Interest Rate Risk Management for Funds: Frameworks and Strategies for Leveraged Portfolios

.png)

What Is Interest Rate Risk Management for Funds?

Interest rate risk management for funds is the process of identifying, measuring, and controlling how changes in benchmark interest rates affect borrowing costs, cashflows, asset valuations, and investment returns. It helps investment funds manage rate-sensitive leverage, stabilize interest expense, protect liquidity, and align financing structures with portfolio risk objectives.

Why Interest Rate Risk Matters for Investment Funds

Interest rates have a direct and material impact on fund performance and portfolio financing structures. For funds using leverage such as private equity, private credit, real estate, and infrastructure funds changes in benchmark rates can influence borrowing costs, covenant headroom, distributable cashflows, and asset valuations.

This article explains how funds manage interest rate risk, outlines common interest rate risk management strategies for investment funds, and highlights how structured analysis and technology support disciplined decision-making across portfolios and financing structures.

What Is Interest Rate Risk for Funds?

Interest rate risk for investment funds refers to the potential financial impact caused by changes in benchmark interest rates on fund-level and asset-level financing structures. For leveraged portfolios, movements in interest rates can affect borrowing costs, cashflows, valuations, and overall investment returns.

Interest rate risk most commonly arises from:

- Floating-rate financing linked to benchmarks such as SOFR or EURIBOR

- Refinancing exposure during recapitalization, refinancing, or exit events

- Mismatch between asset duration and liability duration, where long-term assets are funded with shorter-term or floating-rate debt

Unlike corporates, investment funds must manage interest rate risk across multiple portfolio companies, financing structures, and investment timelines, often under strict return targets and liquidity constraints.

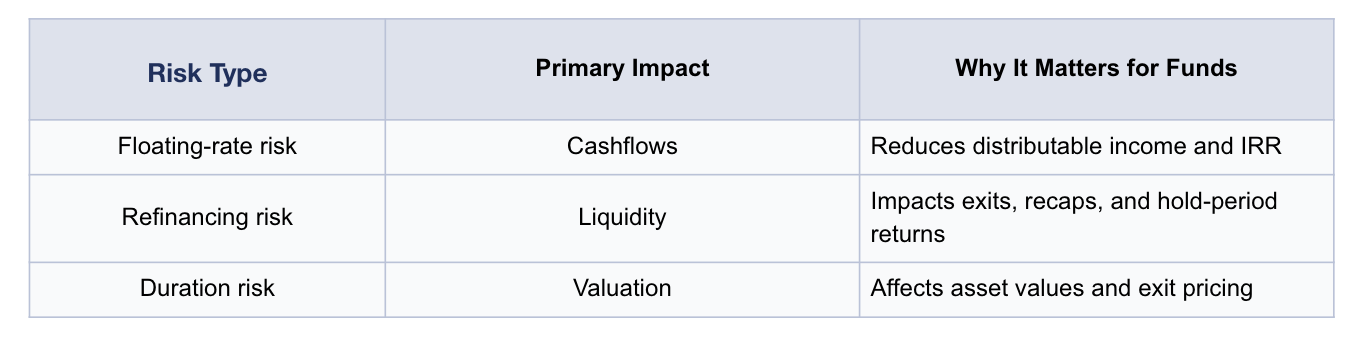

Types of Interest Rate Risk in Fund Structures

Investment funds typically face several forms of interest rate risk depending on how portfolio assets are financed and how debt structures evolve over the investment lifecycle. Understanding these risk categories helps funds implement more structured interest rate risk management frameworks across leveraged portfolios.

Floating-Rate Exposure

Many fund financing structures are linked to floating benchmark rates such as SOFR or EURIBOR. When benchmark rates increase, interest expense rises, which can reduce distributable cashflows and investment returns.

Refinancing and Exit Risk

Debt maturing during a fund’s hold period or near an exit event may need to be refinanced under different market conditions. If interest rates rise before refinancing occurs, borrowing costs may increase, potentially impacting equity returns, exit valuations, and recapitalization strategies.

Duration and Valuation Risk

When long-duration assets are financed with shorter-term or floating-rate debt, changes in interest rates can create mismatches between asset values and financing costs. These movements may influence portfolio valuations, refinancing decisions, and exit multiples.

