Glossary

Every key term in foreign exchange risk management, hedging instruments, treasury strategy, and hedge accounting — written for CFOs, fund managers, treasurers, and finance professionals working with cross-border exposures.

A

ASC 815 (Derivatives and Hedging)

The US GAAP standard governing the accounting treatment of all derivative instruments and hedging relationships. It requires entities to recognise all derivatives on the balance sheet at fair value and sets out the criteria for applying hedge accounting to reduce earnings volatility.

▼

ASC 815 (formerly SFAS 133) governs how US GAAP reporting entities account for derivative instruments. It requires all derivatives to be recognised on the balance sheet at fair value. Without hedge accounting designation, changes in fair value flow directly through the income statement, creating earnings volatility unrelated to underlying business performance.

Hedge accounting under ASC 815 allows entities to offset that volatility by matching gains and losses on the hedging instrument against the hedged exposure. Three hedge types are recognised: fair value hedges, cash flow hedges, and hedges of net investments in foreign operations.

To qualify, the entity must formally document the hedging relationship at inception, demonstrate that the hedge is highly effective (within an 80–125% effectiveness range historically; now a more qualitative test under the 2017 ASU improvements), and assess effectiveness on an ongoing basis.

Example

A US multinational with EUR-denominated receivables designates a USD/EUR forward as a cash flow hedge under ASC 815. Changes in the forward's fair value are recorded in OCI and reclassified to earnings when the receivable is settled, avoiding P&L distortion during the hedge period.S

Deaglo Relevance

Deaglo's platform supports full ASC 815 compliance — generating audit-ready documentation, effectiveness testing output, and hedge performance reports structured for US GAAP reporting.

B

Basis Risk

The risk that a hedge does not perfectly offset the underlying exposure because the two positions do not move in exact correlation. Basis risk arises when the instrument used to hedge differs from the exact exposure being hedged.

▼

Basis risk occurs when the value of a hedging instrument and the value of the exposure it is meant to protect do not move in perfect lockstep. Common sources of basis risk include currency mismatches (hedging with a proxy currency when the exact pair is illiquid), timing differences between the hedge maturity and the cash flow date, and differences in valuation methodology between the hedge and the hedged item.

In FX risk management, a frequent example is using a USD/MXN NDF to hedge a Mexican peso receivable when the actual exposure is denominated in a regional Mexican currency that trades at a spread to the NDF market rate. Even if the overall direction of the hedge is correct, the imperfect correlation produces residual P&L exposure.

Basis risk must be documented and assessed as part of hedge accounting requirements under both IFRS 9 and ASC 815.

Basis Points (bps)

A unit of measurement equal to one hundredth of one percentage point (0.01%). Widely used in FX and interest rate markets to express spreads, rate changes, and pricing differences with precision.

▼

One basis point equals 0.01%, so 100 basis points equal 1%. The term is used across finance because percentage-based language can be ambiguous: saying a spread "increased by 0.5%" could mean 0.5 percentage points or 50% of the original spread. Basis points remove this ambiguity.

In FX, basis points are used to quote forward points (the premium or discount applied to the spot rate to arrive at the forward rate), bid-offer spreads, and execution cost benchmarks. A spread of 5 bps on a $10 million transaction represents a $5,000 cost.

Example

A bank quotes a USD/BRL forward with a bid-offer spread of 25 bps. On a USD 5 million transaction, this spread cost equals approximately USD 12,500 — a figure the Deaglo FX Diagnostic benchmarks against best execution.

Bid-Offer Spread

The difference between the rate at which a market maker will buy a currency (the bid) and the rate at which it will sell (the offer). The bid-offer spread represents the implicit transaction cost paid by the buyer of FX services.

▼

The bid-offer spread (also called bid-ask spread) is the primary source of revenue for FX market makers. A corporate or fund that buys USD will receive the lower bid rate; a party selling USD receives the higher offer. The spread between the two reflects liquidity, volatility, and counterparty risk — as well as the market power of the selling institution.

In EM currencies, spreads are typically wider than in major currency pairs due to lower liquidity, capital controls, and settlement risk. Benchmarking the spread obtained against the mid-market rate is one of the core outputs of the Deaglo FX Diagnostic — specifically in the execution cost analysis.

For companies executing large or recurring FX transactions, even a few basis points of spread improvement per transaction can produce material cumulative savings.

Budget Rate

The exchange rate that a company uses when constructing its financial budgets and forecasts. Budget rates establish the FX assumption embedded in revenue, cost, and profit projections — and the benchmark against which actual FX performance is measured.

▼

The budget rate is the exchange rate assumption used in annual financial planning. If actual exchange rates differ materially from the budget rate by the time transactions occur, revenues, costs, and margins will deviate from plan — even if the underlying business is performing as expected.

The primary purpose of FX hedging in many corporates is to protect the budget rate — ensuring that the FX rate used in planning is as close as possible to the rate at which transactions are actually settled. This is why forward contracts are commonly used: they lock in a rate at or close to the budget rate for a defined period.

The FX Diagnostic compares the budget rate against actual rates obtained and the current hedge position to show how much of the budget assumption is actually protected.

Example

A Mexican importer builds its annual budget assuming USD/MXN at 17.50. If the spot rate rises to 18.20 during the year, unhedged USD purchases will cost 4% more than budgeted — directly compressing operating margins unless the exposure was hedged at or near the budget rate.

C

Carry / Cost of Carry

The net cost or benefit of holding a hedged FX position, derived from the interest rate differential between the two currencies. When hedging a high-yield EM currency against USD, the cost of carry reflects the premium paid to lock in the forward rate.

▼

The cost of carry in FX arises from interest rate parity: the forward exchange rate reflects the interest rate differential between two currencies. If Brazil has higher interest rates than the US, a USD/BRL forward will price in a premium — meaning the forward BRL rate will be weaker than the spot rate. A fund or corporate buying BRL protection via a forward or NDF effectively pays the interest rate differential as an implicit cost.

For companies hedging EM currency exposures, carry cost is a critical component of the total cost of hedging and must be weighed against the risk being protected. A high carry environment makes structured solutions (collars, participating forwards) more attractive than simple forwards because they reduce upfront cost while preserving some directional benefit.

The FX Diagnostic benchmarks carry cost as part of the hedge cost efficiency review — showing whether the current structure is cost-effective given the level of protection provided.

Cash Flow Hedge

A hedge accounting designation that protects against variability in future cash flows attributable to a specific risk. Gains and losses on the hedging instrument are deferred in Other Comprehensive Income (OCI) until the hedged transaction occurs and affects the income statement.

▼

A cash flow hedge is the most common hedge accounting designation for corporate FX risk management. It applies when a company is protecting against the variability in expected future cash flows caused by changes in exchange rates — for example, forecasted export revenues, future foreign currency purchases, or interest payments on variable-rate foreign currency debt.

The effective portion of the hedge's gain or loss is recorded in Other Comprehensive Income (OCI) — a component of shareholders' equity that bypasses the income statement. When the hedged item eventually affects earnings (e.g., when the revenue is recognised), the amounts deferred in OCI are simultaneously reclassified into the income statement, matching the hedge gain or loss against the hedged exposure.

The result: the income statement reflects the hedged rate rather than the prevailing market rate, significantly reducing reported earnings volatility.

Example

A Brazilian PE fund with USD share classes designates NDFs as cash flow hedges of its USD dividend distributions. Gains and losses on the NDFs are held in OCI and reclassified into earnings when the distributions are made — keeping the fund's reported income stable regardless of interim USD/BRL moves.

Key requirements under IFRS 9 and ASC 815: formal designation and documentation at inception, an economic relationship between the instrument and the hedged item, and ongoing effectiveness assessment.

Deaglo Relevance

Deaglo generates hedge accounting documentation and effectiveness testing outputs that support cash flow hedge designation under both IFRS 9 and ASC 815 — reducing the audit and compliance burden on treasury and finance teams.

