How can a hedging strategy allow a firm to enter new markets with confidence, expand its global operations and scale safely with more comfort and clarity?

Along with the excitement and anticipation of venturing out of a company's local market, comes hurdles that must be overcome to have a chance at global success.

Foreign Exchange (FX) risk is one of these hurdles, and some would argue the biggest. When businesses are expanding into international markets, the number of currencies in their operations tends to increase, thus exposing their new venture to exchange rate fluctuations causing FX risk.

But, how much can a currency exchange rate fluctuate?

In short, A LOT.

For instance, Brazilian Real weakened 40% against the dollar in 2020, making it the worst-performing currency in the world, not a sought after title! This is not a lone example, the South African Rand also saw its value decrease by 21%. More?

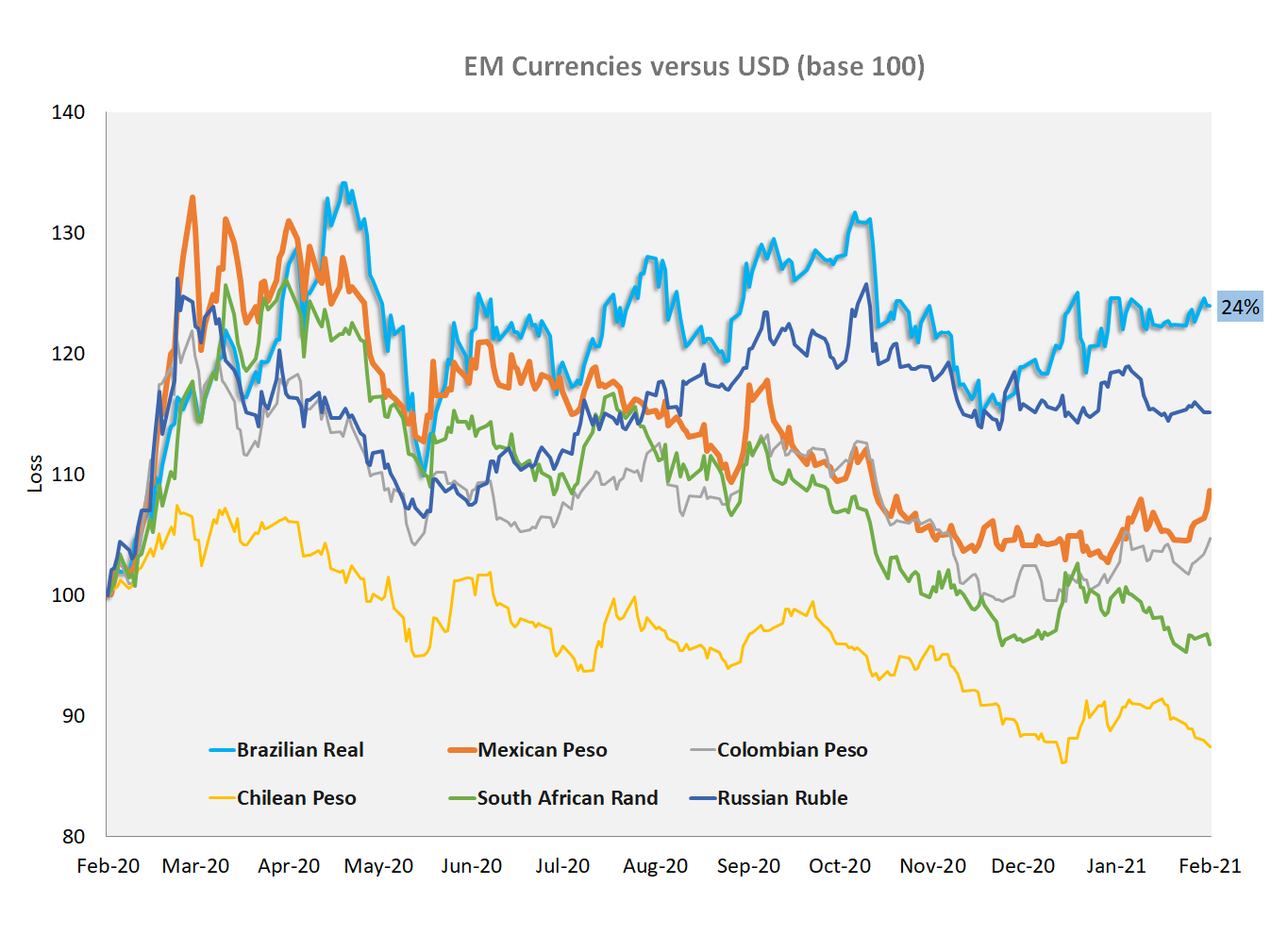

The seasonal data (Fig 1) shows that the major emerging market currencies have declined against the dollar in the past 12 months. However, some currencies have gained back some of their losses as the markets are increasingly optimistic about the economic re-opening.

