Your Portfolio Returns Have a Currency Problem (And How to Fix It)

A Quick Guide to Managing FX Risk in Investment Portfolios

For funds investing across borders, currency risk is not a secondary factor — it is embedded in portfolio performance.

Every foreign investment introduces two layers of return:

- the underlying asset performance

- the currency movement

Yet in many portfolios, FX exposure is treated as background noise , until volatility turns it into a visible drag on returns, investor reporting, and decision-making.

.png)

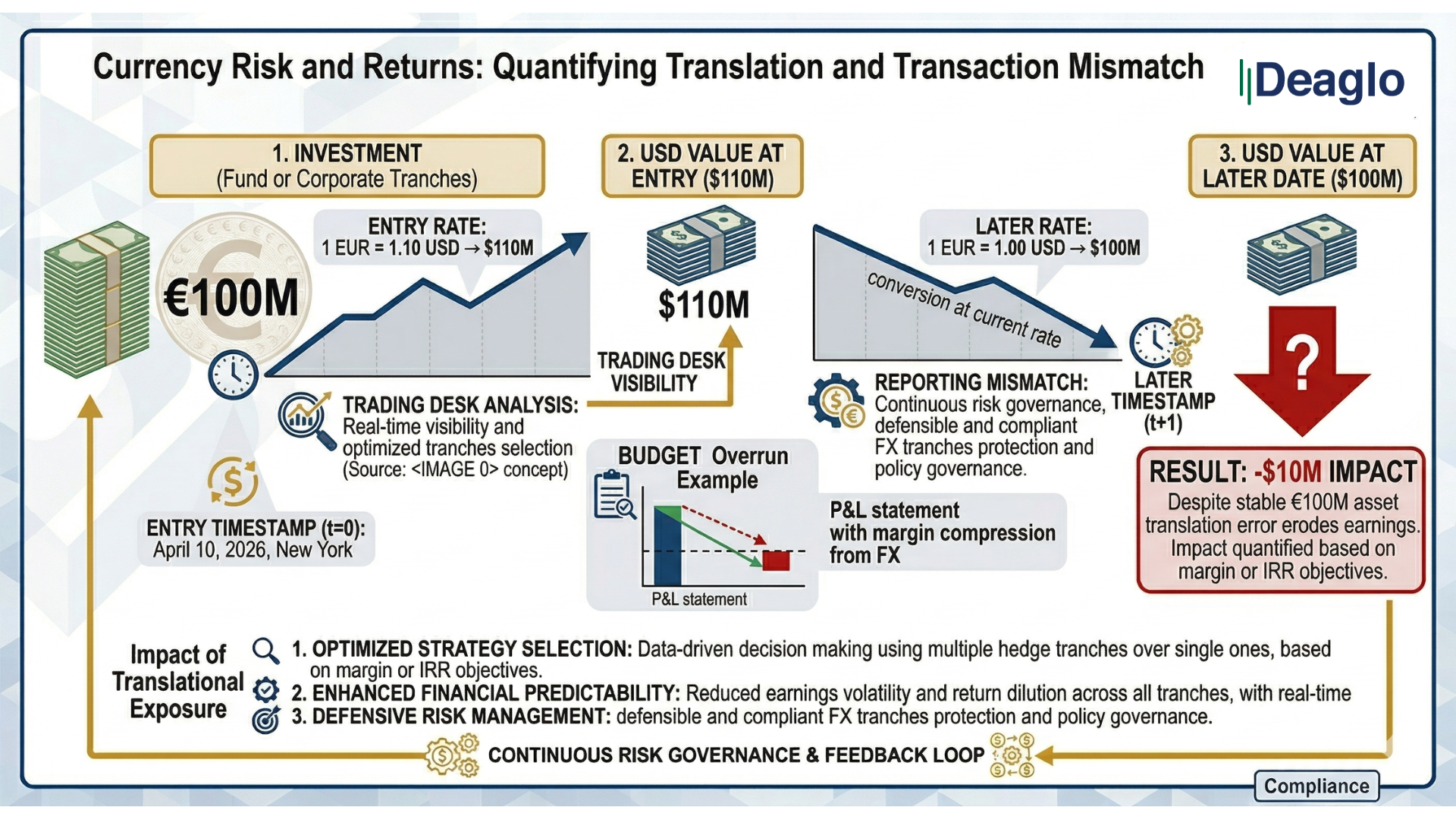

What Is Currency Risk in Investment Portfolios?

Currency risk (foreign exchange risk) is the impact of exchange rate movements on the value of investments denominated in foreign currencies. A portfolio company may perform well in local terms, but if the currency weakens against the fund’s base currency, reported returns decline when converted.

Key takeaway: Portfolio performance is not the same as realized returns after FX conversion.

Why FX Risk Becomes a Problem for Funds

FX risk becomes most visible when funds need to explain performance with clarity and confidence.

- It distorts reported returns - Currency movements can amplify or reduce returns independently of asset performance.

- It weakens LP communication - Investors expect clear attribution of what is driving performance — including FX.

- It complicates capital raising - Unhedged exposure introduces variability into track records.

- It creates missed opportunities - Favorable exchange rates are often not locked in at key investment moments.

