In November, the US economy was heading through supply chain bottlenecks, the Omicron virus development, and robust inflation. Presently, the nation is gripped by surging Covid-19 daily infections, the Fed’s monetary policy tightening phase to combat inflation, improved unemployment situations, and geopolitical tensions such as the approval of the Build Back Better (BBB) plan, as well as tensions over Ukraine. The U.S. Gross Domestic Product, which measures the total output of the economy, grew by 2.3% in December for a quarter-on-quarter annualized basis, surpassing expectations of 2.1% and a previous print of 2.1%. The new strength can be credited to better consumer spending as well as improved unemployment conditions. However, prospects for a strong rebound are being clouded by the rapidly growing Omicron strain in the nation. Furthermore, with consumer prices pinching albeit a healing economy, policymakers are reducing bond purchases and preparing to hike interest rates in the next year.

Although Consumer confidence and labour market conditions have improved, Covid has upgraded itself with a new variant. The final reading of the University of Michigan's consumer confidence index was 70.6 in December, slightly higher than the preliminary estimate of 70.4 and up from 67.4 in November. The index increased as a result of large increments in income for families in the lowest third of the wealth distribution. Additionally, it is important to consider the turnaround in labour market conditions. The unemployment rate decreased to 4.2%, down from 4.6% previously in November, whereas the Labour Force Participation Rate improved marginally. With respect to that, figures stood at 61.8%, up from 61.6% in November. On the flip side, numerous flights have been canceled and plans to return to the workplace have been abandoned. College football games and Broadway productions have been canceled, and Apple outlets in New York City have shut down. With 301,472 cases in a single day on 30th December, the U.S. set a new global record for daily average cases, with Omicron accounting for 59% of all new infections. Lately, Americans are putting pressure on the Biden administration as they spend hours waiting to be tested for Covid-19, and experts worry that the virus will 'threaten essential infrastructure' in the United States, forcing personnel at hospitals, grocery shops, and petrol stations into isolation.

