Using forward contracts to lock in a future rate is a common, well-accepted form of risk management. Forward points vary with the currency pair, and so sometimes (depending on whether you're selling the base currency or term currency, and the differential interest rates) you lock in a little profit, sometimes you lock in a little loss. The former is fine, you will do a little better than chance. The latter, however, begs the question: how much loss is too much?

Forward points can be quite egregious, particularly with emerging market currencies, and their associated high deposit rates relative to the majors. Long tenors exacerbate the problem. For example, hedging USDINR (selling INR, buying USD) the forward points for 18 months is= 483. At a current spot rate of 73.46, that gives a forward rate of 78.29. That means the hedger is locking in a substantial loss.

The forward becomes a catastrophic insurance policy only, as it protects the hedger if the spot rate rises above the (unlikely) forward rate. If the spot rate ends up more advantageous than the forward rate (which it will do more often than not), he'd have been better off not hedging. The question is, how do you quantify this relationship and decide to pursue other hedging alternatives?

If we accept common practice and model spot rate movements with a normal distribution using the current spot as the mean, and the volatility as the standard deviation it makes this problem tractable. It's a straightforward calculation (using the cumulative distribution function) to determine the probability of the spot rate ending up above or below the forward rate.

Let's analyze two examples.

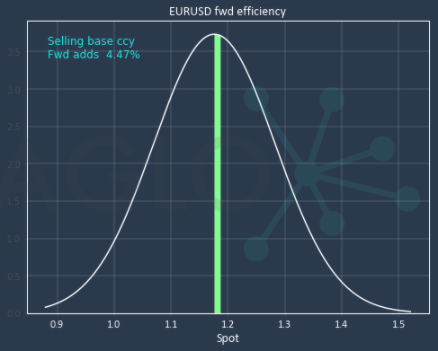

Let's first look at EURUSD, where the hedger is selling EUR and buying USD, the forward points are smallish, and in the hedger's favor. With a spot rate 1.1784, an 18-month forward rate of 1.1932, and volatility of just 8%; using a forward contract locks in an additional 4.47% more value than chance.

This is a small but clear benefit. The decision to hedge is easy.

On the other hand, when the points are against the hedger, the decision is harder. Let's analyze USDMXN, where volatility= 15%, and fwd points = 14,196 (6.7% at current spot of 21.42), selling MXN forward 18 months. We're selling MXN, buying USD, and so the hedge locks in a loss.

Using our methodology of plotting the forward rate on the distribution and measuring the cdf, it becomes clear just how poorly this hedge performs.

The forward rate is so far above the current spot (the middle), that there's only a 40% chance of it ending up further away than the forward rate. Put another way, 60% of the time the hedger would have been better off not hedging! It's time to explore other hedging alternatives (e.g. options).

Because every currency pair is different, and hedgers may be on one side or the other (i.e. selling the base or selling the term currency) each case will be different and require the appropriate calculation to determine the effective "insurance value" of the forward contract. It's easy to believe that using forwards to lock in a future value is good risk management, but that's not always the case.

For a free consultation with our advisory team on your exposure, Contact Us, or read more about Our Solutions.