Despite the recent outburst of the Coronavirus, which has kept investor confidence low since early June, global markets closed out July with an uplift in sentiment, underpinned by strong earnings reports. This was led by the technology sector and an accommodative Federal Reserve opened to considering tapering its bond purchase program in the upcoming meetings, all while assuring that the stimulus will be sustained in the short term. Equity markets extended new all-time highs amid profit bonanza, with Nasdaq reaching 14,863 and S&P 4,422 respectively. Commodities linked companies followed the same trend, suggesting that sustained commodity prices are backed by households returning to spend their money outside their homes and a sustained recovery from China.

Equity Market Performance - S&P & Nasdaq

Source: Bloomberg

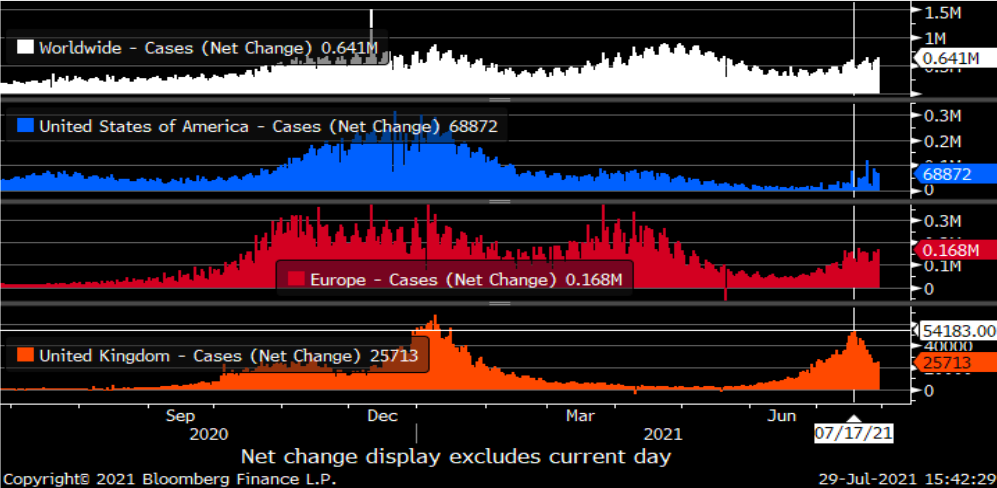

Governments continued to bet on high inoculation ratios as the best way to combat the resurgence of the Delta variant, picking up the pace of their vaccination programmes where possible, in order to avoid putting in place restrictions once again. Unfortunately, the spike in coronavirus cases has activated many red flags globally. Among them are delays in the U.K. reopening, a declaration of a state of emergency in different cities in Japan, and establishing centralized lockdowns in Australia, which are just some examples of how it has affected several markets. As rising Covid cases continued to deteriorate the market mood, economists revised down their growth expectations in economies severely affected by the latest wave of Covid, while jitters of a Chinese economic slowdown kept markets on suspense and commodity prices shaky, especially after the OPEC + fallout. The West Texas Intermediate (WTI) plummeted 7%, but recovered shortly after output quotas were agreed, edging the price above USD 70 amid improving conditions globally and resilience in the Chinese economy to sustain its demand.

COVID CASES Net Change

Source: Bloomberg

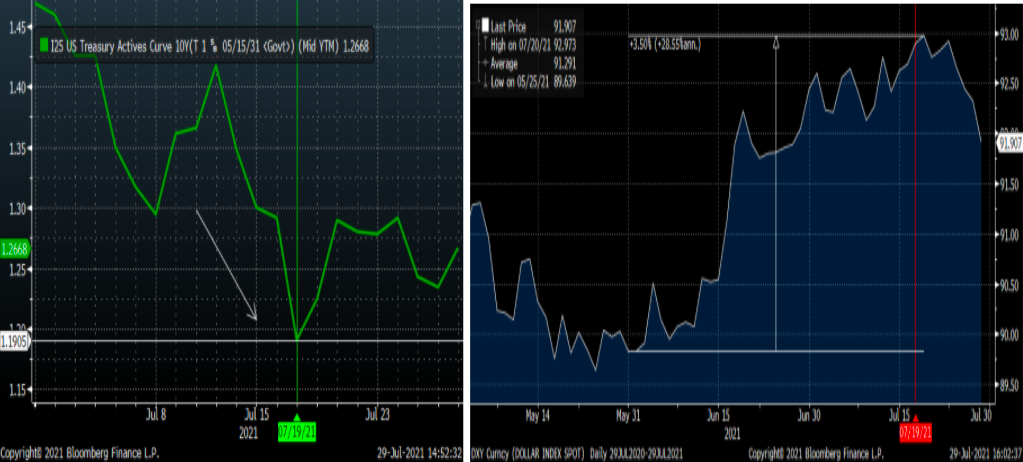

Amid the rising infection rates since the beginning of June, the greenback appreciated against most of its peers as investors sought refuge among U.S. treasuries, pushing yields to 1.1905% during the risk off run. The U.S. dollar index, a coefficient used to benchmark the performance of the greenback against a basket of six major currencies, rallied 3.50% since the beginning of June, as investors de-risked their portfolios while Covid cases continued to rise in Europe and the United Kingdom (U.K.). However, the British government reported in mid June a record high of over 54k daily cases, from which infections started to ease and market confidence began to restore. The U.K. is looking to close out July reporting 50% reduction from the peak, assisted by the end of the Euros and higher inoculation ratios reaching up to 88.3% of the adult population with at least one jab and 71.1% with two jabs. The Covid situation in continental Europe followed a similar path stabilizing at 168k daily cases easing down pressures on lockdowns and increasing the likelihood of sustaining the economic recovery.