Cash Flow at Risk (CFaR)

A risk metric that quantifies the maximum adverse impact of exchange rate or interest rate movements on a company's future cash flows over a defined period at a given confidence level. CFaR is expressed in cash flow terms, making it directly relevant to debt service planning and covenant compliance.

▼

Unlike Value at Risk (VaR), which focuses on the market value of a position, Cash Flow at Risk (CFaR) measures the potential shortfall in operating or financing cash flows due to market rate movements. It is particularly relevant for corporates and infrastructure companies where the primary concern is whether cash flows are sufficient to service debt, meet covenants, and fund operations — rather than the mark-to-market value of a financial instrument.

CFaR is expressed as: "at a X% confidence level, the adverse impact on cash flows over the next 12 months will not exceed Y." This framing is directly useful for CFOs and treasurers presenting FX risk to boards, lenders, or rating agencies.

Deaglo uses CFaR as part of its systematic risk quantification framework alongside DV01, duration, and CVaR — providing a comprehensive view of how market moves affect both earnings and cash flows.

Collar (FX)

An FX hedging strategy that bounds exchange rate exposure within a defined range by combining the purchase of one option (a cap or floor) with the simultaneous sale of another. The premium from the sold option offsets some or all of the cost of the purchased option.

▼

A collar combines a purchased option (providing protection against adverse rate moves) with a sold option (capping participation in favourable rate moves). The sold option generates premium income that fully or partially offsets the cost of the purchased option.

A zero-cost collar is structured so that the premiums on the purchased and sold options exactly offset — meaning no upfront cash premium is paid. However, the company sacrifices the ability to benefit from rate moves beyond the sold option's strike level.

Collars are particularly useful in high-carry environments (common in EM currencies) where the cost of a simple option or forward is high. By accepting a capped upside, the company significantly reduces the cost of its downside protection.

Example

A Colombian fintech with USD credit line hedges USD/COP using a zero-cost collar: it buys a floor at 4,100 (protecting against COP depreciation) and sells a cap at 3,900 (foregoing benefit if COP strengthens beyond that level). Net premium cost: zero. Protection: fully defined.

Deaglo Relevance

The Deaglo Strategy Optimizer evaluates collars, zero-cost collars, and participating forwards against simple forwards — optimising across cost, protection level, and participation rate to find the most efficient structure for each client's specific objectives.

Counterparty Risk

The risk that the other party to a derivative contract will fail to fulfil its contractual obligations. In FX hedging, counterparty risk arises when the counterparty (typically a bank) defaults before a forward, option, or swap is settled.

▼

Counterparty risk in FX is the exposure that exists when the other party to a derivative contract may be unable to perform at settlement. For a forward contract, the exposure equals the mark-to-market value of the position — if that value is positive to the non-defaulting party, it may lose that amount in a default.

Counterparty risk is managed through:

- ISDA Master Agreements and Credit Support Annexes (CSAs) that govern collateral posting;

- Credit limits on individual counterparties;

- Diversification across multiple banking relationships; and (4) central clearing for standardised derivatives.

For funds and corporates operating in EM markets, counterparty risk can be elevated due to the use of local banks or the settlement risk in restricted currencies.

Cross-Currency Swap

A derivative contract in which two parties exchange principal and interest payments denominated in different currencies over a defined period. Cross-currency swaps are used to convert the currency of a debt obligation or investment into a preferred currency.

▼

A cross-currency swap (CCS) involves the exchange of both principal and interest payments in one currency for equivalent amounts in another currency. Unlike an FX swap (which only addresses principal), a CCS also converts ongoing interest payments — making it suitable for hedging the entire economic exposure of a foreign currency debt obligation over its full term.

They are commonly used by corporates that issue bonds in a foreign currency to access a deeper market or lower coupon, then swap the proceeds back to their functional currency. Infrastructure companies with USD project finance debt and local currency revenues often use CCS to align cash flows.

CCS are typically longer-dated than FX forwards (1–30 years) and are governed by ISDA documentation with collateral provisions.

Collateral & Margin Requirements

Assets posted by one party to a derivative contract to secure the counterparty against potential losses. As the mark-to-market value of a hedge moves adversely, additional collateral (a margin call) may be required — creating potential liquidity pressure within the hedge program.

▼

Under a Credit Support Annex (CSA), each party to a derivative agreement must post collateral when the MTM of their position moves against them beyond a defined threshold. This ensures that a default by either party would be covered by the collateral already posted.

For companies with large FX hedge books, collateral requirements can create significant liquidity pressure if exchange rates move sharply against the hedge positions. A company that has sold USD forward (to hedge USD revenues) would face collateral calls if USD strengthens materially — even though the underlying exposure is moving favourably.

This is the collateral/liquidity pressure situation surfaced by the Deaglo FX Diagnostic — identifying whether a hedge program's liquidity requirements have been properly sized against the company's available credit facilities.

Credit Support Annex (CSA)

A legal document that forms part of an ISDA Master Agreement. It specifies the terms under which collateral must be posted to cover the mark-to-market exposure of outstanding derivative transactions between two parties.

▼

A CSA sets out: the eligible collateral types, the thresholds below which no collateral is required, the minimum transfer amounts, the frequency of margin calls, and the interest rate applicable to cash collateral. Entities with strong credit ratings may negotiate higher thresholds (meaning larger exposures before collateral is required), while lower-rated entities may face zero thresholds.

Whether a CSA is in place significantly affects the pricing of FX derivatives — contracts without a CSA carry a higher Credit Valuation Adjustment (CVA) since the counterparty faces uncollateralised exposure. Negotiating uncollateralised lines (as Deaglo has done for certain clients) can significantly reduce the cost of hedging.

Deaglo Relevance

The Deaglo FX Diagnostic produces currency-neutral IRR attribution for PE and infrastructure funds — creating an LP-ready document that separates FX contribution from operational performance across vintages and portfolio companies.

Credit Support Annex (CSA)

A legal document that forms part of an ISDA Master Agreement. It specifies the terms under which collateral must be posted to cover the mark-to-market exposure of outstanding derivative transactions between two parties.

▼

A CSA sets out: the eligible collateral types, the thresholds below which no collateral is required, the minimum transfer amounts, the frequency of margin calls, and the interest rate applicable to cash collateral. Entities with strong credit ratings may negotiate higher thresholds (meaning larger exposures before collateral is required), while lower-rated entities may face zero thresholds.

Whether a CSA is in place significantly affects the pricing of FX derivatives — contracts without a CSA carry a higher Credit Valuation Adjustment (CVA) since the counterparty faces uncollateralised exposure. Negotiating uncollateralised lines (as Deaglo has done for certain clients) can significantly reduce the cost of hedging.

Deaglo Relevance

The Deaglo FX Diagnostic produces currency-neutral IRR attribution for PE and infrastructure funds — creating an LP-ready document that separates FX contribution from operational performance across vintages and portfolio companies.

Currency-Neutral Returns

Fund or portfolio performance calculated after removing the effect of exchange rate movements. Currency-neutral returns isolate investment performance from FX contribution, allowing investors to assess whether returns are driven by portfolio management or by favourable currency moves.

▼

Currency-neutral performance analysis answers the question: "what would this fund's IRR or NAV have been if exchange rates had stayed constant?" It strips out the FX contribution to returns — whether that contribution was positive (a tailwind from favourable rate moves) or negative (a headwind from adverse moves).

This analysis is increasingly important for PE and infrastructure funds operating in EM markets, particularly for LP reporting. LPs investing in a USD-denominated fund with BRL assets want to understand whether their returns reflect operational value creation at the portfolio company level, or whether they are simply a function of USD/BRL movements during the investment period.

XThe FX Diagnostic produces a formal currency-neutral IRR attribution — decomposing reported returns into FX-driven and operationally-driven components.

Conditional Value at Risk (CVaR)

Also called Expected Shortfall, CVaR measures the expected loss in the worst-case tail scenarios beyond the VaR threshold. It answers: "if losses do exceed the VaR level, how large are they on average?"

▼

CVaR (Conditional Value at Risk) extends VaR by focusing on the tail of the loss distribution. Where VaR answers "what is the worst loss at the 95th percentile?", CVaR answers "given that we are in the worst 5% of scenarios, what is the average loss?"

