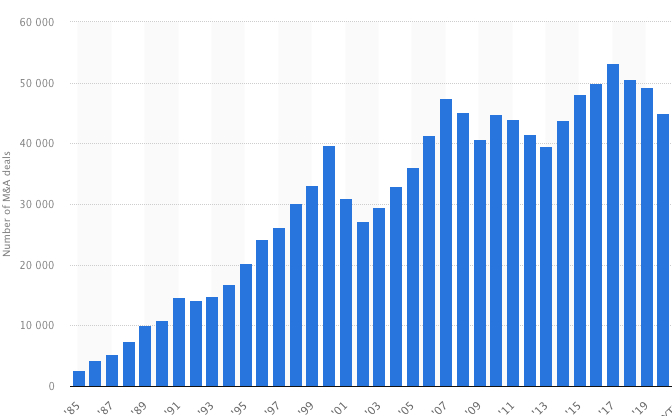

Cross-border M&A transactions have seen a meteoric rise in recent years, from 2,676 international deals in 1985 to a peak of 53,302 in 2018, according to Statista. Therefore, the need for innovation around deal contingent hedging has never been more.

There is no denying, as the world becomes smaller, global investment strategies are becoming the new standard in modern financial markets. Now fund managers are required to engage in cross-border transactions, exposing them and their investors to FX risk that can substantially impact the IRR of the fund/deal.

This is where deal contingent hedging plays a vital role. However, the currently accepted ways of executing a deal contingent hedge do not provide the flexibility that is required when working with a "contingent" transaction. That's why we came up with a new way to implement deal contingent hedges in an easier, cheaper, and more flexible way.

The challenge

Managers are expected to mitigate the FX risk that arises through their M&A, Infrastructure, and Real Estate transactions and it is very common to find managers implementing entry/exit hedging strategies trading OTC derivatives that provide 100% protection over the underlying exposure.

However, M&A and other types of cross-border transactions can have long and complicated due diligence processes and escrow holds which can last several months or even years, and these are not guaranteed to successfully close every time. The caveat with implementing vanilla forwards is the contingent aspect of these underlying transactions.

If the deal does not close or notionals change, and the fund manager hedged that position previously, the fund will end up with an unnecessary hedge which has no underlying deal to offset the PnL, thus exposing the fund to losses when unwinding or closing the hedge.

Ending up with a failed deal and an unnecessary out-of-the-money FX hedge which ultimately will create a drag on IRR is a scenario any fund manager wants to avoid.

When Deal Contingent Hedging Doesn't Work

There is always the possibility of leaving the risk unhedged. Depending on the currency pair and duration of the risk, the potential loss may or may not be acceptable. For example, USDCAD has fairly low volatility of 7% annually (Fig 1). If the performance escrow is also one year, the Value at Risk (VaR) for a $10M escrow (90% confidence interval) is $897k, roughly 9%. However, a deal involving USD and BRL is another story. With annual volatility of 19%, the same transaction size carries a VaR of $2.3M, 23%.

Options can sometimes be a viable alternative. For the USDCAD deal, a one-year ATMF option is 2.78% or 280k on the $10M deal. The same option for the USDBRL is far more expensive, 6.5% or $650k.

Fig 1

The alternative of last resort is deal contingent forwards. However, they are not practical alternatives for most transactions. Deal contingent hedges transfer the risk of the underlying transaction closing to the counterparty banks rather than either the buyers or sellers. Consequently, the banks will underwrite the risk of the deal closing. The principle of any deal contingent hedge is that it only exists and creates obligations on the parties if the underlying transaction closes. Consequently, banks will attempt to define "completion" in as broad a way as possible, while users will want as narrow a definition as possible.

A Deal contingent forward blends components from a vanilla FX forward and an Option in order to provide clients flexibility in their obligations. A deal contingent forward is a derivative contract that is placed before closing the transaction, locking in market conditions and a forward rate, although it fades away without any payment or obligation if the acquisition does not close. Long story short, the managers transfer the risk of the transaction closing to the bank, by embedding a portion of an option premium into the forward rate. These premium allocations vary depending on the complexity and quality of the underlying deal which oscillates between 15%-60%, making it very difficult to price on a case-by-case basis and making it more challenging for smaller market participants. In market conditions with high levels of volatility, these hedges become more expensive given the relationship between premiums and vol.