Figure 1. Emerging currencies against the U.S dollar

Nonetheless, emerging currencies will continue to face economic challenges that will last for decades and which will have a continuous impact on the exchange rate. An outlook that underscores the need for currency hedging strategies in this uncertain market environment.

Why should all international firms be aware of the risk of these foreign exchange movements?

Exchange rate fluctuations affect numerous business transactions including:

- Export receivables

- Import payments

- Intercompany payments between offices and subsidiaries

- Foreign currency loans

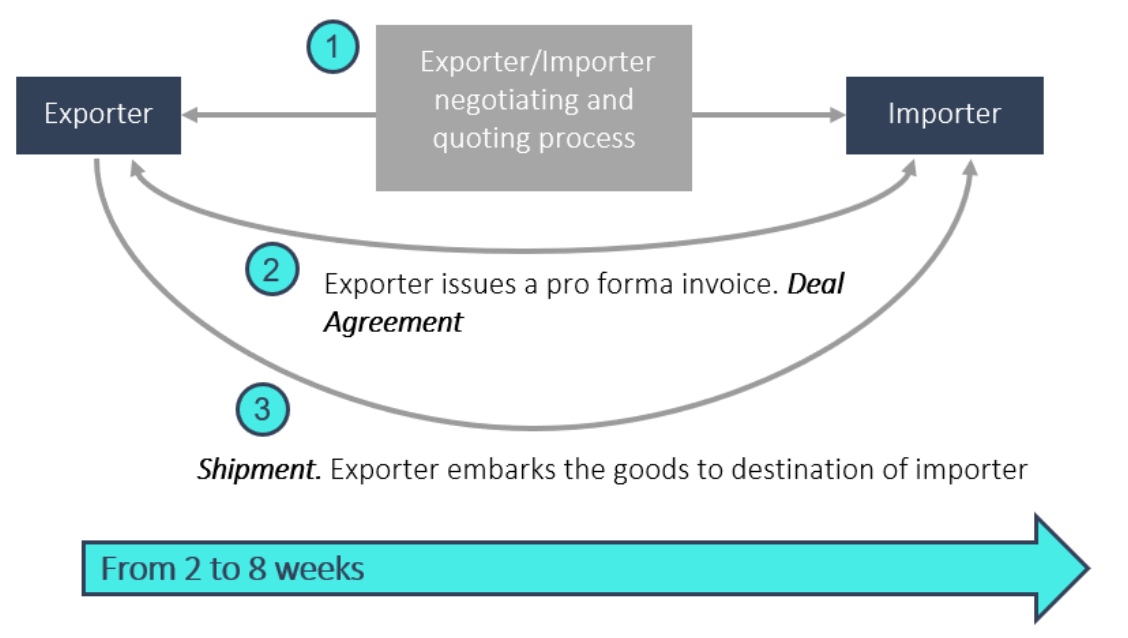

For educational purposes, the flowchart (Fig 2) below provides a high-level examination of the fruit, fishery and dairy exportation industries. This first step is a necessary simplification in a sector with different pricing mechanisms and numerous marketing channels.

Figure 2. Flowchart International Trade

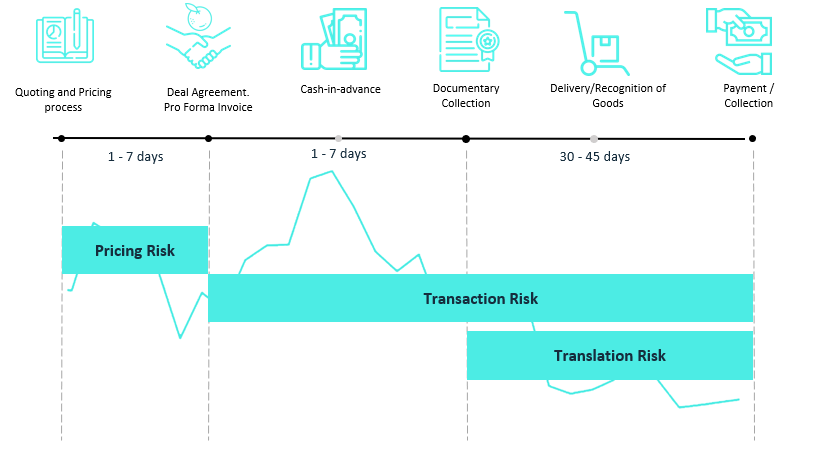

As a result, from this export flowchart, we now can outline the main risks related to currency volatility. The second step for implementing a solid FX risk management strategy when expanding your business globally is to understand the "Risk Map" in those sectors (Fig 3).