CVaR is increasingly preferred over VaR by risk managers and regulators because it better captures tail risk — the scenarios where losses are not just at the threshold but potentially much worse. It is sub-additive (unlike VaR), meaning portfolio CVaR is never greater than the sum of individual positions' CVaRs, making it more appropriate for portfolio risk aggregation.

Deaglo uses CVaR alongside CFaR, DV01, and duration in its systematic risk quantification framework — providing stress-tested views of potential outcomes under adverse market scenarios.

D

Deliverable vs Non-Deliverable Currency

A deliverable currency can be physically exchanged between parties at settlement; a non-deliverable currency cannot, due to capital controls or regulatory restrictions. FX transactions in non-deliverable currencies are cash-settled in a major currency (typically USD) via NDFs.

▼

Major currencies (USD, EUR, GBP, JPY, CHF) are fully deliverable — trades settle through physical exchange of currency. Many EM currencies are non-deliverable due to capital controls: at maturity, the NDF is settled in USD based on the difference between the agreed rate and the published fixing rate (e.g., PTAX for BRL, DOLAR REFERENCIA for MXN in certain contexts).

The distinction matters for: settlement logistics, counterparty risk (physical delivery creates settlement risk that NDFs avoid), liquidity (NDF markets may be more liquid than onshore markets for some currencies), and pricing (onshore and NDF implied rates can diverge significantly during periods of capital flow stress).

Key non-deliverable EM currencies include: BRL, CLP, COP, PEN, CNY, INR, KRW, TWD, IDR.

Delta (Option)

The sensitivity of an FX option's value to a one-unit change in the underlying exchange rate. A delta of 0.50 means the option's value moves by $0.50 for every $1 move in the underlying rate — it also approximates the probability that the option will expire in-the-money.

▼

Delta is the first-order sensitivity of an option's price to changes in the spot rate. It ranges from 0 (deep out-of-the-money) to 1.0 (deep in-the-money). At-the-money options typically have a delta of approximately 0.50. Delta is also used to express option-implied probability — a 25-delta option has roughly a 25% probability of expiring in-the-money.

For FX risk managers, delta is used to: measure the effective FX exposure of an options portfolio, size delta-hedging positions to remain market-neutral, and compare the "coverage" of different option structures. The Deaglo FX Options Builder and Strategy Simulator use delta as one of the parameters for optimising option-based hedging strategies.

DV01 (Dollar Value of a Basis Point)

DV01 measures the change in the value of a fixed income instrument or interest rate derivative for a one basis point (0.01%) move in interest rates. It quantifies interest rate sensitivity in dollar terms.

▼

DV01 (also called PVBP — Price Value of a Basis Point) is the primary metric for expressing interest rate risk in a portfolio or individual instrument. A DV01 of $10,000 means that if interest rates fall by 1 basis point (0.01%), the position gains $10,000 in value; if rates rise, it loses $10,000.

In the context of FX risk management for infrastructure companies and corporate borrowers with floating-rate USD debt, DV01 is used to size interest rate hedges (such as interest rate swaps) alongside FX hedges. Deaglo's risk quantification framework uses DV01 alongside CFaR, duration, and CVaR to provide a complete picture of market risk.

E

Economic Risk (Operating Exposure)

The risk that exchange rate changes will affect a company's competitive position, market value, and long-run cash flows — beyond the near-term transactional or accounting effects. Economic risk is structural and affects a company's ability to compete in its markets.

▼

Economic risk (also called operating exposure) is the broadest form of FX risk. It captures how persistent exchange rate shifts affect a company's competitive dynamics: its pricing power relative to foreign competitors, its ability to source inputs cost-effectively, and the ultimate value of its cash-generating operations.

Unlike transaction risk (which covers specific contractual cash flows) or translation risk (which covers the accounting restatement of foreign assets), economic risk affects the intrinsic business value. A Mexican manufacturer whose USD-denominated equipment costs become structurally more expensive due to peso weakness may lose market share — even if individual transactions are hedged.

Economic risk is harder to hedge than transaction or translation risk because it is forward-looking and uncertain. Long-dated options, structured solutions, and operational hedging (natural hedges, supplier diversification) are the primary tools.

Exposure Mapping

The structured process of identifying, quantifying, and categorising all FX exposures across an organisation — payables, receivables, debt obligations, intercompany flows, and off-balance sheet items — to create a complete view of currency risk before any hedging decision is made.

▼

Exposure mapping is the foundation of any effective FX risk management program. Without a complete and accurate picture of what is exposed, where, in which currencies, and on what timeline, no hedging strategy can be properly designed or sized.

A thorough exposure map covers: commercial exposures (revenues and costs in foreign currencies), balance sheet exposures (foreign currency assets and liabilities), financing exposures (USD debt in a company with local currency revenues), intercompany exposures (loans and trading between entities), and forecast exposures (budgeted future cash flows).

The Deaglo platform consolidates payables, receivables, cash flows, and intercompany positions to build a real-time exposure map — identifying concentrations and emerging risks before they affect performance.

Deaglo Relevance

Deaglo's Exposure Management module consolidates all FX positions in one view — separating hedged from unhedged exposure, identifying currency concentrations, and flagging risks before they distort revenue, EBITDA, or reported fund returns.

F

Fair Value Hedge

A hedge accounting designation that protects against changes in the fair value of a recognised asset, liability, or firm commitment. Both the hedging instrument and the hedged item are remeasured to fair value, with changes in both recognised immediately in the income statement — they offset each other, eliminating net P&L volatility.

▼

In a fair value hedge, changes in the fair value of both the derivative (the hedge) and the hedged item are recognised in the income statement in the same period. Because they move in opposite directions, they substantially offset each other — reducing or eliminating the net P&L impact.

Fair value hedges are commonly used to hedge fixed-rate debt: by converting fixed-rate payments to floating-rate via an interest rate swap, the entity hedges the change in fair value of the debt attributable to interest rate movements. In FX, fair value hedges are used to protect the value of a foreign currency monetary item (such as a foreign currency receivable or payable) on the balance sheet.

Contrast with a cash flow hedge, where the hedge gain/loss is deferred in OCI and matched against the cash flow when it occurs.

FX Forward

A binding contract between two parties to exchange a specified amount of one currency for another at a predetermined rate (the forward rate) on a future date. FX forwards eliminate exchange rate uncertainty by locking in a rate today for a transaction that will settle in the future.

▼

An FX forward is the most widely used FX hedging instrument. It is an over-the-counter (OTC) contract that obligates both parties to exchange currencies at a specified rate on a specified future date. The forward rate is derived from the current spot rate adjusted for the interest rate differential between the two currencies (via covered interest rate parity).

When to use: Forwards are ideal when the timing and amount of the underlying FX exposure are known with high certainty — for example, a scheduled debt repayment, a confirmed foreign currency receivable, or a fixed-cost import contract. They provide complete certainty over the exchange rate but no ability to benefit from favourable rate movements after the forward is executed.

Key features: Flexible tenors (1 day to 5+ years), fully customisable notional amounts, no upfront premium (unlike options), and typically settled by physical delivery of currencies at maturity — though flexible forwards allow early or partial delivery.

Limitations: Forwards are obligations, not rights. If market rates move favourably after the forward is executed, the entity cannot benefit. Opportunity cost can be significant in volatile EM markets.

Example

A Brazilian PE fund with USD-denominated LP commitments contracts a USD/BRL forward at 5.20 for settlement in 90 days, locking in the conversion rate for its next distribution regardless of where USD/BRL trades between now and then. If the rate moves to 5.50 by settlement, the fund is protected. If it moves to 4.90, the fund has locked in a less favourable rate but has eliminated the uncertainty.

Deaglo Relevance

Deaglo's Strategy Simulator models FX forward strategies against alternatives — showing the cost, protection level, and opportunity cost of forwards compared to options, collars, and structured solutions, so clients can choose the optimal structure for their specific exposure and risk appetite.

