A period of slowdown, but not recession

Economic overview

The U.S. economy began the second half of 2022 on a more solid basis than anticipated. The second-quarter economic output decline was less severe than expected, owing to higher consumer spending, private investment, and a tight labor market. Meanwhile, inflation showed signs of slowing, but not enough to breathe a sigh of relief, and the Fed maintained its hawkish stance to curb record-high price pressures.

According to revised figures published by the US Bureau of Economic Analysis, the nation's Gross Domestic Product (the broadest measure of economic activity) fell 0.6% from April to June. The advance estimate given in July, which indicated a 0.9% decline, was revised upward.

Source: Trading Economics

The updated GDP update includes a decline in inventory investment, housing investment, federal government spending, and state and local government spending. These were partially offset by robust exports and increased consumer spending, which accounts for the most economical production. Consumer spending grew 1.5% in the second quarter, up from a previous estimate of 1%. Also, inventory investment was less drag on growth.

Despite the revision, the current estimates reflect an economy that has contracted for two consecutive quarters. This threshold is often regarded as an unofficial indicator of a recession (the official arbiter is a panel of National Bureau of Economic Research economists who consider an array of economic indicators).

Many economists, however, do not believe the United States is in a recession. Instead, they point to a robust labor market and increased consumer and company spending, production, and revenue. The Labor Department reported Thursday that initial jobless claims, a barometer for layoffs, fell to a seasonally adjusted 243,000 from a revised 245,000 the prior week. After increasing from a 50-year low in March, the weekly total has remained close to 250,000 since early July. Also, the employers gained 528,000 jobs in July, completing the recoupment of the 22 million employees lost in the first months of 2020. The unemployment rate in the United States has fallen to 3.5%, matching a 50-year low.

Source: Trading Economics

Still, the new GDP data indicated that the property market faltered due to higher borrowing prices. According to the Commerce Department, residential investment declined at a 16.2% rate in the second quarter, worse than the earlier predicted 14% decline due to a decrease in real-estate brokers' commissions.

Furthermore, other recent economic data suggest a slowdown: An S&P Global purchasing managers index, which gauges manufacturing and service activity, was 45.0 in August, down from 47.7 in July, indicating a contraction. Both business and consumer expenditures are easing lately. Also, overall retail sales, which include spending in stores, online, and in restaurants, were flat in July.

Thus, the varied nature of the data makes it difficult to declare that we are in the midst of a recession. However, one thing is sure: economic growth has paused or slowed for a while, according to the most recent statistics.

All of this is based on the second estimate for quarterly GDP statistics. The third revision, due in September, will shed more light on economic growth with more comprehensive data.

In the meantime, inflation has been exceptionally high in recent months, eroding not only wage increases, purchasing power, and savings accounts but also Americans' optimism about the economy's path.