Figure 3. Risk Map

The export transaction generates three types of risks related to currency volatility:

i) Pricing Risk

ii) Transaction Risk

iii) Translation Risk

In this article, we will focus on transactional risk, this results from fluctuations in the exchange rate between the Deal Agreement and Payment/Collection. In the other words, if the exporter has invoiced in the buyer’s currency or any other currency different from its functional currency (generally the U.S dollar), they will be exposing their profit margins to currency fluctuations.

For an exporter, FX risk is very familiar to them. This is because of their need to convert the invoice into the buyer’s currency (or U.S Dollar) at the prevailing spot rate, on the day that the invoice is issued. His client (buyer) then settles the invoice in their local currency, typically anywhere between 15 to 60 days later, depending on the terms that they have demanded. Then, only after the funds have been received, can the exporter convert the payment into their local currency.

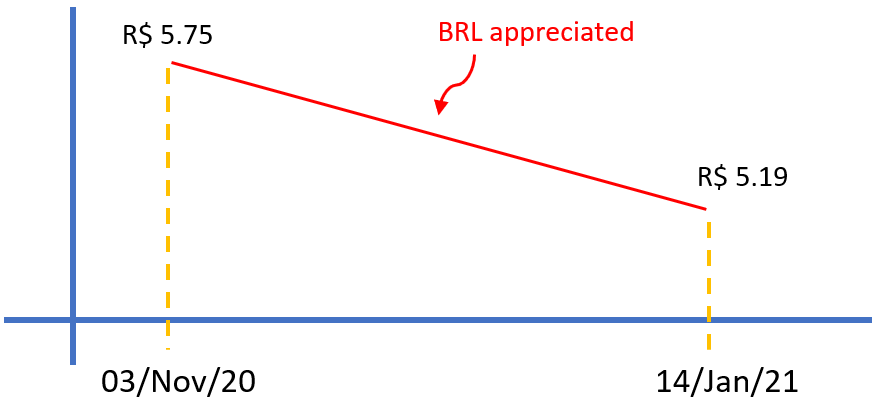

This leaves the fruit exporter exposed to changes in the local currency during the time lag or lead time between an invoice being issued and payment being received. Put simply, if the Brazilian exporter is required to invoice a customer in U.S Dollar and the BRL appreciates against the U.S dollar during this period, the exporter will receive less BRL than originally anticipated. See an example below:

1) Without FX hedging strategy

On 03/Nov/20 - Deal Agreement

- Value Invoice due on 14/Jan/21 = USD 350,000

- USDBRL spot rate on 03/Nov/20 = R$ 5.75

- Expected BRL Notional to receive = 350,000 x 5.75= BRL 2,012,500

On 14/Jan/21 - Converting Invoice

- The Brazilian exporter converts the receivables from USD to BRL using spot rate on 14/Jan/21 = R$ 5.19

- BRL Receivable = 350.000 x 5.19 = BRL 1,816,500

In this period from 03/Nov/20 to 14/Jan/21, the BRL appreciated against the U.S Dollar, the exporter received BRL 196,000 less than initially expected.

Therefore, it is important that these export firms understand the potential impact of FX risk on their bottom line and how to best manage it. Especially in such uncertain times.

Foreign exchange risk management strategies

With hedging strategies in place, not only can globally expanding businesses protect receivables or payments against market volatility, but also maximize their profit by taking advantage of the structure and fluctuation of the FX market.

There are four basic types of derivatives:

- Forward

- Futures

- Options

- Swaps.

A derivative contract is an agreement between two parties, which specifies that an amount of cash may be exchanged at a later date, set at a price fixed today. The value of the contract is derived from the current spot rate and a forward rate, which takes into consideration the interest rate differential between the two counterparty’s countries.

Here we will focus on Forward and Options contracts.

Type 1: Forward Contracts

A non-deliverable forward (NDF) is an agreement between two parties to buy or sell an agreed amount (of the non-convertible currency), on a specific due date, and at a defined forward rate. At its maturity, the forward rate is compared against the reference rate of that day. The difference between the pre-agreed forward rate and the fixing rate is settled in the convertible currency on your account at the due date. Therefore, you will either pay or receive the difference. As with a forward transaction, the costs of an NDF corresponds to the interest differential between the two currencies.

Type 2: Option Contracts

An option on a futures contract is the right, but not the obligation, to buy or sell a particular futures contract at a specific price, on or before a certain expiration date. There are two types of options: call options and put options.

--

If we go back to the example above, where the Brazilian exporter has a receivable of USD350,000 and we implement an FX hedging strategy using a forward contract and/or options contract, we will have the following results.

