In this article, you will understand the main differences between deal-level hedging vs. fund-level hedging, so you can choose the one that fits the best for you and your investors.

Choosing the right hedging strategy will empower you to stabilize your costs, boost your returns and invest with confidence in new regions.

- Why do investment managers implement hedging strategies?

- Deal level hedging

- Fund level hedging

- Warning, important considerations you need to know

- Main getaways from the article

Why do investment managers implement hedging strategies?

Investment managers implement FX hedging programs with the intention of stabilizing performance metrics for their investors. IRR (Internal Rate of Return) is one of the most relevant performance metrics of investment managers; therefore, one of their biggest goals is to establish hedging strategies that reduce the volatility of these returns (amid FX fluctuations), so they can present good results to their investors.Several managers aim to stabilize their expected cash flows and deploy active hedging programs based on the projected flows of individual deals, which can often lead to big differences in real vs model returns.

Despite having a certain amount of visibility over expected cash flows, in practice, we have witnessed that on many occasions, deals differ from their original models amid early repayments, interest defaults, and refinancings, which require managers to adjust their deployed hedging strategies time and time again.It is common among investment managers to raise concerns around the actual fulfillment of underlying deals in contrast to their hedging strategy, which is technically an obligation with the FX counterparty.

Choose the best fx hedging strategy to boost your returns.

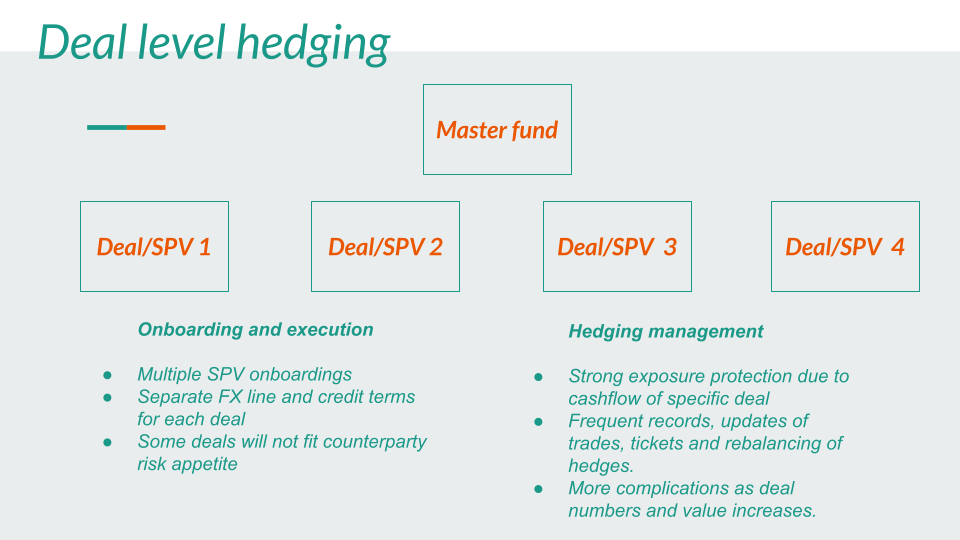

Deal level hedging

Management of hedging program:

Deploying tailor-made hedging strategies to specific cash flows would most likely provide accurate protection to the modeled investment case.

However, forecasts bring along intricacies in the management of the outstanding hedging program, tracking of these deals vs. hedges, and/or unwinding or adjusting any outstanding trade.

As the amount of deals increases, so does the complexity of dealing with an exponential number of trades and tickets booked across several legal entities.

Source: Deaglo

Onboarding and execution of new deals

When placing hedges at a deal level, investment managers aim to onboard specific SPVs that act as holding companies of the underlying deal or even directly the underlying borrower to cover the hedge.

This means that each loan that an investment manager would be looking to deploy, it will require a full KYC/KYB, AML, and credit assessment from the FX counterparty. This opens the broader activity to the risk that some deals will not necessarily fit the appetite of specific providers, given the fact that elements such as legal entity jurisdiction, underlying business/activity, solvency, and creditworthiness will vary on each deal, as well as the suitability of hedging.

