Outlook

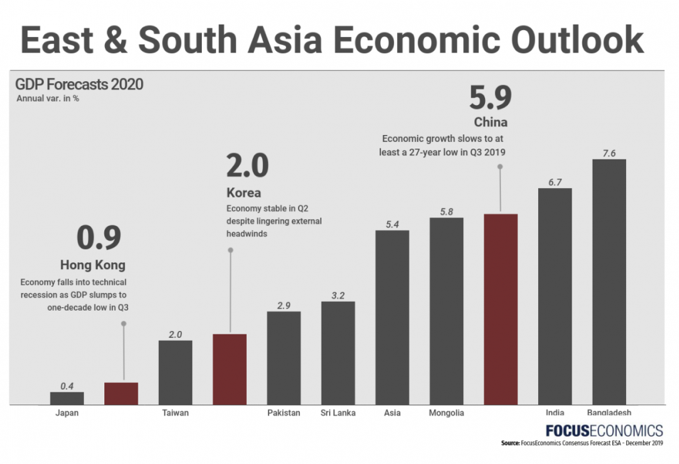

The East Asian economy will decelerate further in 2020 as these export-driven economies continue to face headwinds from the China-U.S. trade tensions. Inflation accelerated to 3.3% in October from 2.6% in September, probably mainly due to the outbreak of African swine fever in China.

The South Asian economic growth is expected to accelerate (on average, not including India) in 2020. Sri Lanka’s economy should pick up steam next year after a tough 2019. Inflation accelerated to 4.7% in September from 4.0% in August. Regional inflation is expected to accelerate even more in 2020, driven by the aforementioned economic growth.

FDI flows

Foreign direct investment (FDI) inflows to developing countries in both East and South Asia rose by 3.9% to US$512 billion in 2018. Asia remains the world’s largest FDI recipient, absorbing 39% of global inflows in 2018, up from 33% in 2017. Inflows to China – the largest developing economy recipient – increasing by 4% to an all-time high of $139 billion, accounting for more than 10% of the world’s total.

South-east Asia received a record level of investment, up 3% to $149 billion. Manufacturing and services, particularly finance, (including the digital economy), continued to support inflows to the sub-region.

Country-specific commentary

China

The longer-term picture is one of strength; the current account has recorded a surplus in every year since 1994, and the capital account has only recorded two deficits in the last 20 years.

However, economic growth has slowed to a 30 year low in Q3/2019 as the domestic economy reacted to the trade war with the United States. Manufacturing activity was weak in Q3, mostly reflecting subdued external demand. China's Purchasing Managers' Index (PMI) came in at 49.8 in September, the fifth straight month of contraction. Perhaps related, China cut its medium-term lending facility by 5 basis points.

Hong Kong

The economy contracted sharply in the third quarter, as widespread protests crippled activity. Purchasing Managers’ Index (PMI), dropped to 39.3 in October from 41.5 in September—the lowest reading since November 2008. Retail sales volume plunged 25.3% year-on-year in August, a significant deterioration from July’s revised 13.1% contraction (previously reported: -13.0% year-on-year). Augusts' numbers reflect the sharpest annual decline in retail sales since current records began in 1981. Private consumption and fixed investment fell, tourist arrivals plummeted, and exports were also down markedly as U.S.-China trade tensions have not abated.

The Hong Kong Monetary Authority cut its base rate by 25 basis points to 2.00% on 31 October in response to all this bad news. Growth of 0.7% is still expected in 2020, which is down 0.7 percentage points from last month’s forecast.

India

The country's $2.7 trillion economy is in the midst of a deepening slowdown driven by waning consumer consumption. Bank lending growth slowed in September to the weakest pace since October 2017, and there is an ongoing credit crunch among non-bank financial lenders.

In response, the Reserve Bank of India has slashed interest rates in recent months and is widely expected to cut rates again at its 3–5 December monetary policy meeting to prop up economic growth.

In response to all this, Moody’s downgraded its credit rating outlook for India from stable to negative in early November, citing concerns about growth headwinds and fragile government finances.

Taiwan

The annual economic growth of this $500B economy accelerated for the second consecutive quarter. Contributions were mainly increased government spending, with some contribution from private consumption. Exports of goods and services also increased at a robust pace, defying the wider global trade slowdown.

Turning to Q4 2019 and 2020, however, the economy seems set for a slowdown. Tourist arrivals from mainland China were down almost 50% in September compared to the same month a year earlier, which was due to the Chinese government’s decision to curb tourist visits to Taiwan amid poor cross-strait relations. Manufacturing PMI fell in October, as it has for 9 of the last 10 months.

Currency/FX

USDINR reflects the volatility of nearly 2%/month, almost twice that of the other regional currencies.

There are headwinds in almost all of the countries included in this report, due to political unrest in Hong Kong and elsewhere, slowing world trade, and specifically the US-China trade war. Still, forecasts indicate mid-single-digit GDP growth, high compared to the RoW.

Do you have questions about Asian currencies and how they could affect your business or investment? Reach out to one of our consultants today.