University of Michigan Consumer Confidence Index

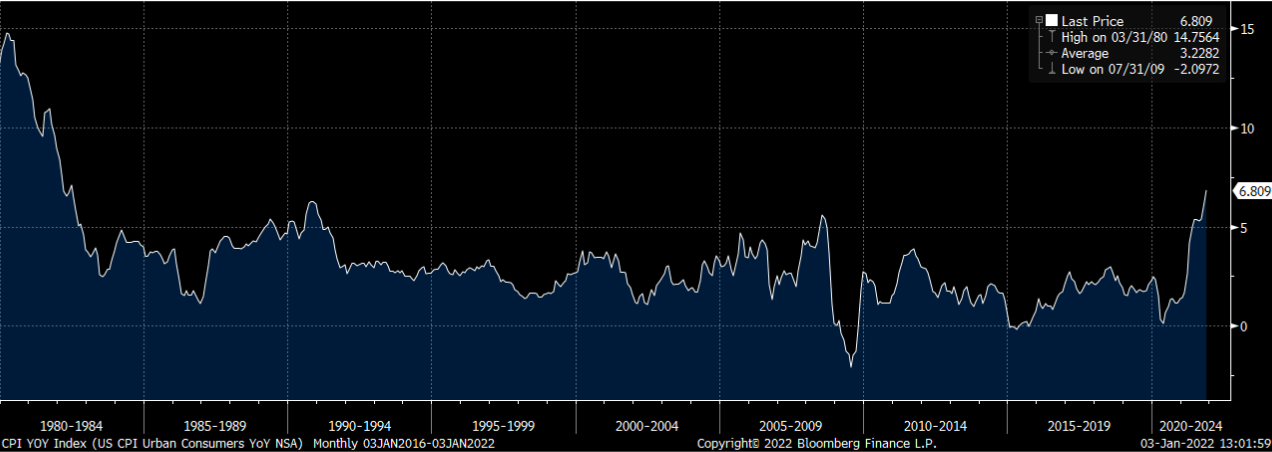

Consumer prices have skyrocketed to the highest levels in nearly four decades while the Fed starts to chase inflation after a long time. The Consumer Price Index, a key indicator to measure inflation and change in purchasing power at a broader level, stands at 6.8% on an annual basis in November, the highest in the last 39 years. According to the Census, prices increased substantially, with fuel, housing, food, used cars and trucks, as well as new vehicles all contributing significantly. In November, the energy index increased by 3.5%, while the gasoline index increased by 6.1%, as motorists paid extra to fill up their tanks. Food got more costly as well - the food index grew by 0.7% throughout the month, with 'food at home' increasing by 0.8%. In these record-high inflation times, the U.S. central bank Federal Reserve has pulled off the band-aid to start focusing on persistently high inflation. The Federal Reserve will accelerate the winding down of its stimulus program, as it ramps up its reaction to rising inflation. Additionally, the updated predictions indicate that policymakers believe three hikes are necessary for 2023 and two more in 2024. Officials increased their inflation projection for 2022 to 2.6%, from 2.2% in September, while also forecasting a decline in the unemployment rate to 3.5%.

Consumer Price Index

The ‘Build Back Better’ (BBB) plan is on hold while it has already baked many economic projections for the next year. President Joe Biden's inability to get the required votes to approve his $1.8 trillion Build Back Better proposal implies that the economic boost that was built into many 2022 estimates will be lost. For example, the expiry of the child care tax credit, which was extended in the blocked plan, would coincide with the winding down of several other stimulus programs and the beginning of the Federal Reserve's "tapering" of monetary stimulus. News that West Virginia Democratic Sen. Joe Manchin voted against the plan prompted Goldman Sachs analysts to lower their first-quarter growth projection from 3% to 2%, while also lowering their full-year estimates.

Looking ahead, it is not just the Omicron that will stymie the economy next year, as Biden's administration Build Back Better (BBB) also plays an important part in the economy. According to Kathy Bostjancic, Oxford's chief U.S. financial economist, the resurgence of COVID-19 could reduce growth next year from 4.3% to 4.1%, and if Biden's Build Back Better program is completely derailed, it could shave another 0.4 percentage point from growth in 2022, lowering it to around 3.7%, and a half-point from growth in 2023, lowering it to below 2%.

U.S. Dollar index

The U.S. Dollar Index, which gauges the greenback against the basket of currencies, is on the verge of closing the month with a marginal loss. The dollar index depreciated by 0.18% during December after touching a 16-month high level in the previous month. Although, it is ending the year with a 7% gain, the highest since March 2015, amid prospects that Fed is paving way for interest rate hikes in the next year. The index reacted positively to improved unemployment statistics, strong ISM service PMI for November, improved Michigan Consumer Sentiment index for December, and higher than expected GDP growth results for Q3. The consistently higher inflation measured through Consumer Price Index (CPI) and Core Personal Consumption Expenditure (PCE) prompted the Fed to increase the rate hike expectations and in turn, boosted the dollar. However, lower than expected Non-farm payroll figures and improved risk sentiment due to easing concerns over the new Omicron variant undermined the dollar. Lastly, the halt of Biden’s Build Back Better (BBB) $1.75 trillion bill, due to the fallout of Democrat Joe Manchin, held back the dollar from potential gains. Looking forward, the development of Omicron, and movement around the BBB bill will drive the dollar dynamics in the near term.

The S&P index ended the month with strong gains again after rallying in November. The index started with $4582.00 on December 1st, and currently trades at $4767.75 as of writing, gaining almost 4.5% for the month. Additionally, it is on course to close the year with 27% gains annually, the highest among its peer index including Nasdaq and Dow Jones, which have gained 24% and 19% respectively. The key market mover was the Fed's interest rate decision, which surged the S&P index by 1.53% for the day. Although the market was highly reactive during the initial start of the month as Omicron infections were rapidly increasing, the S&P index gained its momentum back as the news rolled out that the new variant is less severe than the previous version and leads to fewer hospitalization cases. Following that, improved labor market conditions and increased risk appetite contributed to the surge. In contrast, the S&P index, while approaching the end of the month, has remained steady and posted losses amid thin liquidity conditions and the festive mood. Wrapping up, the index is closing with double-digit gains for the second consecutive year and has posted 70 record gains over the year. Moving on, the index is expected to be influenced further by the Fed’s rate hike movements, Omicron headlines, and the BBB bill news in the near term.