Additionally, the Federal Open Market Committee decided to maintain its cautious tone amid COVID-19 pressures, leaving interest rates unchanged and hinting at tapering bond purchases without providing any details on timing. Remarks from Jerome Powell were very much in line with market expectations controlling the impact over financials and stimulating confidence for investors to shift their risk stance. However, policymakers continue to classify the persisting inflation levels as transitory, and stated that substantial further progress in the labour market still needs to be made before they can consider adjusting interest rates. The dovish comments from Fed officials and stabilizing covid cases have helped market participants to improve their risk positioning amid greater confidence, making the greenback retrace 1.13% from July highs in the last week of the month and looking to extend losses amid rising optimism.

10-Year U.S. Treasury Yields & U.S. Dollar index

Source: Bloomberg

Despite improving conditions and solid earning reports, the U.S. growth missed forecasts in the second quarter as the effects of supply chain bottlenecks denied the economy to take advantage of bolstering consumer spending. Gross Domestic product figures released 6.5% annualized, below 8.4% previously anticipated while previous figures were revised down 0.1% to 6.3% in Q1. The latest growth report underscores the challenges that companies are facing in trying to keep up the pace with that demand. These bottleneck effects continue to weigh on the economy’s ability to speed up the recovery rate and allowance of letting inflation sustain its high levels. Personal consumption expenditures exceeded expectations, enabling inflationary pressures to remain on the upside amid consumers ramping up their spending on services such as dining out and traveling.

As the global outlook starts improving, risk appetite from market participants will restore accordingly, with several flows seeking for riskier assets and aiming for exposures in economies with strong potential of recovery in the medium term. However, risks are still imminent as Covid woes have shown its capability in souring the market mood and triggering further lockdowns and restrictions. However, the economy has proven to be resilient with the latest spike in Coronavirus cases, which give notes of optimism ahead of the post pandemic boom.

June’s Economic Calendar

USD

On Monday (08/02): Markit Manufacturing PMI ¦ ISM Manufacturing Employment Index ¦ ISM Manufacturing PMI ¦ ISM Manufacturing Prices Paid ¦ Construction Spending

On Tuesday (08/03): Factory Orders ¦ Fed’s Bowman Speech

On Wednesday (08/04): ADP Employment Change ¦ Markit Services PMI ¦ Markit PMI Composite

On Thursday (08/05): Goods and Services Trade Balance ¦ Initial Jobless Claims ¦ Fed’s Waller speech

On Friday (08/06): Nonfarm Payrolls ¦ Average Hourly Earning ¦ Labor Force Participation Rate ¦ Unemployment Rate

On Tuesday(08/10): Nonfarm Productivity ¦ Unit Labor Costs

On Wednesday (08/11): Monthly Budget Statement

On Thursday (08/12): Consumer Price Index Core ¦ Producer Price index ex Food & Energy ¦ Consumer Price index n.s.a

On Friday (08/13): Michigan Consumer Sentiment Index

On Tuesday (08/17): Retail Sales ex Autos ¦ Retail Sales Control Group ¦ Retail Sales

On Wednesday (08/18): Building Permits ¦ Housing Starts ¦ FOMC Minutes

On Thursday (08/19): Philadelphia Fed Manufacturing Survey ¦ Initial Jobless Claims

On Monday (08/23): Chicago Fed National Activity Index ¦ Markit Manufacturing PMI (PREL) ¦ Markit Services PMI (PREL) ¦ Markit PMI Composite

On Tuesday (08/24): New Home Sales

On Thursday (08/26): Durable Goods Orders ex Transportation ¦ Core Personal Consumption Expenditures ¦ Durable Goods Orders ex Defense ¦ Personal Consumption Expenditures Prices ¦ Durable Goods Orders ¦ Initial Jobless Claims ¦ Nondefense Capital Goods Orders ex Aircraft

On Friday (08/27): Core Personal Consumption Expenditures - Price Index ¦ Personal Income ¦ Personal Spending ¦ Michigan Consumer Sentiment Index

On Monday (08/30): Gross Domestic Product (PREL) Q2 ¦ Pending Home Sales

On Tuesday (08/31): Housing Price Index ¦ Chicago Purchasing Managers’ ¦ Consumer Confidence