Which Funds Are Most Exposed to Interest Rate Risk?

Interest rate risk management for funds is particularly important for strategies that rely on leverage or hold assets with rate-sensitive financing structures. Changes in benchmark interest rates can directly affect borrowing costs, distributable cashflows, and portfolio valuations.

Funds most exposed to interest rate risk include:

- Private equity funds using acquisition leverage to finance portfolio companies

- Private credit funds with rate-sensitive assets and liabilities tied to floating benchmarks

- Real estate funds relying on floating-rate mortgages or construction financing

- Infrastructure funds holding long-dated assets with refinancing exposure

Even funds with partially fixed-rate debt may still face interest rate risk through refinancing timelines, incremental borrowing, or portfolio expansion, making structured interest rate risk management frameworks essential for leveraged portfolios.

How Interest Rate Risk Impacts Fund Performance

Interest rate risk can significantly affect the financial performance of leveraged investment funds by influencing borrowing costs, cashflows, and asset valuations. When interest rates rise or fluctuate unexpectedly, the impact can extend across both portfolio companies and fund-level financing structures.

Unmanaged interest rate risk can lead to:

- Higher and more volatile interest expense on floating-rate debt

- Reduced cashflow available for distributions to investors

- Pressure on leverage ratios and covenant compliance

- Changes in asset valuations and exit outcomes

For leveraged fund strategies, these effects can compound quickly. Rising borrowing costs and reduced distributable cashflows can materially influence IRR, equity multiples, and overall portfolio performance.

How Funds Measure Interest Rate Risk

Investment funds measure interest rate risk using standardized financial metrics that translate movements in benchmark interest rates into measurable impacts on cashflows, borrowing costs, and asset valuations. These metrics allow fund managers to evaluate exposure consistently across portfolio companies, financing structures, and investment timelines.

Common metrics used in interest rate risk management for funds include:

- Interest expense sensitivity, measuring how borrowing costs change when benchmark rates move

- Duration, assessing the sensitivity of asset or liability values to changes in interest rates

- DV01 (Dollar Value of a Basis Point), estimating the financial impact of a one-basis-point change in rates

- Cashflow-at-Risk (CFaR), quantifying potential downside volatility in future cashflows

- Scenario and stress testing, evaluating performance across different interest rate environments

Together, these metrics help funds quantify rate exposure, compare outcomes across different portfolio structures, and support more disciplined interest rate risk management decisions.

.png)

Interest Rate Risk Management Strategies for Funds

Investment funds apply a combination of hedging and structural approaches to manage exposure to changing benchmark interest rates. Effective interest rate risk management strategies for funds aim to stabilize borrowing costs, reduce cashflow volatility, and protect portfolio performance across different rate environments.

Common strategies used by funds include:

- Fixing a portion of floating-rate exposure to reduce sensitivity to rising benchmark rates

- Staggering hedge maturities so that hedges align with asset hold periods and refinancing timelines

- Applying interest rate hedging selectively at the asset level, depending on leverage structure and risk profile

- Balancing partial and full hedging across the portfolio to manage both protection and flexibility

The appropriate strategy depends on factors such as the fund mandate, investment horizon, leverage structure, and prevailing market conditions. Structured frameworks help ensure that hedging decisions remain aligned with portfolio risk objectives and liquidity constraints.

