The number of Family Offices has surged in the past 20 years, as families start to take more control of their investing. These institutions wield the wealth and flexibility to be able to invest both large and small across the Private Equity, Private Debt, and Venture Capital spectrum.

Much of the increase in Single-Family Offices is driven by rising expectations around investment returns, a move towards more socially and environmentally responsible investing practices, and a reduction of third party manager fees.

As the world has become smaller, international investing has become a staple for Family Offices in the search for higher yields and reduced competition. As these portfolios are diversified, one of the largest concerns will be the FX exposure on the current and future returns.

58% of Family Offices identified risk management as a high priority in UBS’s Global Family Office report 2020.

Despite that the USD's preeminence as an international currency has been questioned due to the recent financial market crisis and changes in the dollar's value, the USD has retained its standing in key roles across critical areas of international trade.

From 2014 the dollar (Fig 1) began to escalate against all other major currencies for the first time since the turn of the century. At the time, the greenback made gains against the euro, yen, pound, swiss franc, Brazilian Real, and other global currencies amid expectations that the Fed would raise interest rates in the next year from historic lows, as central banks in Europe and Japan continued to take an easing approach.

However, the increments in U.S interest rates were not enough to reverse this trend, and US investors began to allocate capital abroad seeking stronger returns in emerging markets - a trend that continues still today. As the USD continued to strengthen, asset classes became cheaper, and investors seem to ignore the apparent risks associated with investing in emerging markets. Nevertheless, few predicted the recent volatility caused by the Coronavirus, with emerging markets getting hit the hardest (Fig 2).

The vast majority of investors (unless entering into a hedged share class) were left wide open to the recent volatility in foreign exchange rates and therefore may be facing a significant impact on their investment returns.

A key driver behind the dollar's recent strength is the perception of the dollar as a "safe-haven" currency amid economic and political turmoil. In times like these, having a solid risk management policy is necessary, to manage the current exchange rate fluctuations.

So with all this volatility in the market, a prudent Family Office would have at least considered the effects of hedging on their international portfolio.

However, Hedging foreign investments can be a complex and daunting task. Hedging instrument costs and efficacy depend greatly on market conditions.

For example, if hedging a deployment from USD into BRL, the large forward points work in the investor's favor, but if hedging BRL returns back to USD, forward points exact a toll, and option strategies may be considered. Option strategies come in many flavors; some designed to be simply cost-effective, others to attempt to extract yet more return.

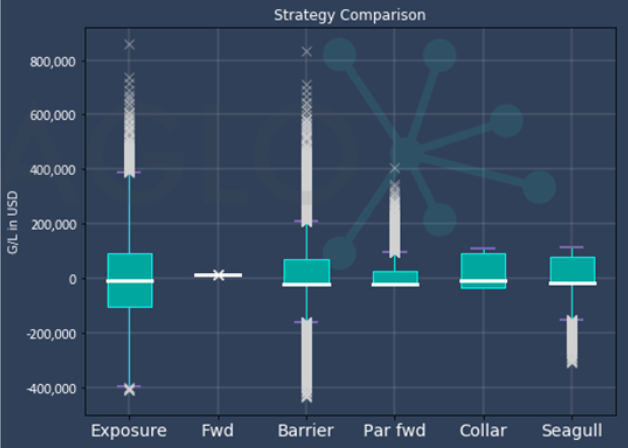

Evaluating option strategies cannot be done by simply examining a payoff diagram, as the likelihood of each spot level is unknown (and thus the expected value). Monte Carlo simulation of multiple hedge strategies is an effective method of evaluation and selection of option strategies. Displaying the results in graphical (Fig 3) form such as box or violin plots usually identifies a clear winner.

The investment horizon is often in excess of four or five years; well beyond the available tenors of most hedging instruments.

In this case, investors can borrow a technique used by corporates to hedge their forecast revenues or expenses a year or more out. The strategy is called layered hedging and consists of making fractional hedges each month or quarter in advance of the exposure. The net result is a hedged exposure using 8-18 layers, each at a different forward rate. The advantage of this technique is vastly-reduced volatility in the effective rate. Often, the volatility is reduced by 70-80% (depending on currency pair and number of layers).

Hedging is supposed to be planned and executed ahead of the investment, therefore, hindsight is not a strategy and sometimes the horse may have already bolted.

All may not be lost, a carefully considered option strategy may be helpful here, even if the disbursements have already started. The use of barrier options and other products can allow the holder both further downside protection with the ability to take advantage of any favorable moves.

We are living in extraordinary times and Family Offices are under extreme pressure to show returns where possible but preserve wealth at an absolute minimum. Understanding risk exposures is key to that and being prepared to act quickly and efficiently could mean the difference between positive and negative returns.

Remember, when it comes to FX risk in your portfolio, hope is not a strategy.

Contact Us, to learn more about how we have helped Family Offices to manage their FX risk and how we could help you.