Who is responsible for implementing a hedging program?

If I had a nickel for every time someone asked my team who was responsible for a hedging program, I'd be a very rich man, admittedly not Bezos rich, but this is a very common question that local fund managers, whether they are focused on private equity, infrastructure, real estate, venture capital, among other theses, ask us.

The short answer? The General Partners (GPs).

In order to avoid foreign exchange fluctuations eroding investment returns in foreign currency by double digits, the use of hedging instruments becomes indispensable.

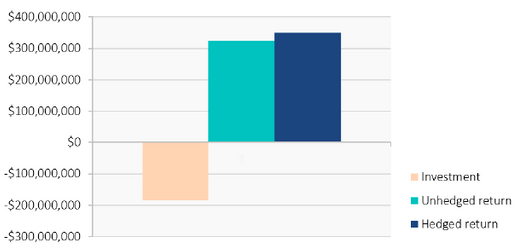

While many General Partners report that foreign Limited Partners are used to local currency volatility in emerging markets, our experience is that LPs get a sour taste after seeing 20% IRR in local currency turning into 5% in USD. It is also extremely difficult for Limited Partners themselves to deal with the high volatility and persistent exchange rate fluctuations of emerging economies.

For example, the Brazilian currency (BRL) suffered a 40% depreciation during the onset of the Covid-19 pandemic, and after 12 months, the currency still accumulated substantial losses.

Turning a blind eye to currency risk, as well as ignoring the fact that Limited Partners are increasingly demanding in wanting to add FX solutions to their portfolios, is a strategy that does not hold up over the long term. Thus, fund managers must seek alternatives to mitigate these idiosyncratic risks in order to harvest long-standing relationships with their investors.

Our focus (and challenge) here at Deaglo is to help fund managers around the globe, mitigate the impact of FX fluctuation on investment projects, while preserving metrics and delivering results to international investors.

To collaborate in delivering such results and indeed collaborate with the Private Equity and Venture Capital industries, we are constantly innovating and creating hedging solutions to address interest rate differential, bank spread, and liquidity risks.

Here are some practical lessons that we have learned alongside our clients:

- The best time to discuss hedging and the creation of a USD hedged share class is before the roadshow. Thus, managers have enough time to structure, learn and present the employed strategy to potential investors;

- Discipline and engagement of all stakeholders involved in the implementation of the hedging strategy are crucial. All financial teams must buy in the strategy;

- Regular updates on cash flow forecasts (capital calls and distribution calls) are key to accurate hedged exposure;

- Adoption of technological tools and sophisticated mathematical models to simulate the effectiveness and performance of the selected hedging strategy will give you more certainty around the most effective hedging strategy;

- Always seek the "best execution" and not the cheaper price with your financial partners to execute trades, including banks and brokers. Plan the execution well in advance. Negotiate collateral terms and spread under stress and pressure can lead to suboptimal outcomes for investors;

Foreign exchange rate fluctuations and volatility will always be present and they are unpredictable. Delivering solid results for foreign investors requires discipline and adopting a robust risk management policy.