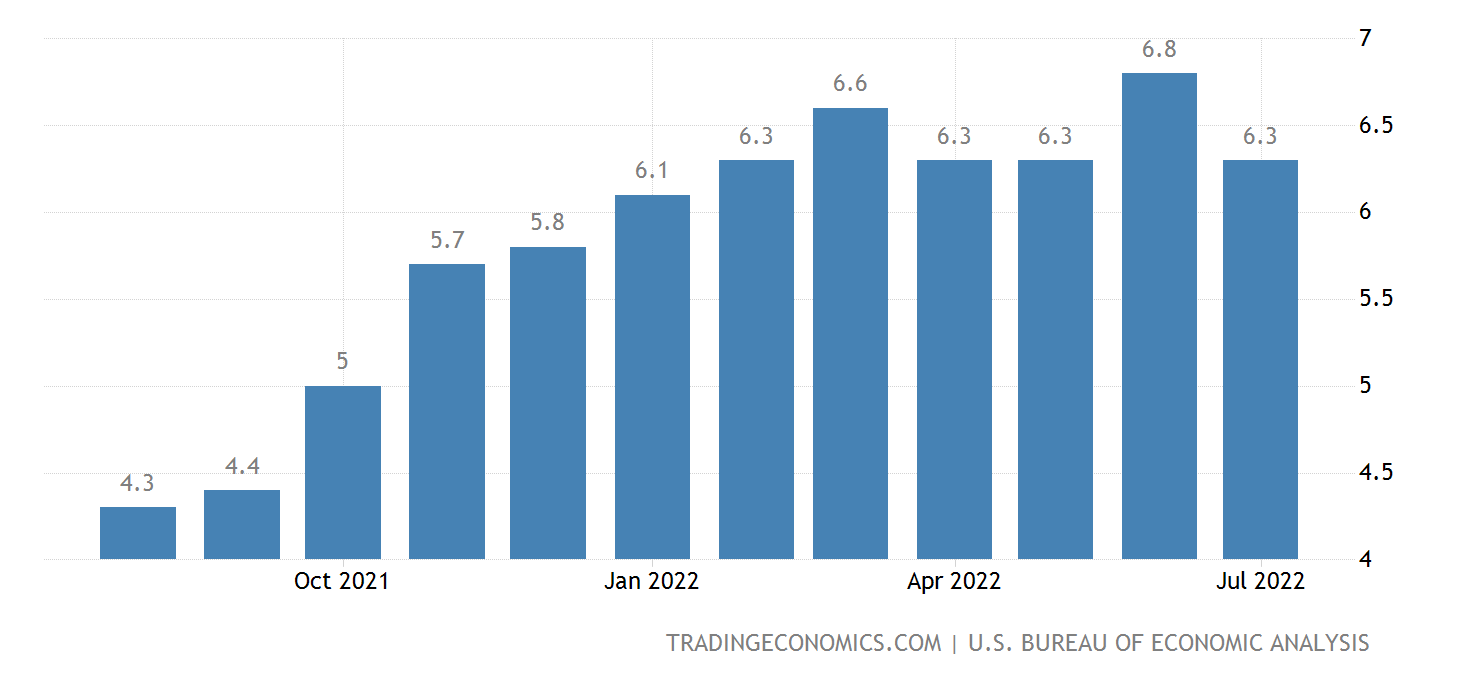

As part of its efforts to cool inflation and slow demand, the Federal Reserve has raised interest rates several times. According to the Fed's preferred measure, annual inflation fell to 6.3% in July from 6.8% in June, partly due to lower energy prices.

Source: Trading Economics

This leads many to believe that the inflation slowdown will be prolonged and that the Fed will be able to scale back its interest-rate hike campaign. However, during the Jackson Hole conference, Fed Chairman Jerome Powell warned that "a single month's improvement falls far short" of what he needs to determine that inflation is returning to the Fed's 2% target. He also stated that rate hikes would continue for some time, raising the likelihood of a 75 basis point hike at the next meeting.

His warning deflated the market's enthusiasm for now. Following his aggressive remarks, experts state that if inflation does not fall and the Fed responds with additional, substantial interest-rate rises, then the United States may be on the verge of an unmistakable downturn that everyone agrees on calling a recession. Thus what happens next will be heavily influenced by inflation's behavior during the next few months.