FX Option

A contract giving the buyer the right, but not the obligation, to exchange currency at a specified rate (the strike) on or before a set date. The buyer pays an upfront premium for this flexibility. Unlike forwards, options allow participation in favourable rate moves while providing protection against adverse moves.

▼

FX options come in two forms: a call option gives the right to buy the base currency at the strike rate, and a put option gives the right to sell. The buyer pays a premium for this optionality. If the market rate at expiry is better than the strike rate, the option is not exercised and the buyer transacts at the prevailing market rate. If the market rate is worse than the strike, the option is exercised and the buyer transacts at the protected rate.

Options are most valuable when there is significant uncertainty over both the size and direction of future exchange rate moves, or when the underlying exposure itself is uncertain (e.g., a bid for a contract that may or may not be won). The premium paid is the maximum cost of the hedge.

Option premium is a function of: time to expiry (longer = more expensive), implied volatility (higher volatility = more expensive), the distance of the strike from the current spot rate, and the interest rate differential.

FX Risk (Currency Risk)

The risk that changes in exchange rates will adversely affect a company's financial results, cash flows, or the value of its assets and liabilities. FX risk exists whenever a company has revenues, costs, debt, investments, or operations denominated in a currency different from its reporting currency.

▼

FX risk (or currency risk) encompasses three primary dimensions: transaction risk (the risk that exchange rate moves affect the cost or value of specific contractual cash flows), translation risk (the risk that foreign currency financial statements produce different results when expressed in the reporting currency), and economic risk (the risk that rate changes affect a company's competitive position and intrinsic value).

FX risk is particularly acute for organisations with cross-border operations — companies with USD revenues and local costs, funds with USD denomination and EM assets, or infrastructure entities with USD debt and local tariff revenues. In each case, exchange rate movements affect outcomes independently of the quality of the underlying business or investment.

The key insight the Deaglo FX Diagnostic communicates: most organisations have more FX risk than they realise, because much of it is embedded in the business model or capital structure rather than in obvious foreign currency transactions.

FX Overlay

A portfolio-level currency hedging strategy that manages aggregate FX risk across multiple investments or share classes using derivatives, without altering the underlying portfolio holdings. FX overlays are used by asset managers to reduce currency-driven volatility in reported returns.

▼

An FX overlay program manages currency risk at the portfolio level by layering derivative instruments — typically forwards or swaps — on top of existing holdings without changing the underlying investments. The overlay effectively separates the currency decision from the investment decision.

Overlay strategies range from passive (maintaining a fixed hedge ratio, e.g., 50% of all non-base-currency exposures hedged) to active (dynamically adjusting hedge ratios based on market views or risk triggers). For PE and infrastructure funds with long-dated assets in EM currencies, overlay programs are typically structured around NDF ladders rolled on a monthly or quarterly basis.

The FX Diagnostic assesses the effectiveness and cost efficiency of the overlay program — identifying where hedge ratios have drifted and where the overlay is no longer aligned to the underlying portfolio composition.

FX Swap

A transaction that combines a spot FX trade with a simultaneous forward trade in the opposite direction. FX swaps are used to manage short-term funding needs across currencies — effectively borrowing one currency while lending another for a defined period.

▼

An FX swap involves two legs: an initial spot exchange of currencies, and a forward exchange at a different rate at maturity. The difference between the spot and forward rates reflects the interest rate differential between the two currencies.

FX swaps are the most heavily traded instrument in the FX market (larger by daily volume than spot transactions). They are primarily used for short-term cash management, funding, and rolling existing hedge positions. For companies that use FX forwards to hedge recurring exposures, an FX swap is the mechanism used to extend (roll) a maturing forward into the next period.

They are distinct from cross-currency swaps, which exchange both principal and interest payments over longer periods.

Forward Rate

The exchange rate agreed today for a currency transaction to be settled at a specified future date. The forward rate is calculated from the spot rate adjusted for the interest rate differential between the two currencies, based on covered interest rate parity.

▼

The forward rate is not a prediction of where the spot rate will be in the future — it is a mathematical derivation from the current spot rate and the interest rate differential between two currencies. This ensures there are no risk-free arbitrage opportunities between borrowing in one currency and investing in another (covered interest rate parity).

If a currency has higher interest rates than USD, its forward rate will be at a discount to the spot rate — meaning it takes more of that currency to buy one USD in the forward market than in the spot market. This forward discount reflects the carry cost of hedging that currency.

Example

If USD/BRL spot is 5.00, US interest rates are 5%, and Brazilian rates are 12%, a 12-month forward will price BRL at a discount: approximately USD/BRL 5.33. A Brazilian fund hedging USD exposure pays this approximately 6.6% carry cost annually for full certainty of the exchange rate.

Forward Points

The premium or discount applied to the spot exchange rate to arrive at the forward rate. Forward points reflect the interest rate differential between two currencies and are expressed in pips or basis points.

▼

Forward points are the numerical adjustment made to the spot rate to derive the forward rate: Forward Rate = Spot Rate + Forward Points. Positive forward points mean the forward currency trades at a premium to spot (it is more expensive in the forward market); negative points indicate a discount.

The magnitude of forward points increases with tenor — a 3-year forward carries three times more interest rate differential than a 1-year forward. In high-rate EM currencies (BRL, COP, PEN), forward points on USD-priced forwards can be substantial — representing a significant component of the total cost of hedging.

Understanding forward points is essential for benchmarking hedging costs and choosing between tenors and instruments.

H

Hedge Documentation

The formal written record required at hedge inception to qualify for hedge accounting under IFRS 9 or ASC 815. Documentation must describe the hedging relationship, the risk management objective, the hedged item, the hedging instrument, and the approach to assessing hedge effectiveness.

▼

Hedge accounting cannot be applied retrospectively. Documentation must be completed at the time the hedge is designated — before any subsequent changes in the market value of the instruments. Without adequate documentation, a hedge that qualifies economically may still fail to qualify for hedge accounting, forcing all derivative gains and losses through the income statement immediately.

Required documentation elements include: the entity's risk management objective and strategy, identification of the hedged item (e.g., the first 10 quarterly USD/MXN purchases), identification of the hedging instrument (e.g., a series of 10 forward contracts), the type of hedge (cash flow, fair value, or net investment), and the method for assessing ongoing hedge effectiveness.

Deaglo generates structured hedge documentation as part of its advisory service — reducing the compliance burden on treasury and ensuring audit readiness.

Hedge Effectiveness

The formal written record required at hedge inception to qualify for hedge accounting under IFRS 9 or ASC 815. Documentation must describe the hedging relationship, the risk management objective, the hedged item, the hedging instrument, and the approach to assessing hedge effectiveness.

▼

Hedge effectiveness is the degree to which the changes in fair value or cash flows of the hedging instrument offset the changes in the hedged item. Under hedge accounting standards, the relationship must be highly effective — historically defined as within an 80–125% offset range, though IFRS 9 replaced this with a more principles-based qualitative assessment focused on the economic relationship.

Three criteria must be met under IFRS 9 for a hedge to qualify: (1) there must be an economic relationship between the hedging instrument and the hedged item; (2) the effect of credit risk must not dominate the value changes that result from that economic relationship; and (3) the hedge ratio must reflect the actual quantities used in the hedging relationship.

Prospective effectiveness is assessed at inception and throughout the hedge term to confirm the hedge continues to qualify. Retrospective effectiveness (under older standards) measured whether the hedge actually offset changes in the past period.

An ineffective portion of a hedge must be recognised immediately in the income statement even under cash flow hedge accounting.

Deaglo Relevance

Deaglo's platform generates ongoing hedge effectiveness documentation and testing output — producing audit-ready reports that satisfy IFRS 9 and ASC 815 requirements without manual spreadsheet work by the treasury team.

Hedge Ratio

The proportion of a total FX or interest rate exposure that is covered by hedging instruments. A hedge ratio of 75% means 75% of the exposure is hedged; the remaining 25% is open (unhedged). The appropriate hedge ratio depends on risk appetite, cost of hedging, certainty of the underlying exposure, and governance policy.

