Matheus Zani – FX Risk Management Consultant at Deaglo

Nick Smale – Partner at Brunel Partners

It's no great secret that the coronavirus crisis created major setbacks in the global economy, which led central banks across the globe to unleash synchronized monetary stimulus to support the economy. This action drove benchmark interest rates downward, in particular, in developed economies.

Coupling this with return compression across many asset classes in developed markets has led many international investors to seek higher returns in Emerging Markets, thus creating a greater opportunity for local Emerging Markets ¨EM¨ fund managers to raise capital overseas.

Brazil, being one of the most developed Latin American countries, offers considerable opportunity for higher returns, particularly as its Private Equity/Venture Capital industry has rapidly developed in recent years. For instance, in 2019, the total committed foreign capital allocated by the private equity and venture capital industries in Brazil was up 76% over 2011 at a record BRL 140.4 billion.

However, challenges remain.

| How do Emerging Market funds raise capital from international investors?

EM investment managers looking to raise money from international investors need to think carefully about how to approach the vast investor universe to focus their fundraising efforts on genuine prospects. The subset of investors that will consider country or region-specific EM funds is small relative to the total, and smaller still when split by asset class. It is important to understand how a product would fit within the overall portfolios of investors, whether it would form part of a global asset allocation approach and how it would be benchmarked. This is crucial in order to understand how best to market it, be it for absolute or relative alpha, diversification, ESG or other purposes.

Fundraising from larger institutional investors is typically a long process (12 months+) as investors will take time to understand not just the firm and strategy but often also the broader market. Lengthy due diligence processes are common with extensive data rooms and in-person country visits often a prerequisite – made harder by Covid related travel restrictions, which have only been relaxed by some investors.

| International investors like your fund and its strategy - what additional market-related challenges do you face convincing them to invest in your fund?

The original paradigm for emerging market investing was a story of capturing the “catch-up growth” as developing economies outperformed through following well-trodden paths towards economic growth and development. Whilst this has occurred to some extent (particularly in China), the paradigm has been widely discredited recently as political instability, commodity dependence, inflation, and currency weakness have led many EMs to underperform their DM peers. Investors aware of these risks will usually require higher return hurdles to justify investing in EMs. Importantly USD or other DM currency-based investors will want to understand the likely risk and returns in their currency. Previous approaches that were common of ‘not worrying about FX’ have been recognized effectively as being long EM currencies, which has not proven to be a profitable call in recent years. As most EM investment managers are not geopolitical or FX specialists, they justifiably focus their efforts on the things they can control within their strategy (stock-picking etc.). Nevertheless, being aware of these wider risks is important when speaking with international investors.

What can be (partially) controlled, effects of currency volatility!

Protecting against political or social instability, commodity price swings is very difficult if not impossible. It’s important to control what you can control.

Currency is affected by all of the above and will end up being a large factor in the size of your returns, as well as responsible for many deals not being reached.