S&P 500, Dow Jones and Nasdaq Composite - Historical Price

To summarise, the United States' economy is on course for a robust end to 2021, and a decent start to 2022, as consumers and companies continue to spend despite rising inflation, staffing issues, continuing Covid-19 infections, and lingering supply restrictions. Economists predict that the economy will increase by an annualized 6% in the fourth quarter before slowing to a still-solid 3% in the first quarter and 3.5% in the second quarter of 2022. In the short term, inflation is anticipated to reach 7%, while the dread of Omicron is spreading swiftly. The next significant item in 2022 would be the development of the Omicron variant as well as action around the ‘Build Back Better’ Plan. Finally, in the midst of the virus and social spending stimulus, it will be interesting to see how the Fed fulfills its vow to combat inflation by lowering its pandemic assistance program and delivering three rate hikes in the next year.

December’s Economic Calendar

USD

Monday 01/03/2022 - Markit Manufacturing PMI (Dec)

Tuesday 01/04/2022 - ISM Manufacturing PMI (Dec)

Wednesday 01/05/2022 - Markit Services PMI (Dec) ¦ FOMC Minutes

Thursday 01/06/2022 - Goods and Services Trade Balance (Nov) ¦ Factory Orders (MoM) (Nov) ¦ ISM Services PMI (Dec)

Friday 01/07/2022 - Labor Force Participation Rate (Dec) ¦ Nonfarm Payrolls (Dec) ¦ Unemployment Rate (Dec)

Wednesday 01/12/2022 - Consumer Price Index (YoY) (Dec)

Thursday 01/13/2022 - Producer Price Index ex. Food & Energy (YoY) (Dec)

Friday 01/14/2022 - Retail Sales (MoM) (Dec) ¦ Michigan Consumer Sentiment Index (Jan)

Wednesday 01/19/2022 - Housing Starts (MoM) (Dec)

Thursday 01/20/2022 - Philadelphia Fed Manufacturing Survey (Jan)

Monday 01/24/2022 - Chicago Fed National Activity Index (Dec) ¦ Markit Services PMI (Jan)

Tuesday 01/25/2022 - Housing Price Index (MoM) (Nov) ¦ Consumer Confidence (Jan)

Wednesday 01/26/2022 - Durable Goods Orders (Dec) ¦ New Home Sales (MoM) (Dec) ¦ Fed Interest Rate Decision

Thursday 01/27/2022 - Core Personal Consumption Expenditures (QoQ) (Q4) ¦ Gross Domestic Product Annualized (Q4)

Friday 01/28/2022 - Core Personal Consumption Expenditures - Price Index (MoM) (Dec) ¦ Personal Spending (Dec) ¦ Personal Income (Dec) ¦ Michigan Consumer Sentiment Index (Jan)

Monday 01/31/2022 - Chicago Purchasing Managers' Index (Jan)

EUR

Wednesday 01/05/2022 - Markit PMI Composite (Dec)

Friday 01/07/2022 - Consumer Confidence (Dec) ¦ Consumer Price Index (YoY) (Dec) ¦ Industrial Confidence (Dec) ¦ Retail Sales (YoY) (Nov)

Thursday 01/13/2022 - Economic Bulletin

Thursday 01/20/2022 - Consumer Price Index (MoM) (Dec) ¦ ECB Monetary Policy Meeting Accounts

Monday 01/24/2022 - Markit Manufacturing PMI (Jan) ¦ Markit PMI Composite (Jan) ¦ Markit Services PMI (Jan)

Friday 01/28/2022 - Gross Domestic Product s.a. (QoQ) (Q4)

GBP

Tuesday 01/04/2022 - Markit Manufacturing PMI (Dec)

Wednesday 01/12/2022 - Gross Domestic Product (MoM) (Nov) ¦ Gross Domestic Product (MoM) (Nov) ¦ Manufacturing Production (MoM) (Nov)

Tuesday 01/18/2022 - Claimant Count Change (Dec) ¦ ILO Unemployment Rate (3M) (Nov)

Wednesday 01/19/2022 - Consumer Price Index (MoM) (Dec) ¦ PPI Core Output (MoM) (Dec) ¦ Retail Price Index (MoM) (Dec)