▼

The hedge ratio is a fundamental parameter of any FX risk management program. A 100% hedge ratio eliminates exchange rate uncertainty but maximises carry cost and eliminates any potential benefit from favourable rate moves. A 0% hedge ratio retains full exposure to exchange rate movements — both beneficial and adverse.

In practice, most programmes hedge between 50–100% of near-term exposures (where certainty is high) and progressively less for more distant exposures (where both the direction and magnitude of exposure may be uncertain). Hedging policy documentation specifies the target hedge ratio range and the minimum and maximum permitted levels.

The FX Diagnostic compares the current hedge ratio against the actual exposure — identifying where the ratio has drifted from policy targets and where material gaps exist.

Hedged Share Class

A fund share class that uses FX derivatives to minimise the exchange rate difference between the fund's base currency and the investor's reference currency. It is designed so that investor returns reflect the fund's underlying investment performance rather than currency movements between the fund and the investor's home market.

▼

A hedged share class is created when a fund manager wants to offer investors exposure to the fund's portfolio without the additional risk (or return) of currency movements. The fund manager (or a specialist overlay manager) uses FX forwards or NDFs to hedge the currency difference between the fund's base currency and the share class currency.

Managing hedged share classes involves: monthly rebalancing of the hedge as NAV and subscriptions/redemptions change, tracking error management, carry cost allocation between share classes, and proper accounting and LP reporting of the hedge program.

Deaglo specialises in creating and managing hedged share class programs for PE and infrastructure funds operating in LatAm and other EM markets.

Example

A USD-base fund investing in BRL assets may offer a EUR-denominated share class. The hedged version uses EUR/USD forwards so that EUR investors experience returns close to those of USD investors — without bearing EUR/USD exchange rate exposure on top of the BRL/USD exposure already embedded in the portfolio.

Deaglo Relevance

Deaglo's advisory and platform services cover the full lifecycle of hedged share class management — from initial strategy design and NDF line negotiation through monthly rebalancing, LP reporting, and IFRS 9 compliance documentation.

I

IFRS 9 (Financial Instruments)

The International Financial Reporting Standard governing the recognition, classification, measurement, and hedge accounting of financial instruments. Under IFRS 9, qualifying hedge relationships allow derivative gains and losses to be deferred in Other Comprehensive Income (OCI), reducing income statement volatility.

▼

IFRS 9 replaced IAS 39 and introduced a significantly reformed hedge accounting model designed to better align accounting treatment with risk management activities. Key improvements over IAS 39 include: replacement of the rigid 80–125% retrospective effectiveness test with a qualitative principles-based approach, allowing more hedging instruments and hedged items to qualify, and providing more flexibility in rebalancing hedge relationships without termination.

Under IFRS 9's hedge accounting model, three types of hedging relationships are recognised: cash flow hedges, fair value hedges, and hedges of net investments in foreign operations.

For IFRS 9 compliance, entities must: document the hedging relationship at inception, demonstrate an economic relationship between the instrument and the hedged item, assess effectiveness prospectively on an ongoing basis, and maintain complete hedge accounting records. The standard applies to entities reporting under IFRS — the majority of non-US publicly listed companies globally.

Deaglo Relevance

Deaglo supports full IFRS 9 hedge accounting compliance — generating designation documentation, effectiveness testing, and reporting outputs that are trusted by LPs and auditors across fund and corporate clients.

Implied Volatility

The market's consensus expectation of future currency volatility, derived from current option prices. Implied volatility is the primary driver of FX option premiums — higher implied volatility means more expensive options and higher hedging costs.

▼

Implied volatility (IV) is extracted from current market option prices using an option pricing model (typically Black-Scholes for vanilla FX options). It represents the annualised standard deviation of expected currency returns implied by the options market — effectively a consensus view on how much the exchange rate is expected to move.

For FX risk managers, implied volatility is important because: (1) it drives the cost of option-based hedges — high IV periods make options expensive but also make them most valuable; (2) it can be used to benchmark market fear and uncertainty; and (3) it influences the cost-benefit trade-off between different hedging instruments (forwards vs options vs structured products).

EM currency pairs typically carry higher implied volatility than G10 pairs, reflecting greater uncertainty, thinner liquidity, and political/economic risk premium.

Interest Rate Parity

The market's consensus expectation of future currency volatility, derived from current option prices. Implied volatility is the primary driver of FX option premiums — higher implied volatility means more expensive options and higher hedging costs.

▼

Covered interest rate parity (CIP) is a no-arbitrage condition: if you borrow in USD, convert to BRL, invest at Brazilian interest rates, and simultaneously lock in the reconversion back to USD via a forward contract, you should earn exactly the same return as investing in USD directly. If you earned more, arbitrageurs would exploit it until the rates equalised.

This means the forward rate is not a market prediction of where spot will be — it is a mathematical consequence of current interest rates. The forward discount on BRL relative to USD simply reflects Brazil's higher interest rates. A hedger locking in the BRL forward is effectively paying the interest rate differential as the cost of certainty.

Understanding interest rate parity is essential for interpreting forward rates, evaluating carry costs, and making informed decisions about hedging tenor and instrument selection.

Interest Rate Risk

The risk that changes in interest rates will adversely affect the cost of borrowing, the value of fixed income assets, or the cash flow from floating-rate instruments. For companies with variable-rate USD debt and local currency revenues, interest rate and FX risks are closely interrelated.

▼

Interest rate risk affects corporates primarily through: (1) the cost of floating-rate debt — a rise in SOFR or local benchmark rates increases interest payments; (2) the value of fixed-rate assets or liabilities — rising rates reduce the present value of fixed cash flows; and (3) the interaction with FX risk — in cross-currency debt structures, interest rate and currency movements compound each other's impact on total debt service cost.

Deaglo manages interest rate risk alongside FX risk — recognising that for infrastructure companies with USD project finance debt and local currency revenues, the two risks are inseparable. Tailored rate-hedging strategies cover floating-rate debt, term loans, revolvers, and multi-currency facilities, with systematic quantification using CFaR, DV01, duration, IRR, and CVaR.

IRR (Internal Rate of Return) — FX Context

In the context of FX risk management, IRR is the fund return metric most directly distorted by unmanaged currency exposure. Exchange rate movements between investment and exit can significantly inflate or deflate reported IRR, independently of underlying portfolio performance.

▼

IRR (Internal Rate of Return) is the discount rate that makes the net present value of a fund's cash flows equal to zero — in practice, the annualised return on invested capital. For a USD-denominated fund investing in EM assets, reported IRR is the product of both the underlying investment performance and the exchange rate movement between entry and exit.

A fund that invested in Brazilian infrastructure in 2016 (at USD/BRL 3.50) and exited in 2021 (at USD/BRL 5.50) would show a significantly lower USD-denominated IRR than the BRL-denominated return would imply — simply due to BRL depreciation, regardless of operational performance. Conversely, an investment made when BRL was weak may show inflated USD returns if BRL strengthens at exit.

The FX Diagnostic produces a currency-neutral IRR analysis — separating the exchange rate contribution from the operational IRR and giving fund managers and LPs a defensible attribution framework.

ISDA Master Agreement

The standardised legal contract published by the International Swaps and Derivatives Association that governs over-the-counter derivative transactions between two parties. All FX forwards, options, and swaps between institutional counterparties are typically traded under an ISDA agreement.

▼

The ISDA Master Agreement is the legal foundation for bilateral OTC derivative trading. It covers: the definitions of events of default and termination events, close-out netting provisions (allowing all positions to be offset against each other in a default), representations and warranties, and governing law. A Credit Support Annex (CSA) is typically attached to address collateral arrangements.

Having an ISDA agreement in place with a counterparty is a prerequisite for trading FX derivatives with that bank. For funds and corporates hedging EM exposures, negotiating ISDA agreements — particularly with local EM banks — is a critical step in establishing a cost-effective hedging program. Uncollateralised ISDA lines (obtained without a CSA) reduce hedging costs by eliminating the need to post collateral.

