With global economic uncertainties on the rise, currency volatility is expected to surge in 2024. Treasurers and risk managers face the critical task of safeguarding shrinking margins efficiently. While forwards and swaps have traditionally dominated hedging strategies, diverging central bank mandates are leading to increased forward points, reducing their appeal. In this landscape, options emerge as a compelling alternative, often the sole option available. However, their perceived complexity and costs have hindered widespread adoption. This post aims to demystify the realm of hedging with options, offering insights into navigating currency volatility.

FX Risk Management: Strategies for Corporations and Investment Funds

Businesses spanning various sectors, including corporations, investment funds, and import/export firms, operate across borders, exposing them to foreign exchange (FX) risk. The collapse of Bretton Woods in the early 1970s ushered in an era of floating exchange rates, introducing FX risk.

Corporations, managing regular monthly local currency flows and holding local currency assets, dedicate substantial resources to forecasting and hedging these flows against their reporting currency. Metrics such as EPS attributable to FX and probabilistic earnings at risk gauge their hedging success, guided by accounting standards like FASB and IAS.

Conversely, investment funds undergo deployment and harvest cycles spanning several years, posing unique challenges in hedging large, uncertain flows with maturities surpassing available derivative tenors. Their success metrics focus on hedge cost and the internal rate of return (IRR) of hedged flows. Navigating these complexities requires tailored strategies and adherence to regulatory frameworks, highlighting the importance of effective FX risk management practices.

Investment funds face extended deployment and harvest cycles, presenting a unique challenge in hedging large, long-term flows exceeding derivative tenors. Success metrics include hedge cost and hedged flow internal rate of return (IRR).

Another instance is cross-border loans or bonds, where emerging market countries' high deposit rates, set by central banks to curb inflation, elevate local borrowing costs. This prompts firms to seek loans from OECD countries like the US or UK. Repayment risk, particularly for loans with balloon terms, escalates due to potential adverse exchange rate fluctuations in the future.

Mastering Currency Options: Strategies, Costs, and Risk Management Explained

Similar to equity options, currency options provide the right, yet not the obligation, to buy (call) or sell (put) foreign currency at a predetermined exchange rate (the strike) at a specific future date. For instance, a EURUSD call (specifically a EUR Call/USD put) shields against the USD depreciation versus the EUR, potentially utilized by an EU-based firm to hedge USD profits. However, options aren't cost-free; hedgers must pay a premium. Moreover, premiums are influenced by volatility, becoming pricier when most needed, prompting the use of various option strategies combining buying and selling to optimize protection while minimizing costs.

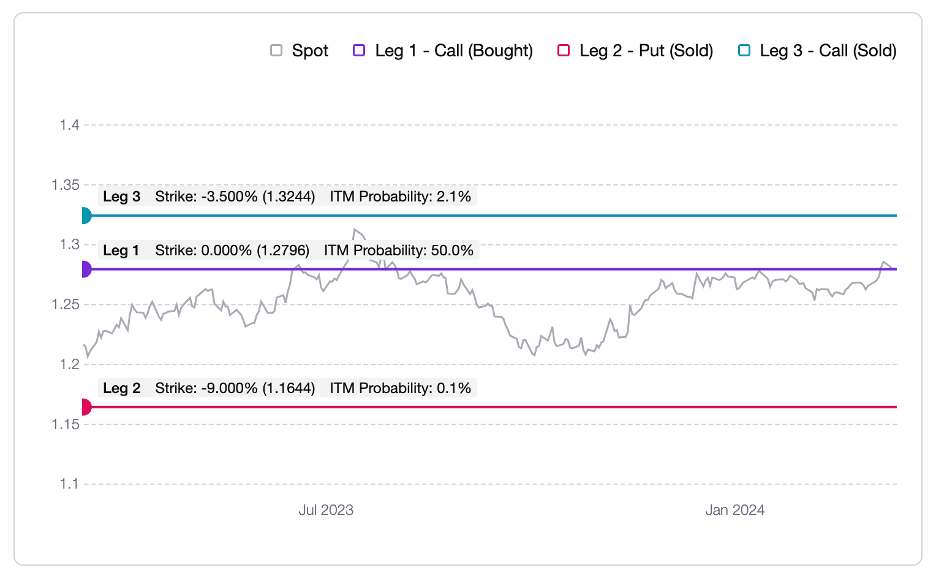

The "strike" of an option denotes the spot rate at which it takes effect. For a call option, if the strike surpasses the current spot rate, it's deemed out of the money (OTM); conversely, if the strike is below the current spot, it's in the money (ITM). This relationship is reversed for put options.