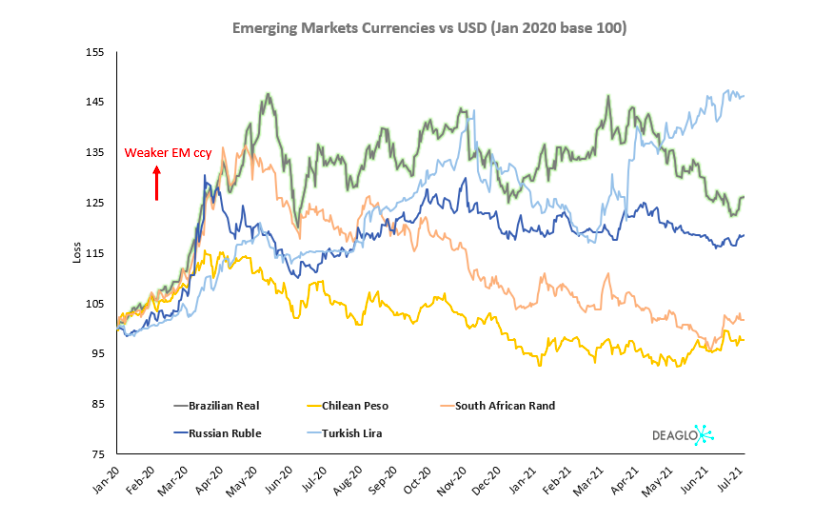

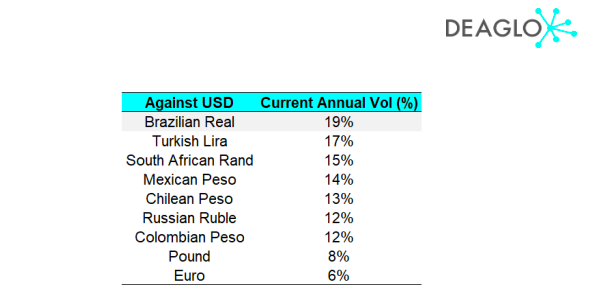

In the first quarter of 2021, (Fig 1), the BRL was one of the worst-hit currencies in LatAm, weakening around 20% against the dollar. Also, the current annual volatility (Table 1) for the USD/BRL pair is over 19%, which is extremely high related to other emerging markets and major peers.

Figure 1. Emerging Markets Currencies vs. the US dollar. Source: Bloomberg

Table 1. Current annual volatility

Looking ahead, volatility remains a distinct possibility and will continue to deter international investors, particularly those that look to make longer-term investments. Therefore, this environment underscores the importance of currency hedging strategies.

| Currency Risk Management

Usually, an investor/fund manager is exposed to foreign exchange (FX) risk over the whole investment project. Firstly, an investor commits to a total level of investment, which is cash called over time, i.e. a waterfall. This deployment in-country over many months to several years means the investor's currency will be converted to the fund's currency at different rates.

In this case, this currency conversion would be USD to BRL. The risk present during this phase is that an appreciating BRL reduces the amount of local currency that the USD investor acquires in the fund.

After the initial investment tranches begin generating returns in local currency (typically several years later), the harvesting phase begins. The returns are converted back to the investor's home currency before distribution (BRL to USD). This phase may also last several years. The FX risk during this phase is that a depreciating BRL reduces the amount of USD the investor receives.

Deaglo has created a simple and transparent way of determining, implementing, and executing FX risk. Effectively, it will substantially reduce risks for foreign investors and their international investments.

The hedged USD share classes aim to provide investors with a return correlated to the base currency performance of the fund by reducing the effect of exchange rate fluctuations between the base and hedged currency.

| To hedge or not to hedge

For a Brazilian alternative manager raising capital overseas and distributing locally, there are two main types of FX exposure, as explained earlier; Deployment phase: to eliminate functional currency depreciation risk. Harvest phase: to eliminate local currency depreciation risk. There can be a major benefit to hedging both phases.

Usually, there is a cost associated with placing a hedge on a currency (Bid/Ask +/- Forward Points, see Figure 2). However, there can be benefits to hedging currencies depending on the direction. In some cases, interest rate differentials will favor the hedger and these discounts can partially offset the costs associated with the other side of the hedge (we call this roundtrip hedging).

Figure 2. (a) Interest rate differentials. Source: Bloomberg

Figure 2. (b) Forward points annualized (%)

| Explaining Roundtrip Hedging

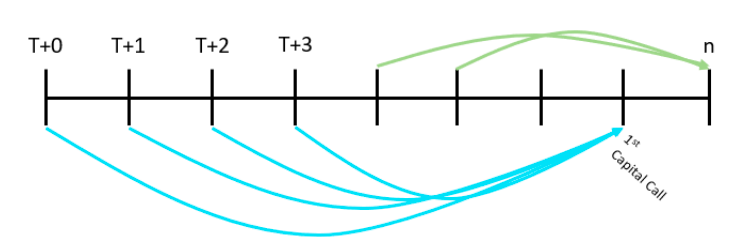

The essence of the Roundtrip Hedging strategy is the “layering methodology” (Fig. 3), which consists of hedging the correct fraction of each capital call and harvest forecast before the effective distribution of the capital. The fraction can be hedged monthly, quarterly or semi-annual, and starting one or two years before the effective cash flow. Thus, the effective rate for each period will be a smoothed average of the prior monthly, quarterly, and semi-annual forward rates.