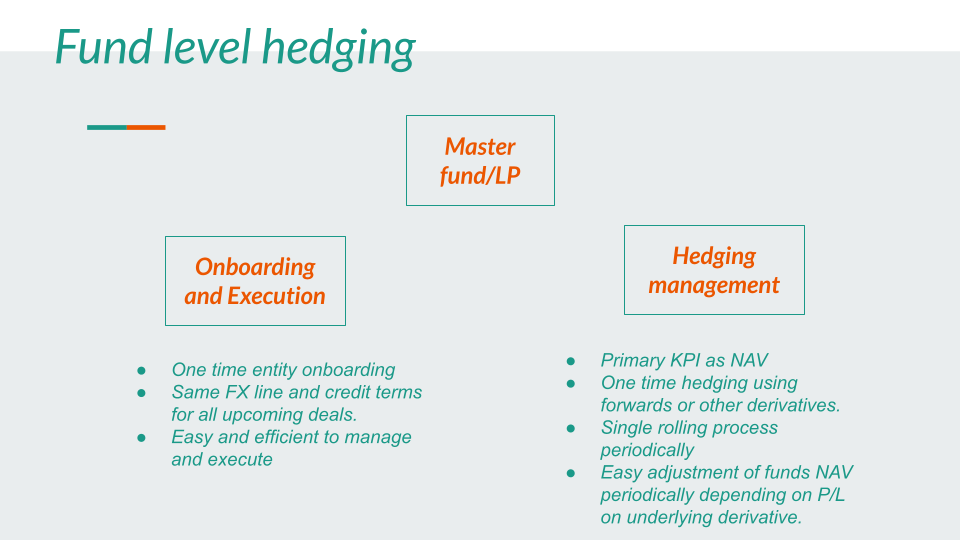

Fund level hedging

Management of hedging program

By tracking NAV as underlying exposure and defining a specific rolling tenor, the broader hedging program can be managed on a net exposure basis of the derivatives providing the hedge.

This brings simple processes for adjustment and rebalancing events, as well as the unwinding of positions that would have a similar process with the underlying realization of the cash flow event.

Onboarding and execution of new deals:

An Ecosystem level setup would require a single onboarding process and negotiation of a facility that would allow the Ecosystem to hedge any approved or upcoming deal instead of negotiating an FX line per opportunity.

This would guarantee that all deals will follow the same hedging strategy and deployment in an efficient fashion. The net derivative exposure will cover the portfolio level risk by identifying the NAV as a risk KPI. However, we have witnessed funds simplifying their hedging programs by placing cost or principal repayments as the metrics to match the derivative protection.

Source: Deaglo.

Important considerations

Despite considering either hedging program, it is important to also consider tax, regulatory and constitutional limitations to the actual hedging program. The realization of PnL at hedging operations needs to be closely revised by legal advice in order to avoid any issues in that regard.

The regulatory environment is constantly changing, but taking advantage of facing entities as non-financial counterparties (FX SPVs) would allow the fund hedging program to have flexibility in terms of collateral arrangements against its own counterparties while being classified as a Financial Counterparty would require tougher measures of margining and collateralization of derivative operations.

Finally, constitutional limitations could be fundamental when negotiating credit facilities as clauses around financial indebtedness or derivative operations could add complexities when negotiating FX lines for hedging purposes.

Main getaways from the article

- Investment managers can choose to hedge at a deal level or fund level depending on which performance KPI they choose to guide their hedging program.

- Deal level structures and tailormade hedging programs could provide better performing protection to specific deals.

- Ecosystem-level programs provide setups of economies of scale for high-growth managers and diversified portfolios.

- In terms of onboarding, ecosystem-level programs have an operational advantage against deal-level hedging.

- FX SPV structures are implemented across private equity and private credit managers to find synergies in terms of tax, regulatory requirements, and operational efficiencies. Either Ecosystem level programs or deal-level programs can benefit from these structures.

- Managers should seek legal advice before proceeding with defining hedging level program, its tax implications, regulatory requirements, and constitutional limitations.

Now that you know that it is time to choose which hedging strategy is the best fit for you and your investors.

In case you need help developing your hedging strategy Deaglo has got your back:

Our experts can code you a bespoke strategy based on your fund's underlying performance and requirements, empowering you to make more foreign investments in an easy and effective manner.