There is no question that CFOs at Private Equity (PE) firms are polarized in their stance towards hedging foreign currency (FX) exposure. There are CFOs implementing meticulously planned strategies and policies, which are re-evaluated annually or even on a quarterly basis. On the other hand, there are seasoned CFOs that pay little or no attention to their FX exposure and have no policies in place to combat these potential currency risks. However, the industry is starting to become more aware of foreign exchange (FX) risks and are showing a keenness to learn from past lessons.

In contrast to the corporate world where it is deemed essential to have protective policies in place to ensure margins are secure, many CFOs at PE Firms have decided to hide away from the decision to manage their FX exposure. This is partly due to PE as a general industry and it being difficult to pinpoint exact future exposures as cash flow is a dynamic variable, and partly due to the view that risk management will only negatively affect returns.

So where are PE firms exposed?

- Portfolio Risk - any local valuations of international investments that the firm has in their portfolio will need to be converted and revalued in the firms base currency along with any foreign dividend payments.

- Transaction Risk - as the firm adds new portfolio investments, provides follow on financing and exits others, there will be a marked change in the aggregate FX exposure of the fund.

- Closing/Due Diligence Risk - the exchange rate can be effected in the time it takes to approve a transaction, call capital and deliver funds.

- Operational FX Risk - the PE firm or their portfolio companies may have their own FX risk through international office costs or payroll to import/export.

This disregards the possible exposures that may arise from a foreign investor and management fees. Nevertheless, it shows the direct exposure that will typically befall any PE firms that are engaging in international transactions.

What are the current FX risk management practices?

In the face of inadequate hedging solutions - PE CFOs had cited the following strategies:

- Seeking out natural hedges *e.g. Investing in companies whose revenues and liabilities do not present a currency mismatch, or selecting businesses that generate U.S. dollar revenues and local currency costs.

- Identifying portfolio companies with growth rates that offset local currency depreciation, and/or underwriting for substantial local currency depreciation.

- Hedging only short-term cash flows.

- Disbursing cash in tranches to spread currency risk over time.

So should hedging be considered?

A Fund Manager's job is to, where necessary, take the risk to increase returns and mitigate risk to protect returns.

Protecting these returns against both the known and the unknown - Sterling lost 20% of its value in the four months following the BREXIT referendum, in 2018 when President Trump doubled down on tariffs the Turkish Lira lost 94% against the US Dollar. It's easy to look at geopolitical events and chalk them off as one-offs. However, foreign exchange volatility is very much a constant.

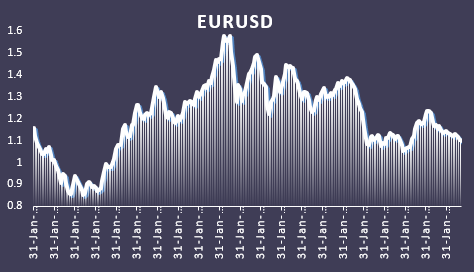

Looking at the EUR/USD currency pair over the past 20 years, it has shown an average swing of nearly 12%. Including at least 1 movement of over 10% the equivalent of every 6 years.

The Solution

While PE funds continue to invest their capital on a global basis and engage with multi-national companies, FX will continue to pose challenges. It's important to understand the constant nature of FX risk and make a decision on the approach on an individual basis and remember that you cannot insure yourself against currency volatility after the event.

At Deaglo Partners we provide tailored solutions for the next generation of FX risk management which provides flexible solutions to unique problems. Learn more about our services here.