Deal contingent forwards have become significantly popular in the alternative space, especially in buyout and infrastructure strategies as it gives managers the flexibility of walking away from the hedge if the acquisition fails to complete. According to an article in FX Week, experts estimate that 30% of PE transactions are hedged this way and that they predict a notable increase in the price of premium for these types of hedges. However, these are very lengthy and heavy processes that require several teams to overwork in tight timeframes to remove the FX risk as soon as possible. Structuring these deals can become very expensive, as usually banks require on-boarding, and will run credit assessments and due diligence on top of assuming the risk of the underlying deal. The complexity of these credit assessments and due diligence process makes it difficult to benchmark transactions or costs, and we haven’t even dug into tax advisors and lawyers. Lastly, parties will likely struggle with accounting for deal-contingent hedges; the gory details are left to the reader's imagination.

Despite the success that deal contingent forwards have represented for the industry, there are clear limitations in the current offering which translate into challenges for fund managers who are trying to optimize their risk management offering to investors.

Deaglo has positioned itself differently when creating strategies for clients as Ashley Groves, CEO sums up.

Here at Deaglo, we are open to new possibilities for investment managers in the way we offer and structure FX hedging solutions, led by transparency and efficiency as key pillars to deliver holistic hedging solutions to clients.

Deaglo's solution for deal contingent hedging

The core idea is to identify a basket of currencies that exhibit low variance relative to both currencies of interest. This way, if the deal unwinds or proceeds, the total value of the basket remains relatively constant to either currency.

At deal inception, the buyer's cash is converted at spot to the basket. If the deal concludes, the basket is converted to the seller's currency. If the deal doesn’t conclude, the basket is converted back to the buyer's currency.

Because banks will charge the client if a currency has a negative carry, the candidate currencies for the basket are those which exhibit a positive carry. For example, 'CNY', 'CZK', 'NZD', 'SGD', 'NOK', 'HKD', 'CAD', 'PLN', 'GBP', 'USD' are liquid, positive-carry currencies.

The method used for identifying the currencies to use and the weights to assign to each is constrained optimization. The weights must be constrained between 0 and 1.0 and their sum = 1.0 (in other words, no leverage). The optimization is a minimization of basket variance against both target currencies. Selecting the best optimization algorithm is non-trivial. Some optimization algorithms (e.g. BFGS) require knowledge of the gradient, or a computable Hessian (Newton). Some algorithms do not provide for constraints; others do not deal well with noisy data (spot history charts are the epitome of noise!) In the end, an SQSLP optimization method proved the most suitable.

One of the additional parameters to be determined is how far back to go when computing the variance. Too far, and the relevance fades, too little, and there's not sufficient data. Empirical evidence was used to optimize this parameter.

Implementation and results

One of the biggest advantages of the basket methodology is that it doesn't require any derivatives. The party with the potential obligation simply converts the notional amount in their home currency to the calculated currencies and weights. Cash converted to other currencies involves little to no spread, no credit underwriting, and no ISDAs.

The basket is usually held in a multi-currency account, and the currencies suggested will all be positive-carry currencies. However, as many banks do not actually pay positive carry, the same effect can be achieved if the client instantiated the basket using liquid government instruments (on-the-run US Treasuries, Gilts, Bunds, etc).

Depending on the duration of the hedge, updating the optimal basket and subsequent rebalancing of the portfolio may be desirable. Back-testing of many major currency pairs shows that weights remain fairly stable over several months, but if the duration is many months or years (as with a performance escrow), regular rebalancing is recommended.

Example basket weights for hedging USD and BRL are; HKD 22%, CAD 5%, USD 24%, and BRL 49%. Typical results for major currencies (EUR, USD, GBP, JPY) is a reduction of spot variance (i.e. no hedging) of 50-65%.

The weights remain fairly constant over backtest periods of 4-6 months. This means that rebalancing can be done as often as monthly, or as little as quarterly. For currency pairings where one is an Emerging Market, such as BRL, the results are similar but naturally larger in size.

For example, USDBRL monthly volatility is a little over 5%. Over the period from March 2021-July 2021, the spot moved between +4.7% and -7% (Fig 1). The basket variance for both USD and BRL remained under 3% during the same period.

For the major currencies, the basket method will likely be the best alternative, as the variance is far less than the comparable option premiums. For the emerging markets, a careful evaluation of variance and options premiums should be carried out before selecting a method.