US dollar Index (DXY) and Stock markets

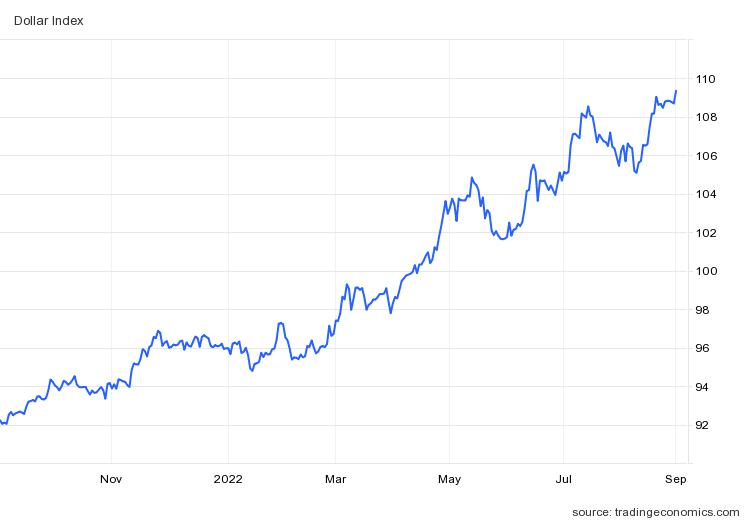

The dollar index is extending its July upswing and is currently on track for a third consecutive monthly gain, supported by robust expectations that the Federal Reserve will keep interest rates raised until inflation returns to the target range. The index has risen 2.4% this month and is anticipated to climb higher, supported by Fed officials’ hawkish tone. Recently, Fed's Mester stated on Wednesday that the central bank will need to boost the fed funds rate by 4% in early 2023 and maintain it there to combat skyrocketing inflation.

Meanwhile, supporting the hawkish Fed was recent data suggesting that job opportunities in the United States surged in July, and consumer confidence rebounded considerably in August. Moving forward, the Fed's decision to raise interest rates by 75 basis points will be focused on the inflation outlook rather than the monthly jobs data due on Friday. Nonetheless, the U.S. nonfarm payrolls report is projected to indicate that the economy added 300,000 jobs in August and might strengthen the case for rate hikes for the Fed.

US Dollar Index historical rates. Source: Trading economics

What started out as a solid month for the three major averages is set to end on a down one. The Dow and S&P 500 finished approximately 3% lower in August. The Nasdaq is expected to close down nearly 4%. Investors have been discussing whether the economy is in a recession or moving toward one for weeks, and many believed that a downturn would give the Fed cause to ease off on its rate hike schedule. Since Powell’s hawkish remarks on the Jackson hole symposium, stocks have been falling precipitously. In addition, Cleveland Fed President Loretta Mester stated recently that benchmark interest rates would rise over 4% by early next year. Volatility has escalated since the Fed's last signal, taking many investors' breath away, but a few indicators provide hope, such as the rise in Treasury yields. Moving forward, economic data releases and the Fed's tone about rate hikes to combat inflation will drive U.S. equities.

S&P 500 and Nasdaq Composite historical prices. Source: Trading Economics

September's Economic Calendar

Thursday 09/01/2022 – Initial Jobless Claims (Aug) | Nonfarm Productivity Q2 | ISM Manufacturing PMI(Aug) | S&P Global Manufacturing PMI (Aug)

Friday 09/02/2022 – Labor Force Participation Rate (Aug) | Nonfarm Payrolls (Aug) | Unemployment rate (Aug)

Tuesday 09/06/2022 – ISM Services PMI (Aug) | S&P Global Service and Composite PMI (Aug)

Wednesday 09/07/2022 – Goods and Service Trade Balance (Jul)

Tuesday 09/13/2022 – Consumer Price Index (Aug)

Wednesday 09/14/2022 – Producer Price Index (Aug)

Thursday 09/15/2022 – Retail Sales (Aug) | Philadelphia Fed Manufacturing Survey (Sep)

Friday 09/16/2022 – Michigan Consumer Sentiment Index (Sep) PREL

Tuesday 09/20/2022 – Building Permits and Housing Starts (Aug)

Wednesday 09/21/2022 - Fed’s Interest Rate Decision

Friday 09/23/2022 – S&P Global Composite, Service and Composite PMI (Sep) (PREL)

Monday 09/26/2022 – Chicago Fed National Activity Index (Aug)

Tuesday 09/27/2022 - Durable Goods Orders (Aug) | Housing Price Index (Jul) | S&P/Case Shiller Home Price Index (Jul) | Consumer Confidence (Sep) | New Home Sales (Aug)

Wednesday 09/28/2022 - GDP Q2

Thursday 09/29/2022 – PCE Q2

Friday 09/30/2022 – Personal Income (Aug) | Personal Spending (Aug) | Chicago PMI (Sep) | Michigan Consumer Sentiment Index (Sep)

If you have any questions, feel free to contact us and speak to an expert today.