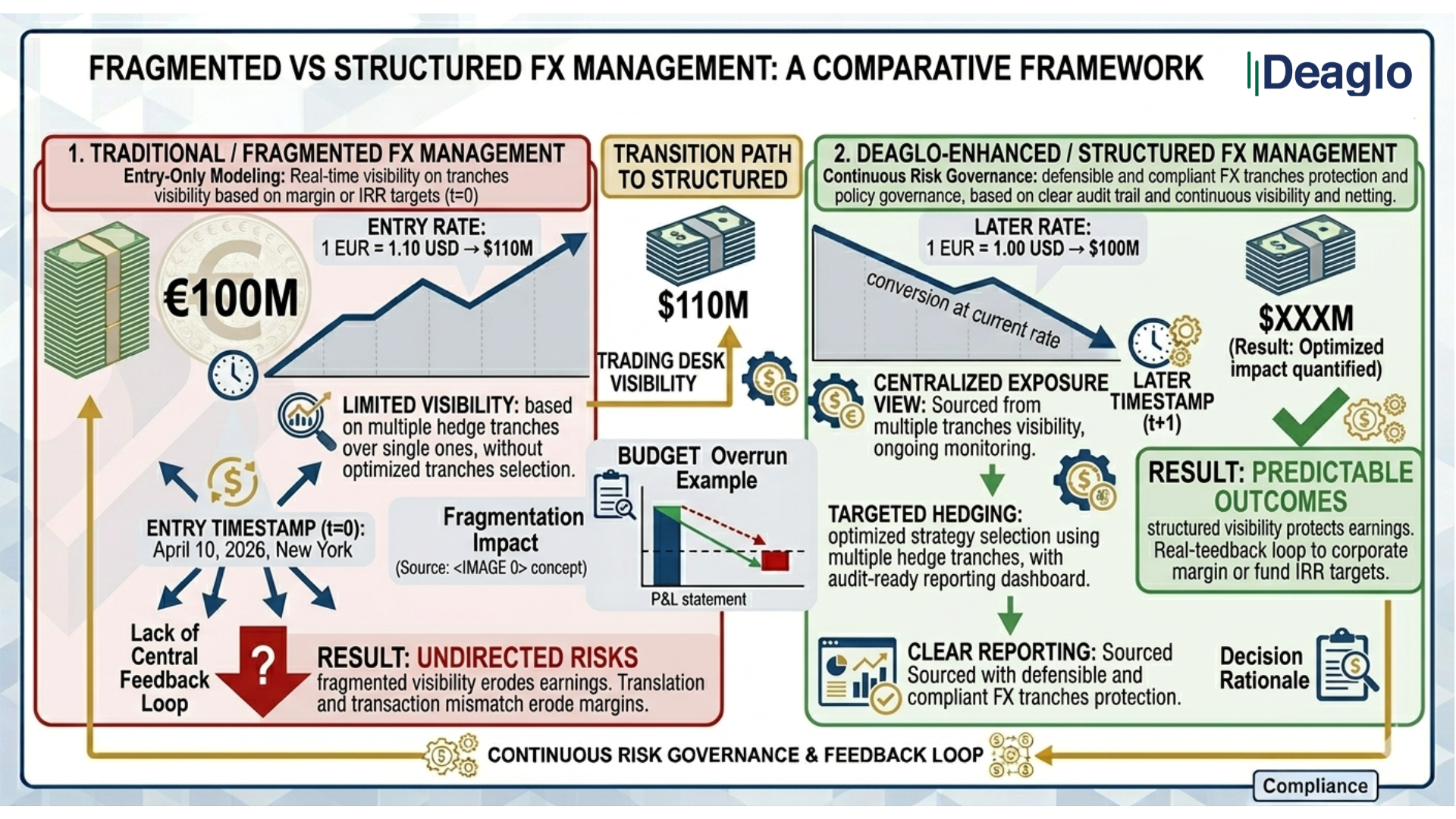

Where Most Funds Fall Short

Across private equity, venture capital, and private credit, the pattern is consistent:

- FX exposure is modeled at entry but not actively managed during hold

- hedging is reactive instead of strategy-driven

- reporting lacks transparency on currency impact

- portfolio-level exposure is not centralized

The challenge is not awareness, it is execution.

How to Manage Currency Risk in a Portfolio

A structured approach to FX risk management transforms currency from a source of uncertainty into a controllable variable.

1. Centralized Exposure Visibility

Track FX exposure across all investments, currencies, and entities in one place.

2. Scenario Analysis

Model how currency movements impact:

- IRR

- cash flows

- exit outcomes

3. Targeted Hedging Strategies

Use tools such as:

- forward contracts

- currency options

- natural hedging

4. Transparent Reporting

Provide LPs with:

- FX attribution

- hedged vs unhedged views

- forward-looking exposure insights

Goal: Make FX measurable, explainable, and controlled.

.png)

From Passive Exposure to Active Management

Leading funds are shifting from:

- reactive → proactive

- fragmented → centralized

- unclear → transparent

Currency risk is no longer treated as an afterthought. It is becoming a core component of portfolio strategy and investor communication.

Final Thought

Currency risk is not just a market variable — it is a portfolio variable.

Funds that actively manage FX exposure gain:

- more stable returns

- clearer LP communication

- stronger control over performance outcomes

See how funds are quantifying and managing FX exposure.