M

Mark-to-Market (MTM)

The process of revaluing a financial instrument at its current market price — recording unrealised gains and losses based on where the instrument could be closed out today. For FX derivatives, MTM value changes as exchange rates move.

▼

Mark-to-market (MTM) is the current fair value of a derivative position. A forward contract entered into at USD/BRL 5.00 has a positive MTM if the current forward rate has moved to 5.30 (for the USD seller) and a negative MTM if it has moved to 4.70.

UMTM is important for:

- Balance sheet reporting — IFRS 9 and ASC 815 require derivatives to be recognised at fair value;

- Collateral management — negative MTM positions may trigger margin calls under a CSA;

- Counterparty risk management — positive MTM represents credit exposure to the counterparty; and

- Hedge effectiveness assessment — comparing MTM changes on the hedge against changes in the hedged item.

The Deaglo Client Portal provides real-time MTM tracking across all outstanding hedge positions — alerting account managers to adverse spot movements, expiring trades, and required next steps.

Monte Carlo Simulation

A computational technique that runs thousands of randomly generated exchange rate scenarios — each drawn from a statistical distribution calibrated to historical volatility — to model the full range of possible outcomes for a hedged or unhedged FX position. It produces probability distributions of P&L, cash flow, and hedge performance, rather than single-point estimates.

▼

Monte Carlo simulation generates a large number of hypothetical future exchange rate paths — typically 10,000 to 100,000 — by repeatedly drawing random returns from a calibrated statistical model (commonly geometric Brownian motion, jump-diffusion, or a GARCH-based process for EM currencies). Each simulated path produces an outcome (a P&L, a cash flow shortfall, a hedge gain or loss), and the full set of outcomes forms a probability distribution.

This distribution directly answers questions that single-point or parametric methods cannot: "What is the range of possible P&L outcomes for our hedge program over the next 12 months?" or "In how many of 10,000 scenarios does our debt service coverage ratio fall below the covenant threshold?"

Why it matters for FX risk: Real FX markets — especially EM currencies — exhibit non-normal return distributions: fat tails, asymmetry, and volatility clustering. Parametric VaR assumes normality and systematically underestimates tail risk. Monte Carlo simulation can incorporate richer statistical models (stochastic volatility, mean reversion, sudden devaluation jumps) that better reflect EM currency behaviour.

Key outputs from a Monte Carlo FX simulation:

- P&L distribution — the histogram of simulated hedge gains and losses across all paths, showing the most likely outcome, the median, and the tail scenarios at the 5th and 1st percentiles.

- Monte Carlo VaR — the loss at the chosen confidence level (e.g., 95th or 99th percentile) derived from the simulated distribution rather than a parametric formula.

- Expected Shortfall (CVaR) — the average loss in the worst X% of simulated scenarios.

- Hedge performance distribution — for each simulated path, how well did the hedge offset the underlying exposure? This directly feeds hedge effectiveness analysis.

- Scenario fan chart — a visual showing the range of simulated exchange rate paths over time, with percentile bands (10th, 25th, 50th, 75th, 90th) illustrating the uncertainty cone as the horizon extends.

Monte Carlo vs Scenario Analysis: Scenario analysis models a small number of manually chosen, named scenarios ("USD/BRL depreciates 15%"). Monte Carlo samples thousands of statistically consistent paths — including extreme events that analysts may not explicitly consider — providing a more complete view of the risk landscape.

Deaglo's Strategy Simulator uses Monte Carlo simulation as its core engine: running simulated exchange rate paths through each candidate hedge structure to compare expected cost, worst-case outcome, and probability of breaching user-defined thresholds across all modelled scenarios. This is how the platform evaluates forwards versus collars versus structured solutions — not on a single-path basis, but across the full probability distribution of outcomes.

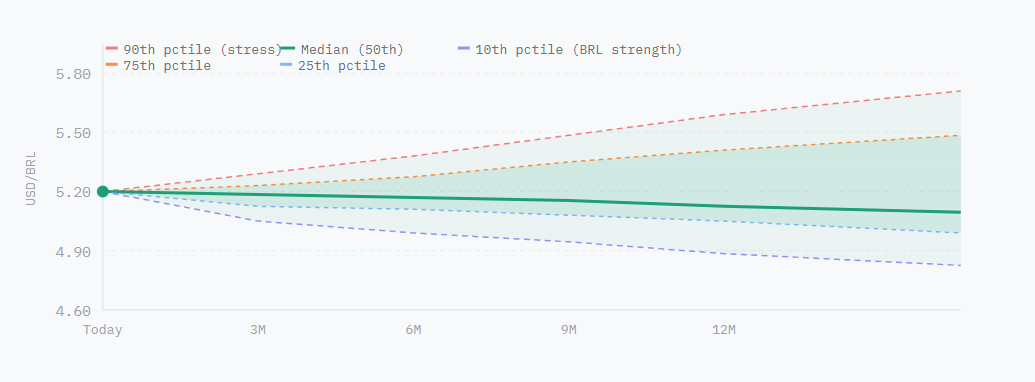

Worked example — reading a Monte Carlo fan chart

A Deaglo simulation for USD/BRL over 12 months starting at spot 5.20 might show: median path at 5.35 (reflecting carry), 75th percentile at 5.70 (BRL depreciation scenario), 90th percentile at 6.10 (stress scenario), 25th percentile at 5.05 (BRL strengthening), 10th percentile at 4.75. A fund reading this knows: there is a 10% probability that BRL strengthens beyond 4.75 — at which point an unhedged USD position gains substantially — and a 10% probability it weakens beyond 6.10, where the hedge payoff becomes critical. The hedge program is sized against the full distribution, not a single number.

Monte Carlo Fan Chart — Simulated USD/BRL paths (illustrative, 10,000 runs)

Deaglo Relevance

Deaglo's Strategy Simulator runs Monte Carlo simulations across thousands of exchange rate scenarios to compare hedge structures — producing probability-weighted performance comparisons that show each strategy's expected cost, worst-case outcome, and probability of breaching defined thresholds. This powers the Strategy Optimizer's machine learning engine, which uses Monte Carlo outputs as training data for its optimisation across up to nine hedging parameters.

N

Natural Hedge

A reduction in FX risk achieved through the structure of business operations rather than financial instruments. A natural hedge exists when revenues and costs in the same foreign currency offset each other — so that exchange rate movements affect both sides of the P&L in the same direction, reducing the net FX exposure.

▼

A natural hedge is created when a company structures its operations so that foreign currency cash inflows and outflows offset each other. A company that exports in USD and sources its key inputs in USD has a natural hedge — a weakening of the local currency improves export competitiveness while reducing the local currency cost of USD inputs, with the effects largely cancelling out.

Natural hedges are the most cost-effective form of FX risk management because they require no derivative instruments and incur no carry cost. However, they are rarely complete — the timing, amount, and currency of inflows and outflows seldom match perfectly enough to eliminate all residual FX exposure.

Exposure mapping is the tool used to identify and quantify natural hedges before sizing any financial hedging program — only the residual, unmatched exposure requires derivative hedging.

NAV (Net Asset Value) — FX Context

The per-unit or total value of a fund's assets minus liabilities, reported in the fund's base currency. In the FX risk management context, NAV is particularly vulnerable to translation risk — exchange rate movements cause reported NAV to fluctuate independently of underlying portfolio performance.

▼

For a USD-denominated fund holding EM assets, NAV is calculated by translating the value of all assets and liabilities into USD at the prevailing exchange rate at each reporting date. Even if the underlying assets are performing exactly as expected in local currency terms, a depreciating local currency will reduce the USD NAV — creating reported losses that have nothing to do with portfolio management.

This NAV volatility driven by FX is one of the primary concerns the Deaglo FX Diagnostic addresses for fund managers. The diagnostic decomposes quarterly NAV changes into:

- Investment performance contribution,

- FX translation effect, and

- Hedge program offset

Giving fund managers and LPs a clean view of what is driving reported results.