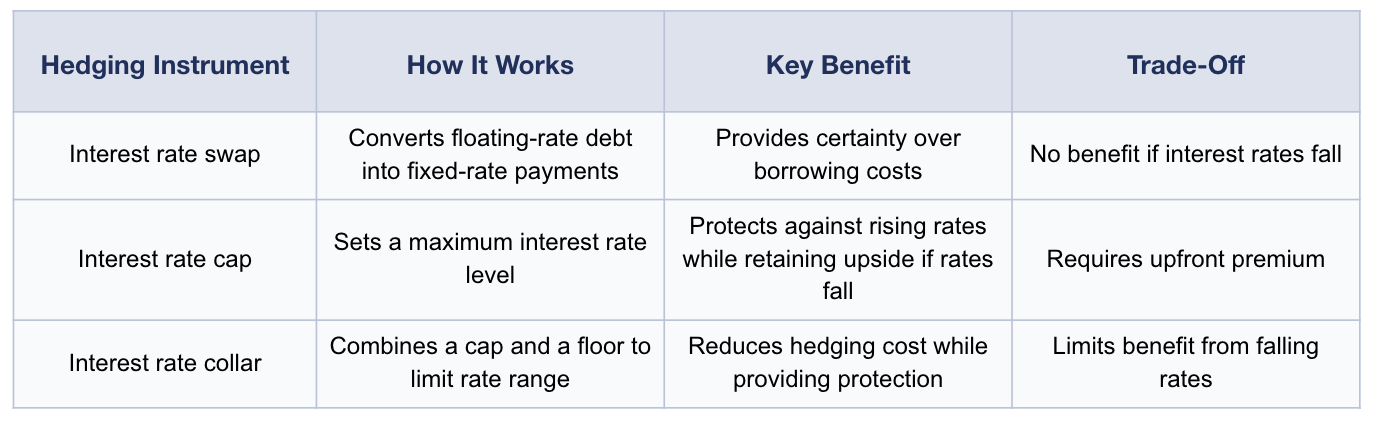

Interest Rate Hedging for Funds

Investment funds commonly use interest rate hedging instruments to manage exposure to rising benchmark rates and stabilize borrowing costs. The most widely used tools include interest rate swaps, caps, and collars, each offering different trade-offs between protection, flexibility, and cost.

Partial vs Full Hedging at the Fund Level

When implementing interest rate hedging strategies, funds often choose between partial hedging and full hedging depending on their exposure profile, liquidity constraints, and investment horizon. The appropriate approach depends on how much interest rate volatility the fund is willing to tolerate.

Partial hedging may be preferred when:

- The interest rate outlook is uncertain and flexibility is required

- Liquidity constraints limit the ability to fully hedge exposure

- Portfolio companies may refinance or exit during the hold period

Full hedging may be appropriate when:

- Predictable cashflows are critical for portfolio stability

- Leverage levels or covenant risk require stable borrowing costs

- Assets have long and relatively stable hold periods

Choosing between partial and full hedging is a key decision within interest rate risk management for funds, helping investment teams balance protection, flexibility, and cost across the portfolio.

The Role of Technology in Fund Interest Rate Risk Management: Visibility, Consistency, and Governance

Modern interest rate risk management for funds increasingly relies on technology to manage complex financing structures across multiple portfolio companies and jurisdictions. As portfolios scale, manual processes and spreadsheets often make it difficult to maintain consistent analysis and governance.

Interest rate risk management software for funds helps investment teams:

- Maintain centralized visibility of interest rate exposure across portfolio companies and financing facilities

- Perform consistent scenario analysis and stress testing across different rate environments

- Compare hedged versus unhedged outcomes to evaluate potential financial impact

- Support documentation and governance requirements for investment committees, LP reporting, and audits

Solutions designed specifically for funds—such as Deaglo’s interest rate risk management solutions, help centralize exposure data, analyze financing sensitivity to interest rate changes, and evaluate potential hedging strategies across portfolios. By combining structured analytics with governance frameworks, funds can manage interest rate exposure more consistently across assets, financing structures, and investment timelines.

Managing Interest Rate Risk with Structure and Discipline

Effective interest rate risk management for funds is essential for maintaining stable borrowing costs, protecting liquidity, and supporting consistent portfolio performance. As leveraged fund strategies depend heavily on financing structures, changes in benchmark interest rates can directly influence cashflows, covenant headroom, valuations, and ultimately IRR outcomes.

A disciplined approach to interest rate risk management involves identifying exposure across portfolio companies, measuring financial sensitivity using standardized metrics, and implementing structured strategies aligned with the fund’s investment horizon and risk appetite. Combining interest rate hedging strategies, portfolio-level analysis, and strong governance frameworks allows funds to manage interest rate exposure more consistently across assets and financing structures.

Technology-driven solutions can further strengthen this process by providing centralized visibility, scenario analysis, and structured reporting across portfolios. Deaglo’s solutions for funds help investment teams analyze interest rate exposure, evaluate hedging strategies, and quantify the potential financial impact of changing rate environments, supporting more informed and disciplined decision-making across leveraged portfolios.

By combining structured frameworks, analytics, and governance, funds can manage interest rate risk more effectively and improve resilience across changing market conditions.