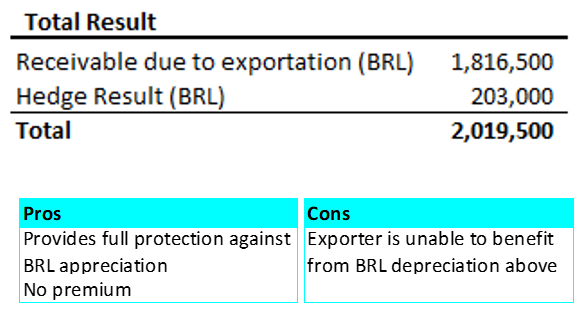

1. Forward

With a Forward Contract (NDF), the Brazilian exporter agrees to sell its USD at the Outright Forward Rate of 5.77, which provides full protection against the BRL appreciation of the spot rate, but will not be able to benefit should the BRL further depreciate.

On 03/Nov/20 - Deal Agreement

- Value Invoice due on 14/Jan/21 = USD 350,000

- USDBRL spot rate on 03/Nov/20 = R$ 5.75

- USDBRL forward rate on 14/Jan/21 = R$ 5.77

- Notional BRL hedged = 350,000 x 5.77 = BRL 2,019,500

On 14/Jan/21 - Converting Invoice and Hedge expiration

- The Brazilian exporter converts the receivables from USD to BRL using spot/PTAX rate on 14/Jan/21= R$ 5.19

- BRL Receivable = 350.000 x 5.19 = BRL 1,816,500

- The hedge strategy (NDF) expires against the spot/PTAX rate on 14/Jan/21 = 5.19

- FX Hedging strategy result = 5.77 – 5.19 = R$0.58

- 350.000 x 0.58= + BRL 203,000

The total result is:

If we compare both cases (with and without FX hedging strategy), we can see that the exporter not only protects the spot rate at R$ 5.75, but also maximizes their profit due to the forward curve that allows them to price the invoice using a forward USDBRL rate at R$ 5.77.

Thus, the exporter receives BRL 7,000 more than they would without an FX hedging strategy in place.

2. Options

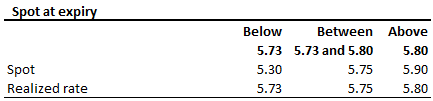

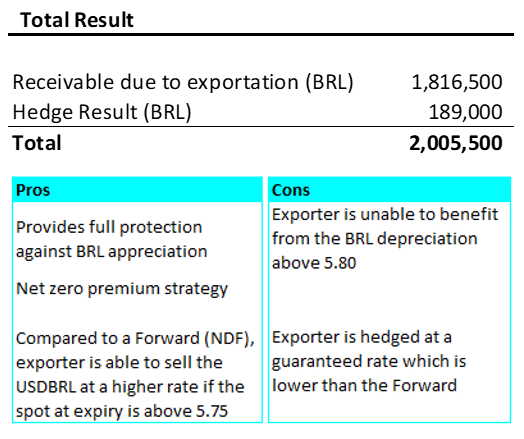

A Collar is a zero cost strategy and provides a minimum (floor rate) and a maximum (ceiling rate) realizable rate for the BRL against the USD. It provides full protection against the BRL appreciation and involves the purchase of a Put option and the sale of a Call option for the same amount. The premium raised by the sale of the Call matches the cost of the purchased Put Option.

The Exporter buys a Put option on the USDBRL at a strike of 5.73 and sells a Call option on the EUR at a strike of 5.80, thus being assured of a minimum and maximum selling price for the USDBRL.

How does it work?

On 14/Jan/21 - Converting Invoice and Hedge expiration

- The Brazilian exporter converts the receivables from USD to BRL using spot/PTAX rate on 14/Jan/21= R$ 5.19

- BRL Receivable = 350.000 x 5.19 = BRL 1,816,500

- The hedge strategy expires against the spot/PTAX rate on 14/Jan/21 = 5.19 and the Put Bought (floor rate) is exercised at 5.73.

- FX Hedging strategy result = 5.73 – 5.19 = R$0.54

- 350.000 x 0.54= + BRL 189,000

The total result is:

Hedging – The Advantages

Hedging offers definite advantages to global businesses and costs comparatively little. Hedging with the derivatives mentioned above allows an organization to lock in a foreign exchange rate that stabilizes a company’s operating costs or sales revenue whilst protecting its budget rate. Setting and protecting a budget rate can allow a business to enter new markets with confidence, expand its global operations and scale safely with more comfort and clarity.

It is important that the FX risk is managed, so the C-suite can focus their energies on core business operations, and not exchange rate fluctuations.

An FX specialist firm can help put together a risk management strategy that is bespoke to a client’s requirements. A great consultant will help you understand the strategy and give you all that you need to gain buy-in from your stakeholders and swiftly implement it.