Jan, 2021

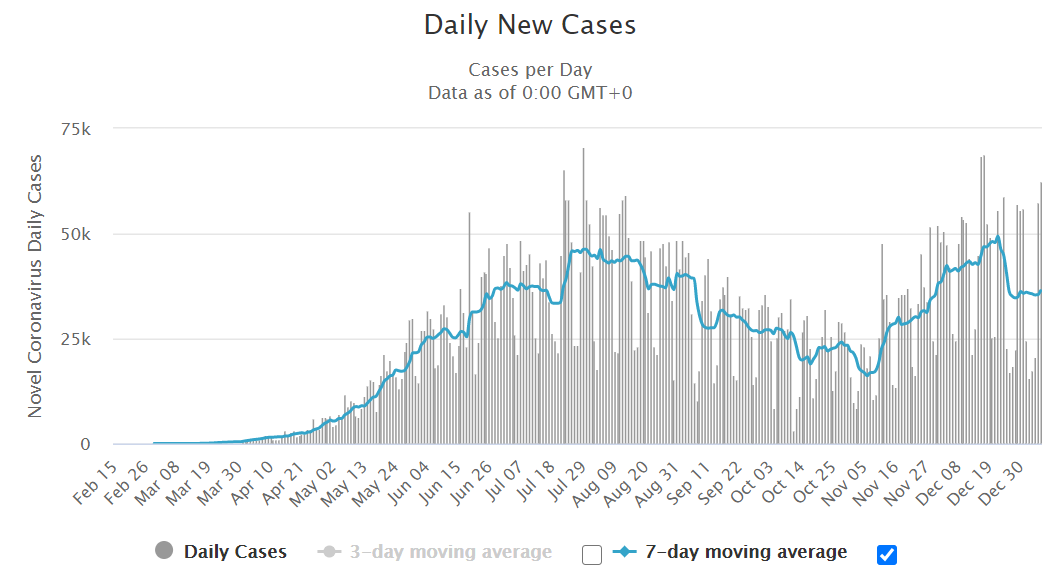

The recovery in economic activity in 2020 is welcome news for a country trying to shake off a tragic year as Covid-19 continues to claim thousands of lives. However, as local epidemic curves and hospitalizations show an upward trend (Fig 1), it is difficult to predict if Brazil will remain as one of the front runners in the global economic recovery from the pandemic shock through 2021.

Figure 1. Daily new cases in Brazil

Source: Worldometers

At the beginning of the spread of Covid-19, the federal government promptly designed one of the strongest stimulus packages in Latin America, providing fiscal support worth about 12% of GDP; which helped to protect vulnerable households and limit long-terms scars. At the same time, Banco Central do Brasil (BCB) has slashed its benchmark interest rate (Selic) by 250 basis points in order to provide liquidity support.

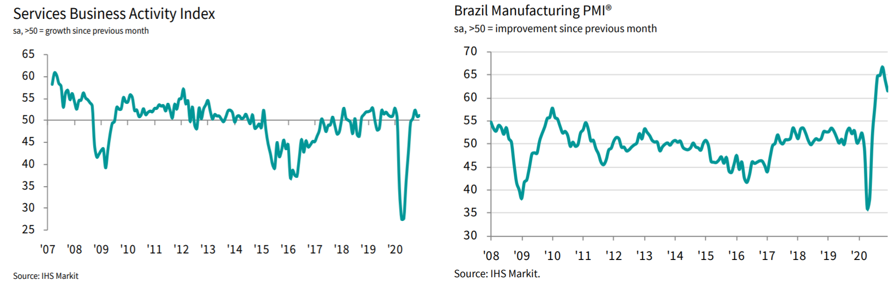

As a result, economic activity in the country began to improve in the third quarter of 2020. Pandemic-control measures were loosened somewhat, fiscal and monetary stimulus continued, and external demand picked up. As of December, services sector (Fig 2) had nearly returned to January 2020 levels, while manufacturing sector (Fig 3) signaled sharp increases in sales and production.

Figure 2. Services Business Activity PMI. Figure 3. Manufacturing PMI index

Source: IHS Markit

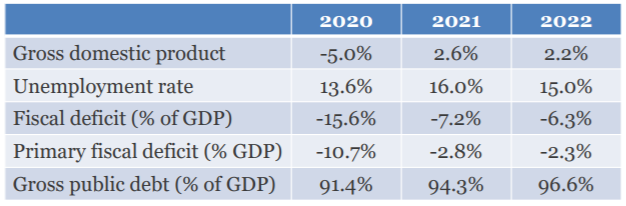

However, the pandemic crisis will nonetheless cause GDP to drop by 5.0% (Table 1), but the country should experience a rapidly recovery in 2021 and 2022. That can be considered a fantastic performance, since its major peers in the region will experience an even deeper contraction. For instance, Mexico, Colombia and Chile will shrink 9.2%, 8.3% and 6.0%, respectively.

Table 1. The economy is recovery

Source: OECD Economic Outlook

As mentioned, monetary and fiscal policies have both been proactive during the pandemic; however, some side effects and concerns have already started to appear. First, the consumer price index (IPCA-15) climbed 1.06% in December and finished 2020 at 4.2% (compared to 3.91% in 2019). Rising prices for food at home (2.6%), gasoline (2.2%), electricity (4.1%) and airfares (28.3%) were noteworthy. This current inflation will likely make the central bank more cautious in easing rates further.

Second, the country will end 2020 with a high government debt-to-GDP ratio of around 92%, and is expected to remain high in the near to medium term, according to OECD. The challenge for fiscal policy is great.

Against this backdrop, the rise in Covid-19 infections and increasing concerns over fiscal health remain as major sources of overwhelming stress in the price-action for the Brazilian real (Fig 4). This market narrative is expected to continue to pressure the BRL at least in the near-term. Meanwhile, Brazil’s Central Bank will continue to intervene (for example rolling out currency swap contracts) in an attempt to smooth market volatility.

Figure 4. Historical USDBRL spot rate