Figure 3. Layering methodology

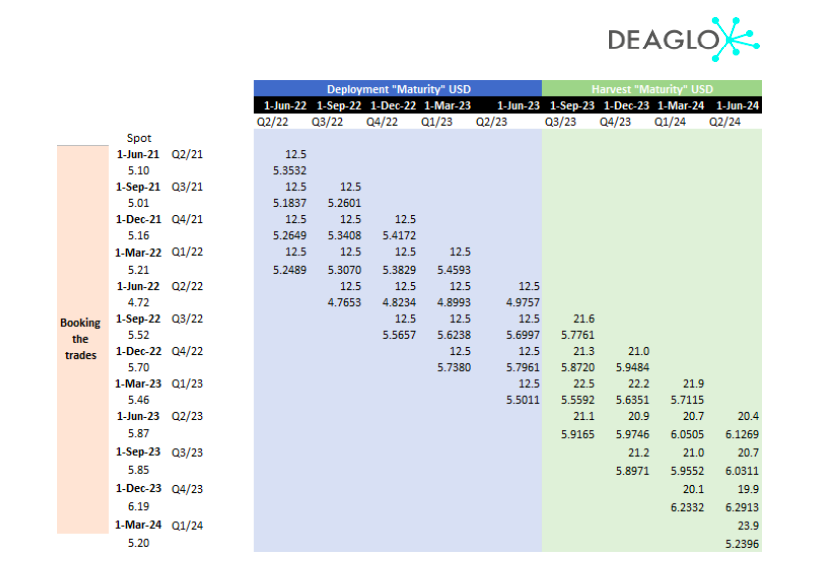

Figure 4 illustrates a hypothetical cash flow. In this example it expects a capital call amounting to USD 50M in June/2022, adopting a quarterly layering hedging program and one-year horizon out. The first layer is booked in June/2021, the second layer is booked in September/2021, the third layer is in December/2021, and the last one is in March/2022. For each layer it hedges 25% of the exposure. This is called "layered hedging". The effective reduction in volatility can be dramatic for the BRL.

Figure 4. Hypothetical PE fund’s cash flow. The figure shown above is for illustrative purposes and does not represent past or future performance for an actual product. There is no guarantee performance will match this illustration.

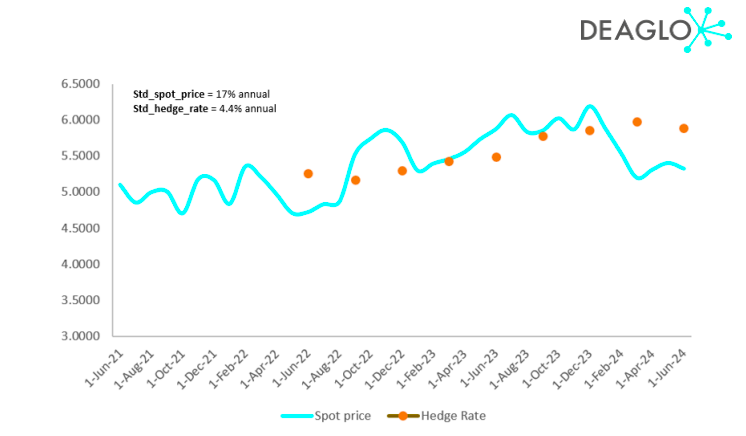

The difference in the behavior of the two exchange rates (Fig. 5), spot rate and hedged rate respectively, also highlights the effect it will have on the portfolio. With the layered hedging strategy, volatility is reduced by approximately 75%. The effects of currency on the hedged share class performance have been smoothed out compared to those of the unhedged class.