Non-Deliverable Forward (NDF)

A cash-settled forward contract used to hedge currencies that are restricted, illiquid, or not freely convertible. At maturity, only the net difference between the contracted rate and the prevailing spot fixing is settled in a major currency (typically USD) — no physical exchange of the restricted currency occurs.

▼

An NDF functions like a deliverable forward in every respect except settlement. Rather than exchanging the two currencies at maturity, the parties calculate the net P&L based on the difference between the contracted forward rate and the official spot fixing rate on the expiry date. The net amount is settled in USD (or another freely convertible currency).

NDFs are the primary hedging instrument for EM currencies subject to capital controls: Brazilian Real (BRL), Colombian Peso (COP), Peruvian Sol (PEN), Chilean Peso (CLP in certain tenors), as well as Asian currencies including CNY, INR, and KRW. The BRL NDF market is one of the largest and most liquid NDF markets globally.

- Settlement: The BRL NDF fixes against the PTAX rate published by the Banco Central do Brasil. COP NDFs typically fix against the TRM. PEN NDFs fix against the SBS rate.

- Pricing: NDF pricing reflects the interest rate differential between the EM currency and USD, adjusted for market liquidity and capital control risk premium. In periods of market stress, NDF rates can diverge significantly from onshore rates.

- Key advantage: No need to establish local banking relationships, local accounts, or navigate capital control reporting requirements. NDFs can be executed internationally with global banking counterparties under standard ISDA documentation.

Example

A US PE fund with BRL-denominated portfolio assets contracts a 12-month USD/BRL NDF at 5.40. At maturity, if the PTAX fixing is 5.80 (BRL has depreciated), the fund receives the difference (0.40 per USD of notional) in USD — compensating for the loss in BRL value of the assets when translated back to USD.

Deaglo Relevance

Deaglo specialises in NDF hedging for LatAm currencies — structuring NDF programs for PE funds, infrastructure companies, and fintechs with BRL, COP, PEN, and CLP exposures. Deaglo has negotiated uncollateralised NDF lines for clients, substantially reducing the cost of carry on EM hedging programs.

Notional Value

The face value of a derivative contract — the amount of the underlying currency on which the contract's cash flows are calculated. Notional value does not represent the amount at risk (which is typically the MTM value), but it determines the scale of gains, losses, and settlement amounts.

▼

The notional value (or principal amount) of an FX derivative is the currency amount that the contract references — for example, USD 10 million in a USD/BRL forward. Gains, losses, and settlement amounts are calculated as a percentage of this notional. The notional is not exchanged (except at settlement for deliverable forwards) — only the net P&L or differential (in the case of NDFs) is exchanged.

In aggregate hedge books, total notional outstanding is used to measure the scale of the hedging program and compare it against the underlying exposure — calculating the hedge ratio. A USD 5 million notional hedge against a USD 10 million exposure represents a 50% hedge ratio.

O

Other Comprehensive Income (OCI)

A component of shareholders' equity that captures unrealised gains and losses that bypass the income statement. Under cash flow hedge accounting (IFRS 9 / ASC 815), the effective portion of a hedge's gain or loss is deferred in OCI until the hedged item affects earnings.

▼

OCI (Other Comprehensive Income) is the financial reporting mechanism that makes cash flow hedge accounting work. Instead of recording hedge gains and losses immediately in the income statement — which would create P&L volatility when markets move between hedge inception and settlement — the effective hedge amounts are held in OCI (a sub-component of equity) and released to the income statement when and as the hedged transaction occurs.

This matching principle is the core value of hedge accounting: the income statement reflects the hedged rate (the rate locked in via the derivative) rather than the spot rate at the transaction date, significantly reducing reported earnings volatility.

The OCI balance related to hedge accounting represents the cumulative deferred gain or loss on qualifying hedges. Analysts reviewing financial statements should include OCI movement in their assessment of the total P&L impact of the entity's FX risk management program.

Onshore vs Offshore Rate

An onshore rate is the exchange rate available within a country's domestic market, subject to local regulations and capital controls. An offshore rate (typically the NDF-implied or CNH rate) trades internationally without those restrictions. The spread between onshore and offshore rates reflects the cost of capital controls and domestic monetary conditions.

▼

In countries with capital controls or restricted currency regimes, two distinct exchange rate markets often coexist: the onshore market (accessible only to residents or entities with local accounts and regulatory approval) and the offshore market (accessible to international participants and free of local restrictions).

For EM currencies, the BRL illustrates this well: the onshore USD/BRL rate (fixing via PTAX) reflects domestic Brazilian monetary conditions and is used by Brazilian entities. The offshore NDF-implied rate trades internationally and can diverge from the PTAX during periods of capital flow pressure — creating a basis risk for international entities hedging BRL exposure via NDFs but conducting business at onshore rates.

Understanding the onshore/offshore dynamic is essential for EM hedging strategy: it affects instrument selection, fixing rate choice, basis risk management, and the total cost of hedging.

P

Participating Forward

A hybrid hedging instrument that provides guaranteed protection at a specified rate (like a forward) while retaining partial participation in favourable rate moves (like an option). The protection rate is less favourable than a standard forward, but no upfront premium is required.

▼

A participating forward combines protection (a worst-case rate guarantee) with partial upside participation. The structure works by: buying a vanilla option at a slightly worse strike than the current forward rate, and selling a smaller notional of the same option to fund the premium. The result: full notional protection at a defined worst-case rate, plus partial (e.g., 50%) participation in favourable rate moves beyond that level.

For example, a 50% participating forward at USD/BRL 5.20 would guarantee a minimum BRL amount equivalent to 5.20 per USD, while allowing the hedger to benefit from 50% of any BRL strengthening beyond 5.20. The cost: zero upfront premium, but the guaranteed rate is worse than the current outright forward.

Participating forwards are particularly attractive in high-carry EM environments where the full option premium would be prohibitively expensive but the hedger wants to retain some directional exposure.

Proxy Hedge

A hedge that uses a different but correlated currency to manage an exposure in an illiquid or inaccessible currency. Proxy hedges introduce basis risk — the risk that the proxy currency and the target currency do not move in perfect correlation.

▼

When a target currency is illiquid, inaccessible, or prohibitively expensive to hedge directly, a proxy hedge uses a more liquid, correlated currency. For example, a fund with exposure to the Peruvian Sol (PEN) might hedge using the Colombian Peso (COP) if PEN liquidity is poor at the required tenor — relying on the historical correlation between the two EM currency pairs.

The effectiveness of a proxy hedge depends on the stability of the correlation between the two currencies. During periods of global stress, EM correlations often increase (diversification breaks down), making proxy hedges more effective. During country-specific crises, correlations can diverge dramatically, making proxy hedges ineffective or counterproductive.

Proxy hedges must be carefully documented and assessed for basis risk as part of any hedge accounting designation.

R

Restricted Currency

A currency that cannot be freely exchanged outside its domestic market due to government-imposed capital controls or restrictions on convertibility. FX transactions in restricted currencies must be conducted through approved local channels or hedged via NDFs offshore.

▼

Restricted currencies (also called controlled or non-deliverable currencies) are those where the government limits or controls capital flows. Restrictions can take many forms: limits on the amount that can be converted, requirements for prior approval, taxes on outflows (e.g., Brazil's IOF tax historically), or outright prohibition on offshore settlement.

For international investors and multinational corporations, restricted currencies create significant FX risk management complexity. The key implications:

- Physical currency cannot easily be moved offshore, so hedging must be done via NDFs;

- Onshore and offshore rates may diverge;

- Local banking relationships and regulatory approvals may be required;

- Repatriation of investment returns may be subject to delays or taxes.

Major restricted or semi-restricted currencies in LatAm: BRL (Brazil), COP (Colombia, restricted for certain flows), PEN (Peru, partially), ARS (Argentina, highly restricted), VES (Venezuela, effectively non-convertible).

Rollover (FX Hedge)

The extension of an expiring FX hedge position into a new period via an FX swap. When a forward or NDF matures and the underlying exposure continues beyond the maturity date, a rollover extends the hedge by simultaneously settling the maturing contract and entering a new forward at prevailing market rates.

