The Mean Reversion Fallacy in FX Risk Management

Understanding Why "Wait and See" Destroys Corporate and Fund Returns

What Is Mean Reversion — and Why It Tempts FX Risk Managers?

Mean reversion is the financial principle that an asset's price will, over time, tend to converge back toward its long-run historical average. Inequity markets, where the same asset class is actively traded, this concept under pins dozens of well-known technical indicators, from MACD (Moving Average Convergence Divergence) to the Percentage Price Oscillator (PPO).

For CFOs, treasury managers, and fund managers grappling with fluctuating foreign exchange exposures, the appeal of mean reversion as an FX strategy is understandable: if the exchange rate will eventually return to its average, why incur the cost and complexity of derivative-based hedging? Simply absorb the volatility and "wait it out."

This article demonstrates why that logic is fundamentally flawed and potentially catastrophic for corporates and funds managing real FX risk.

.png)

KEY INSIGHT

Mean reversion as an FX strategy requires two conditions that almost never hold in practice: (1) no persistent trend in the currency pair, and (2) reversion within a timeframe aligned with your business cycle. Neither condition is reliably met in major or emerging market FX pairs.

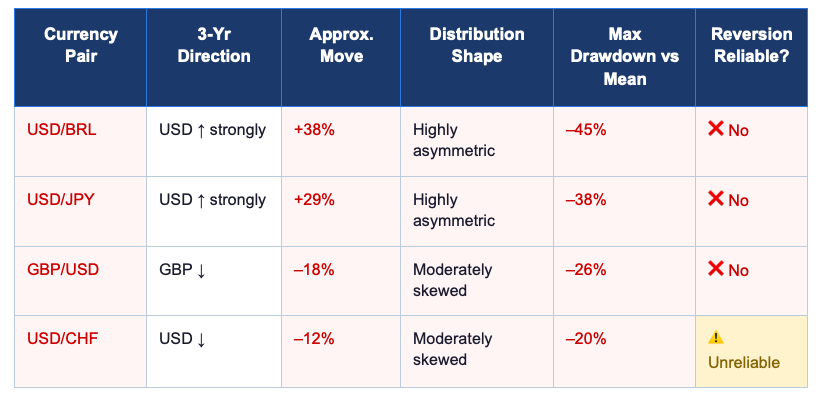

2. The Mathematical Reality: Trends Invalidate Mean Reversion

For mean reversion to function as a viable strategy, the underlying time series must exhibit approximate symmetry around the mean, returns should be distributed relatively evenly above and below the long-run average. This is the theoretical bedrock of reversion-based indicators.

The critical complication is trend. When a time series exhibits a persistent directional trend, the distribution of returns becomes asymmetric, and mean reversion signals become unreliable or misleading.

Why FX Pairs Are Structurally Trending

Foreign exchange markets are driven by macro fundamentals interest rate differentials, inflation divergence, geopolitical risk, capital flows, and central bank policy. These forces are slow-moving, persistent, and generate multi-year trends in currency pairs. Unlike individual equities that trade around a business's intrinsic value, currencies have no fundamental anchor that enforces reversion.

3. The Corporate and Fund Reality: You Cannot Time FX Exposure

Technical traders using mean reversion indicators have one crucial advantage that corporate treasury teams and fund managers do not: discretion over when to take and exit positions. A hedge fund running an FX carry strategy can wait six, twelve, or eighteen months for a reversion signal to materialise.

Corporates and funds generating FX-denominated revenues, dividends, or capital flows do not have this luxury. Their exposures arise on fixed schedules, monthly revenue receipts, quarterly dividend repatriations, semi-annual debt service, capital deployment into overseas assets, entirely independent of where the spot rate sits relative to its historical mean.

The Accountability Gap

No CFO can stand before their board and explain a 20% currency-driven earnings miss with: "We were waiting for mean reversion." No fund manager can defend a 15% NAV decline driven by unhedged FX exposure to theirLPs with a theoretical argument about long-run averages.

The asymmetry of consequences is absolute: the upside of avoiding hedging costs is measured in basis points; the downside of an unhedged trending move is measured in percentage points of earnings, NAV, or capital.

4. When Does Mean Reversion Actually Work in FX?

It is worth acknowledging the narrow conditions under which mean reversion concepts retain some validity in FX markets, to avoid overstating the case.

Mean reversion may generate modest, intermittent signals when all of the following hold simultaneously:

1. The currency pair is genuinely ranging (no macroeconomic divergence driving a trend).

2. The measurement period is short , weeks to a few months, not years.

3. The entity has full discretion over timing of the FX transaction.

4. The entity can absorb the full mark-to-market loss if the trend extends.

None of these conditions apply to a corporate treasury team or institutional fund manager with scheduled, obligation-driven FX flows.

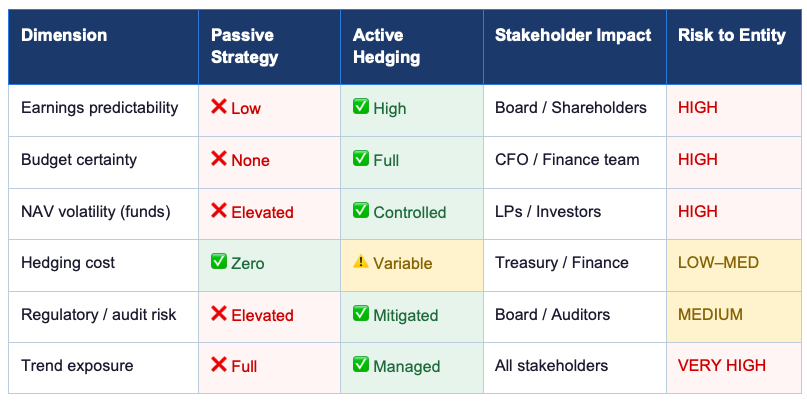

5. Active FX Risk Management: The Only Viable Framework

For corporates and funds, active FX risk management through derivatives is not merely a best practice, it is a fiduciary obligation. The question is not whether to hedge, but how to optimize the hedge to maximize protection while minimizing cost.

.png)

6. Reducing Hedging Costs Without Reducing Protection

A common objection to active FX hedging among corporates and fund managers is cost. Derivative-based hedging does carry a cost, but that cost is manageable, and in many cases can be reduced substantially or even eliminated through intelligent structuring.

Conclusion: Wishful Thinking Has No Place in FX Risk Management

Mean reversion is an intellectually appealing concept that fails inpractice for corporates and funds managing real currency exposure. FX markets are structurally driven by persistent macro forces that generate multi-yeart rends. Firms and funds cannot time their exposures. And the consequences of a trending unhedged move earnings volatility, NAV erosion, covenant breach,investor confidence loss, are categorically more severe than the cost of any derivative-based hedging programme.

Active FX risk management, executed intelligently through acombination of forwards, options, and structured products, is not a luxury, it is a risk management imperative. The cost of hedging is known, bounded, andoptimisable. The cost of not hedging is open-ended.

About Deaglo

Deaglo provides institutional-grade FX risk management solutions forcorporates and funds. Our strategy simulator generates graphical displays ofthe efficacy of multiple hedging strategies, making selection straightforwardand intuitive. Our team helps clients lower hedging costs potentially to zero, by optimizing hedge structures, tenors, and credit lines.

→ Ready to manage your FX risk actively? Contact Deaglo to run a no-cost strategy simulation.