Smart contracts

One of the requirements for the use of basket-based deal contingent hedging is that both parties must accept the concept. The buyer must accept the risk that if the deal is not completed, the amount of home currency returned from the basket may be several percent less than the initial amount (it could be more, too). Likewise, the seller must accept the amount of their home currency received if the deal is completed will depend upon the value of the basket at the end of the contingency period. This may be several percent less than the amount that would have been obtained at the original spot rate (it could be more, too).

One elegant implementation of basket-based deal contingent hedging is to use smart contracts. Smart contracts are simply programs stored on a blockchain that run when predetermined conditions are met. They typically are used to automate the execution of an agreement so that all participants can be immediately certain of the outcome, without an intermediary’s involvement, cost, or time loss. They can also automate a workflow, triggering the next action when conditions are met.

Once both parties decide to utilize a smart contract, a program is written that incorporates the agreed-upon terms. One of the first actions would be the conversion of funds to the basket currencies. An intermediate action might be the re-balancing of the basket. The last item would be determined by the contract conditions not being met, and the basket converted back to the buyer's currency and released to them, OR conditions are met, and the basket is converted to the seller's currency and funds released to them.

Having a self-executing contract running on the blockchain (typically Etherium) has several benefits.

- Speed: Once a condition is met, the contract term is executed immediately.

- Simplicity: No paperwork to process, no fees, and no time spent reconciling errors.

- Safety: Because records of transactions are encrypted and shared across the distributed .ledger, hackers would have to alter the entire blockchain to change a single record.

There are some downsides which should be considered as well:

- Smart contracts are almost impossible to change. Any errors in the code will be time-consuming and expensive to correct.

- While smart contracts seek to eliminate third parties, they will still be involved. For example, code developers will need lawyers to understand the terms to create the code.

- Lastly, contracts may have terms that are somewhat vague - you can't code vagueness!

Limitations

Deaglo’s proposal provides a cost-efficient solution for managers that look to hedge their FX risk for entry/exit strategies showing competitive advantage against traditional deal contingent hedging solutions.

However, there is no such thing as a free lunch in FX, and deal contingent hedging is no exception. Thus, it is important to flag the limitations as conditions may vary across business cases.

As mentioned before, optimal currency baskets can’t be guaranteed for all currency pairs, as market conditions will not allow in every case to provide an efficient hedging harmony through this methodology. In addition to this, despite the theory suggesting that carry should be a given for holding cash in a deposit account, different counterparties that provide multi-currency accounts or escrow solutions don’t necessarily pass carry to clients, which may vary the workings and outcome on the hedge for high-yielding currencies.

For this solution to work, it is imperative for both parties to agree and participate in the hedging approach as the deal will require counterparts to share the risk, unlike deal contingent forwards which are placed unilaterally. Nevertheless, the transaction size and market liquidity may also raise significant challenges, as the bigger the deal and depending on the optimal basket, managers may require to buy large amounts of illiquid currencies which may increase the cost if not managed properly.

For example, let’s take the proposed currency basket for hedging USD and BRL we discussed in previous sections and assume that we have an underlying deal size of USD 100 million.

To execute this specific hedge, we require to sell the defined USD amounts in exchange for the currency basket. The USD and CAD allocations don’t seem to be a challenge given the fact that USD does not require any exchange and CAD 5 million should be straightforward to execute with any bank.

However, on the BRL side, we must take into consideration that deliverable FX requires a licensed counterparty or partner in Brazil and we expect a significant slippage on a USD 49 million notional during execution, due to less liquid conditions than what we usually find in the developed market or currency pairs. A similar trend we could expect with HKD as not all banks or liquidity providers cover emerging market currencies, although the notional amount halves the exposure of BRL. This challenge grows with the underlying deal size, especially with allocations that require vast sums of emerging market deliverable cash. At Deaglo, we encourage our client to define best execution KPIs ahead of placing any trade execution to guarantee a smooth and predictable hedging delivery.

Deaglo’s approach is a proven, unique, cost-efficient, and effective solution for fund managers that are looking to hedge on a contingent basis. The efficiency around documentation, due diligence, and the lack of derivatives provide a vastly simpler and transparent approach to traditional dual contingent hedging which usually represents a hustle and overturn for fund managers. Our unique solution is available for any fund manager or institutional investor. No two deals are the same.

Reach out to us to learn more about how your own cross-border transactions can be hedged using our Deal Contingent Hedging.