Friday 01/21/2022 - GfK Consumer Confidence (Jan) ¦ Retail Sales (MoM) (Dec) ¦ Markit Services PMI (Jan)

Monday 01/24/2022 - Markit Manufacturing PMI (Jan)

JPY

Thursday 01/06/2022 - Overall Household Spending (YoY) (Nov) ¦ Tokyo Consumer Price Index (YoY) (Dec)

Tuesday 01/11/2022 - Current Account n.s.a. (Nov)

Tuesday 01/18/2022 - BoJ Interest Rate Decision ¦ Industrial Production (YoY) (Nov)

Wednesday 01/19/2022 - BoJ Outlook Report (Q4) ¦ Merchandise Trade Balance Total (Dec)

Thursday 01/20/2022 - National Consumer Price Index (YoY) (Dec) ¦ BoJ Monetary Policy Meeting Minutes

Thursday 01/27/2022 - Tokyo Consumer Price Index (YoY) (Jan) ¦ Retail Trade (YoY) (Dec)

Sunday 01/30/2022 - Industrial Production (MoM) (Dec)

Monday 01/31/2022 - Unemployment Rate (Dec)

CAD

Tuesday 01/04/2022 - Markit Manufacturing PMI (Dec)

Thursday 01/06/2022 - International Merchandise Trade (Nov)

Tuesday 01/11/2022 - Unemployment Rate (Dec) ¦ Ivey Purchasing Managers Index (Dec)

Monday 01/17/2022 - Bank of Canada Business Outlook Survey

Tuesday 01/18/2022 - BoC Consumer Price Index Core (MoM) (Dec) ¦ Consumer Price Index (MoM) (Dec)

Friday 01/21/2022 - Retail Sales (MoM) (Nov)

Wednesday 01/26/2022 - BoC Interest Rate Decision ¦ Bank of Canada Monetary Policy Report

CNY

Tuesday 01/04/2022 - Caixin Manufacturing PMI (Dec)

Thursday 01/06/2022 - Caixin Services PMI (Dec)

Friday 01/07/2022 - Foreign Exchange Reserves (MoM) (Dec)

Monday 01/10/2022 - Consumer Price Index (YoY) (Dec) ¦ M2 Money Supply (YoY) (Dec)

Thursday 01/13/2022 - Trade Balance USD (Dec)

Monday 01/17/2022 - Industrial Production (YoY) (Dec) ¦ Retail Sales (YoY) (Dec)

Tuesday 01/18/2022 - Gross Domestic Product (QoQ) (Q4)

Wednesday 01/19/2022 - FDI - Foreign Direct Investment (YTD) (YoY) (Dec)

Thursday 01/20/2022 - PBoC Interest Rate Decision

Sunday 01/30/2022 - Caixin Manufacturing PMI (Jan)

Monday 01/31/2022 - NBS Manufacturing PMI (Jan) ¦ Non-Manufacturing PMI (Jan)

BRL

Monday 01/03/2022 - HSBC PMI Manufacturing (Dec) ¦ Trade Balance (Dec)

Thursday 01/06/2022 - Industrial Output (MoM) (Nov)

Sunday 01/09/2022 - IPCA Inflation (Dec)

Friday 01/14/2022 - Retail Sales (MoM) (Nov)

Friday 01/21/2022 - Mid-month Inflation (Jan)

Wednesday 01/26/2022 - Current Account (Dec)

Friday 01/28/2022 - Inflation Index/IGP-M (Jan) ¦ Unemployment Rate (Nov)

Monday 01/31/2022 - Nominal Budget Balance (Dec) ¦ Primary Budget Surplus (Dec)

MXN

Wednesday 01/05/2022 - Consumer Confidence (Dec)

Friday 01/07/2022 - 12-Month Inflation (Dec) ¦ Core Inflation (Dec) ¦ Headline Inflation (Dec)

Thursday 01/20/2022 - Jobless Rate (Dec)

Monday 01/24/2022 - 1st half-month Inflation (Jan) ¦ Trade Balance (Dec)

Monday 01/31/2022 - Fiscal Balance, Pesos (Dec)

If you have any questions, feel free to contact us and speak to an expert today.