. Hence, it is very flexible.

Additionally, many CFOs appreciate the ability to adapt a hedge ratio depending on macroeconomic conditions. The hedge ratio for each layer can be adjusted up or down depending on the CFO’s predilections.

Results

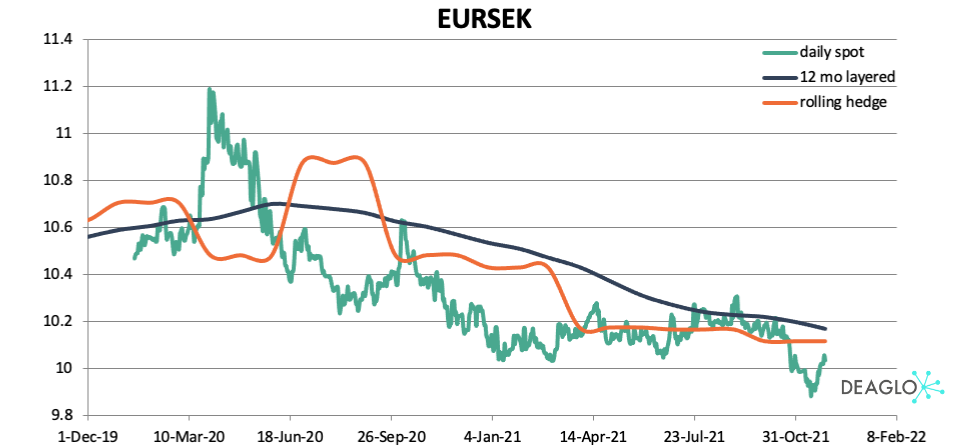

The following represents how layered hedging would have worked over the past five years for EURUSD. The volatility was reduced from 1.43%/month to .53%/month, a 63% reduction.

How do you implement it?

While 80% of organizations use spreadsheets for FP&A, the Association of Financial Professionals warns, “attempting to do a rolling forecast and hedge for a multimillion-dollar company in Excel is almost impossible.” Spreadsheets are prone to errors, broken links, and erroneous formulas. As a result, finance spends more time fixing the tool than fixing the problem.

Deaglo provides a dedicated program that:

- Allows for any hedge horizon or hedge interval

- Forecasts updates whenever they are available

- Provides the ability to do early drawdowns for intra-month liquidity, which is very important.

Additionally, many firms will want to complete the FX risk management solution with a balance sheet hedging strategy. Having a cash flow hedging solution that is tightly integrated with its balance sheet hedging is critical to avoid over or under-hedging, as well as conflicting forecast hedges with fair value hedges.

Deaglo - Next Generation FX Risk Management

Deaglo is an FX risk advisory firm. Our goal is to educate and empower investors and their finance teams to make more effective decisions around their cross-border investments.

How can we help you? Our in-depth hedging analysis allows managers to first quantify what their FX risks are. We then compare the effective performance of the different hedging strategies over multiple FX market environments using Monte Carlo analysis, before providing the manager with the tools they need to clearly communicate the FX strategy to internal and external stakeholders and the effect it may have on their international investment returns.