Figure 5. Example Simulation Hedge and Unhedged (does not predict future fund performance in any way)

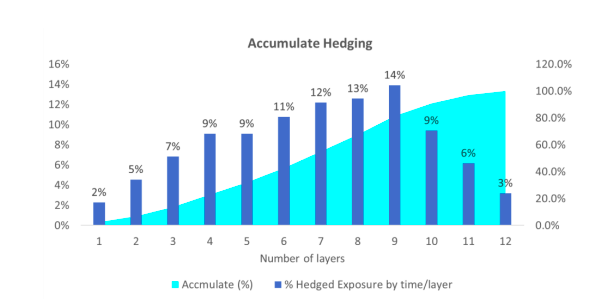

Another interesting feature of this methodology is that the cash flow is never fully hedged (Fig. 6), allowing General Partners (GP) to adequately forecast for many months. It is a very flexible strategy. Additionally, many GPs appreciate the ability to adapt hedge ratios depending on macroeconomic conditions. Hedge ratios for each layer can be adjusted up or down depending on the GPs predilections.

Figure 6. Accumulate Hedging. The cash flow is never fully hedged.

| Main benefits

Hedged share classes are capable of shielding investors’ returns against FX variation that can result in substantial losses. Thus, it allows GPs to reduce considerable uncertainty regarding the performance of a fund.

These are the main benefits:

1. Sharpe ratio of the hedged share class can be higher than unhedged share class

2. It can achieve similar (or better) IRR

3. It helps reduce or neutralize returns volatility

Below are the results of a simulation and analysis showing the performance of a roundtrip hedging strategy for a Brazilian PE Fund. The hedged share class had an IRR of 22.3%. Against an unhedged IRR of around 19.8% (Fig. 7).

In this instance, the hedged share class reduced the volatility in currency pairs by as much as 75% and brought the Sharpe ratio up 4x higher.

Figure 7. Example IRR Outcome (does not predict future fund performance in any way). The figure shown above is for illustrative purposes and does not represent past or future 11 performance for an actual product. There is no guarantee performance will match this illustration.

| Where’s the risk?

1) Black Swan event

A Black Swan is a metaphor coined by Nassim Taleb to describe events that are possible but could not have been predicted based on past evidence. From a mathematical perspective, the black swans or “fat tails” distributions are characterized by frequent small events and infrequent large events, which is the result of the combination of kurtosis risk and the risk associated with skewness. These fat-tail distributions pose several fundamental risk management problems.

Thus, the major downside of the layering strategy is that the exposure is never fully hedged, which leads the GP exposure to such events that can substantially impact the cash flow.

2) Margin Call

Implementing a hedging strategy can bring new challenges and even add unnecessary risk to companies if the strategy is not carefully analyzed and monitored, especially for those companies that have cash flow with little liquidity or seasonal liquidity.

In this sense, an unexpected negative variation margin of positions may introduce new risks to the company's cash flow. This is often accompanied by the need to post financial deposits (this requirement is also known as margin call) to cover negative positions, directly impacting the availability of the company's financial resources.

Moreover, every dollar posted as cash collateral or held as a buffer for potential daily margin swings incurs an opportunity cost of lost investment returns. Therefore, it is crucial to find FX providers who are willing to negotiate 0% collateral facilities. Given that many funds typically need to post between 5%-10% initial margin against their FX hedges, this can free up significant cash flow for their clients.

3) Interest Rate Differential

Each currency pair has a distinct hedging cost, made of the difference in interest rates between the two countries – domestic minus foreign. Hedge impact or “hedging cost”: it is priced based on the spot rate and the difference between the interest rates on the two currencies, therefore forward points may increase or decrease and thus affect the moneyness of the strategy.

| To Conclude

A perennial issue for investors in Brazil historically has been the volatility implicit in Latin America, particularly with regards to the currency. Better options to mitigate some of the currency risk and volatility could help GPs to achieve higher returns in difficult markets. The hedging strategies using forward contracts, along with the layering methodology approach, have the same mean IRR (or in some cases better) as the unhedged fund, as well as performing better in terms of Value-at-Risk and Sharpe ratio. In general, having the same mean IRR but lower volatility implies a better performing hedging strategy.