Lastly, the issuing bank may impose an initial or variation margin to mitigate the risk of hedgers defaulting on derivative losses, with terms contingent on the hedger's creditworthiness.

Exploring Advanced Currency Hedging Strategies: Maximizing Protection, Minimizing Costs

Currency hedging strategies encompass a myriad of approaches, ranging from simple to complex, involving combinations of bought and sold calls and puts. These strategies, often involving 2 to 4 "legs," aim to optimize protection while minimizing net premiums paid. Some common strategies include collars, which bound both downside and upside; participating forwards, offering a synthetic forward with reduced cost and upside; and "seagulls," a three-legged approach with a protective leg and two sold, out-of-the-money legs to offset costs (but with notable tail risk).

Choosing the right strategy demands a thorough understanding of option interactions. Hedgers must consider various constraints, such as total hedge cost as a percentage of underlying exposure and the risk of sold option legs becoming in the money, thus imposing obligations on the hedger. Additionally, each hedge strategy carries the risk of a margin call, particularly concerning for entities like closed-end funds.

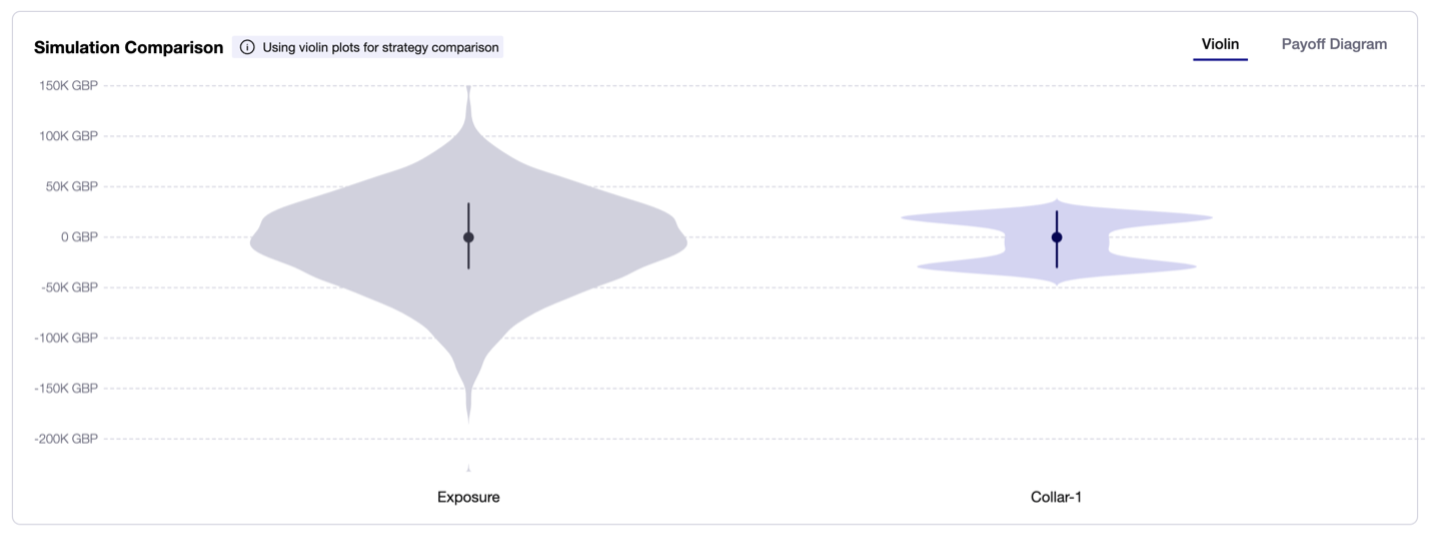

Utilizing simulation and visualization tools is vital for comprehending hedge effects. For instance. Navigating these complexities requires a nuanced approach and careful consideration of risk factors to ensure effective currency risk management.

Selecting legs, strikes, and leverage quickly complicates currency risk management.

Conclusion

Hedging with options presents an attractive alternative to forwards, particularly when facing negative carry. However, navigating the complexity and optimizing strategies can be challenging. While you may find a viable strategy, determining if it's the best option requires careful consideration and often involves trial and error, which can be time-consuming and inefficient.

Enter hedge optimization - the holy grail of hedging. This approach promises to democratize access to optimal hedges, leveling the playing field for all.