▼

Rolling a hedge involves using an FX swap to close the expiring position at the current spot rate and simultaneously open a new forward at the current forward rate for the extended maturity. The net cost or benefit of the roll reflects the FX swap points — the interest rate differential for the extension period.

Rolling is a routine part of managing ongoing FX exposures — particularly for funds that hedge share classes on a monthly or quarterly cycle and for corporates with recurring import or export flows. The mechanics, timing, and cost of rolling need to be managed actively because the roll rate can diverge from budgeted rates in volatile markets.

For EM currencies with significant carry costs, rollovers accumulate the interest rate differential at each extension period, making the total cost of maintaining a long-dated hedge substantially higher than a single-period hedge.

S

Scenario Analysis & Stress Testing

The process of modelling how specific exchange rate or interest rate scenarios — such as a 10% USD/BRL depreciation, a parallel rate curve shift, or a market stress event — would affect a company's P&L, cash flows, covenant headroom, or hedge book value.

▼

Scenario analysis models a specific set of market conditions and measures their impact on the entity. Unlike VaR (which uses statistical distributions), scenario analysis uses explicitly defined rate moves — allowing management to ask and answer specific questions: "what happens to our debt service cost if USD/MXN moves to 20?" or "what would our Q4 EBITDA look like if BRL depreciates 15% before year-end?"

Stress testing is a subset of scenario analysis that focuses on extreme, low-probability events — tail scenarios rather than central cases. Regulators increasingly require banks and systemically important entities to conduct regular stress tests; similar disciplines are now expected of well-governed corporate treasury operations and fund managers.

Deaglo's platform performs scenario and shock analysis — including parallel and non-parallel interest rate curve shifts — to stress-test debt service outcomes and model the impact of extreme market events on hedge programs and exposures.

Settlement

The process by which an FX trade is completed — the actual exchange of currencies between parties. Spot FX trades typically settle on T+2 (two business days after the trade date). Forwards settle on the agreed future date. NDF settlement involves only the net cash differential, not physical currency exchange.

▼

Settlement is the final step in an FX transaction — when the contractual exchange of currencies (or, for NDFs, the cash differential) actually occurs. Settlement conventions vary by currency pair: most major pairs settle on T+2 (trade date plus two business days), though some (USD/CAD) settle T+1. EM currencies may have extended settlement cycles due to local market hours and clearing infrastructure.

Settlement risk (also called Herstatt risk, after the 1974 bank failure) is the risk that one party delivers currency but the counterparty fails before making its reciprocal payment. This risk is mitigated by CLS (Continuous Linked Settlement), which settles matching payments simultaneously for major currency pairs.

For NDF settlement, the fixing date (when the reference rate is determined) typically precedes the settlement date by 2 business days, following the same T+2 convention.

Spot Rate

The current exchange rate at which two currencies can be exchanged for immediate delivery (technically T+2 settlement). The spot rate is the starting point for all FX pricing — forward rates are derived from the spot rate adjusted for interest rate differentials.

▼

The spot rate is the price at which one currency can be exchanged for another today, with delivery (settlement) in two business days. It is the most widely quoted exchange rate and the reference point from which all forward rates, option strikes, and derivative prices are calculated.

In the context of FX risk management, the spot rate is important because: (1) it determines the starting price from which forward rates are calculated; (2) it is the rate used to value (mark-to-market) outstanding forward and option positions; (3) it is the reference used to calculate the gain or loss on an NDF at fixing; and (4) it determines the immediate P&L impact of unhedged FX transactions.

Budget rates, hedge effectiveness, and financial statement translation all reference the spot rate at relevant measurement dates — making spot rate movements the primary driver of reported FX gain or loss for most organisations.

Structured FX Solution

A tailored combination of FX instruments designed to address a complex, multi-layered, or otherwise non-standard currency exposure. Structured solutions combine forwards, options, swaps, and bespoke features to balance cost, protection level, participation rate, and cash flow timing.

▼

Structured solutions are used when a standard forward, option, or collar does not adequately address the specific characteristics of the exposure. They are particularly appropriate for: multi-currency portfolios with correlated exposures, complex cash flow profiles (e.g., ramp-up infrastructure projects), exposures with conditional outcomes (e.g., pending M&A transactions), and situations where carry cost minimisation is a primary objective.

Deaglo's Strategy Optimizer uses machine learning to evaluate structured solutions across up to nine parameters simultaneously — finding the combination of instrument, strike, tenor, notional, and participation rate that delivers the best risk-return outcome for the client's specific constraints. This replaces the traditional approach of evaluating two to three manually-constructed structures.

Deaglo Relevance

The Deaglo Strategy Optimizer is purpose-built for structured solutions — using machine learning to search and optimise across the full parameter space of hedging structures, delivering strategies that balance cost, protection, and participation in ways that manual analysis cannot achieve.

T

Tenor

The time period from the trade date to the maturity or expiry date of an FX derivative contract. Tenor determines the duration of a hedge and is a key driver of forward points (and therefore hedging cost), liquidity, and counterparty credit exposure.

▼

Tenor refers to the length of a derivative contract — typically expressed as weeks, months, or years (1M, 3M, 1Y, 5Y). Standard tenors in FX include: overnight, 1 week, 1 month, 2 months, 3 months, 6 months, 1 year, 2 years, and 5 years. Non-standard tenors (broken dates) are quoted to match specific future cash flow dates.

The choice of tenor is a critical strategic decision: longer tenors provide certainty over a longer horizon but accumulate more carry cost and create larger MTM positions that are more sensitive to rate changes. Shorter tenors reduce carry cost and MTM sensitivity but require more frequent execution and expose the entity to re-hedging risk at each rollover.

For EM currencies with significant interest rate differentials, tenor optimisation — balancing carry cost against coverage horizon — is a primary advisory function. Deaglo's Strategy Simulator models different tenor ladders to find the optimal coverage structure.

Transaction Cost Analysis (TCA)

The measurement and benchmarking of the costs incurred in executing FX transactions — primarily the bid-offer spread paid versus the mid-market rate. TCA answers whether a specific FX transaction was executed at a cost-efficient rate relative to what was available in the market.

▼

TCA in FX measures the execution quality of individual transactions: how far the executed rate was from the mid-market rate at the time of execution, what the spread cost amounted to, and how it compares to the market standard for that currency pair, volume, and time of day. It answers: "did you get a good price?"

TCA is fundamentally different from the FX Diagnostic. TCA evaluates transaction execution quality — a backward-looking, transactional analysis. The FX Diagnostic evaluates whether the overall FX risk management program is aligned to the actual exposure, cost-effective, and properly structured — a forward-looking, strategic analysis. A company could have excellent TCA scores (good execution on individual transactions) while still having a deeply misaligned hedge program.

Both are valuable, but TCA alone provides no insight into whether the hedging strategy is right — only whether individual trades were executed efficiently.

Deaglo Relevance

Deaglo's FX Diagnostic includes execution cost benchmarking (a form of TCA) as one component — but the diagnostic goes further, examining whether the hedge strategy itself is appropriate. TCA = did you get a good price? FX Diagnostic = did you manage the risk properly?

Transaction Risk

The risk that exchange rate changes will affect the value of specific, known future cash flows in a foreign currency — such as a scheduled debt repayment, confirmed export receivable, or committed import payment. It is the most direct and common form of FX risk faced by corporates.

▼

Transaction risk exists the moment a company enters into a contract (or creates a commitment) denominated in a foreign currency. From that point until the cash is actually exchanged, any movement in the exchange rate affects the amount that will be received or paid in the home currency. If the rate moves adversely, the company will receive less (or pay more) than anticipated.

Transaction risk is the most straightforward type of FX risk to hedge because both the amount and the timing are known or can be estimated reliably. FX forwards are the primary instrument — locking in a rate for the specific amount and date of the underlying cash flow.

Transaction risk is distinct from translation risk (which affects financial statement values without affecting cash flows) and economic risk (which affects the business's competitive position over time).

Translation Risk (Accounting Risk)