EUR

On Monday (08/02): Markit Manufacturing PMI

On Tuesday (08/03): Producer Price Index

On Wednesday (08/04): Markit Services PMI ¦ Markit PMI Composite ¦ Retail Sales

On Thursday (08/05): Economic Bulletin

On Monday (08/09): Sentix Investor Confidence

On Tuesday (08/10): ZEW Survey - Economic Sentiment

On Thursday (08/12): Industrial Production

On Friday (08/13): Trade Balance

On Saturday (08/14): Gross Domestic Product (PREL)

On Monday (08/16): Eurogroup meeting

On Tuesday (08/17): Ecofin Meeting ¦ Employment Change (PREL) ¦ Gross Domestic Product (PREL)

On Wednesday (08/18): Consumer Price Index

On Thursday (08.19): Current Account ¦ Economic Bulletin

On Monday (08/23): Markit Manufacturing PMI (PREL) ¦ Markit Services PMI (PREL) ¦ Markit PMI Composite (PREL) ¦ Consumer Confidence (PREL)

On Monday (08/30): Services Sentiment ¦ Consumer Confidence ¦ Industrial Confidence ¦ Business Climate ¦ Economic Sentiment Indicator

On Tuesday (08/31): Consumer Price index ¦ Consumer Price Index Core

GBP

On Monday (08/02): Markit Manufacturing PMI

On Wednesday (08/04): Markit Services PMI

On Thursday (08/05): Markit Construction PMI ¦ Bank of England Monetary Policy Report ¦ BoE MPC Vote ¦ BoE Asset Purchase Facility ¦ Monetary Policy Summary ¦ Bank of England Minutes ¦ BoE’s Governor Bailey Speech

On Friday (08/06): Halifax house Prices

On Monday (08/09): BRC Like-for-like Retail Sales

On Wednesday (08/11): NIESR GDP Estimate

On Thursday (08/12): Manufacturing Production ¦ Industrial Production ¦ Gross Domestic Product (PREL)

On Tuesday (08/17): Claimant Count Change ¦ ILO Unemployment Rate ¦Average Earnings Excluding Bonus

On Wednesday (08/18): Consumer Price Index ¦ Retail Price Index ¦ PPI Core Output ¦ Producer Price Index

On Thursday (08/19): GfK Consumer Confidence

On Friday (08/20): Retail Sales

On Monday (08/23): Markit Manufacturing PMI ¦ Markit Services PMI

JPY

On Monday (08/02): Tokyo Consumer Price Index ¦ Consumer Confidence

On Wednesday (08/04): Jibun Bank Services PMI ¦ Foreign Investment in Japan Stocks ¦ Foreign Bond Investment

On Thursday (08/05): Overall Household Spending

On Friday (08/06): Leading Economic Index

On Thursday (08/12): Producer Price Index ¦ Gross Domestic Product (PREL)

On Monday (08/16): Industrial Production ¦ Capacity Utilization ¦ Industrial Production

On Tuesday (08/17): Merchandise Trade Balance ¦ Imports ¦ Exports

On thursday (08/19): National Consumer Price Index

On Wednesday (08/25): Leading Economic Index

On Thursday (08/26): Tokyo Consumer Price Index

On Monday (08/30): Jobs / Application Ratio ¦ Unemployment Rate ¦ Retail Trade ¦ Industrial Production ¦ Larger Retail Sales

On Tuesday (08/31): Housing Starts ¦ Construction Orders ¦ Consumer Confidence Index

CAD

On Monday (08/02): August Civic Holiday

On Tuesday (08/03): Markit Manufacturing PMI

On Wednesday (08/04): Building Permits

On Thursday (08/05): Imports ¦ Exports ¦ International Merchandise Trade

On Friday (08/06): Unemployment Rate ¦ Participation Rate ¦ Average Hourly Wages ¦ Net Change in Employment ¦ Ivey Purchasing Managers

On Monday (08/09): Housing Starts

On Tuesday (08/17): Manufacturing Sales ¦ Foreign Portfolio Investment in Canadian Securities ¦ Canadian Portfolio Investment in Foreign Securities

On Wednesday (08/18): BoC Consumer Price Index ¦ Wholesale Sales Consumer Price Index

On Thursday (08/19): ADP Employment ¦ Employment Insurance Beneficiaries Change

On Friday (08/20); Retail Sales

On Monday (08/30): Current Account

On Tuesday (08/31): Raw Material Price Index ¦ Gross Domestic Product Annualized ¦ Industrial Product Price

CNY

On Monday (08/02): Caixin Manufacturing PMI

On Wednesday (08/04): Caixin Services PMI

On Saturday (08/07): Exports ¦ Imports ¦ Trade Balance

On Monday (08/09): Consumer Price Index ¦ Producer Price Index ¦

On Monday (08/10): FDI - Foreign Direct Investment

On Monday (08/16): House Price Index ¦ NBS Press Conference ¦ Industrial Production ¦ Retail Sales

On Tuesday (08/31): Non-Manufacturing PMI ¦ NBS Manufacturing PMI

MXN

On Monday (08/02): Remittance Total ¦ Central Bank Economist Survey ¦ Markit Mexico PMI ¦ IMEF Manufacturing Index

On Tuesday (08/03): Leading Indicators ¦ Consumer Confidence

On Wednesday (08/04):Vehicle Domestic Sales

On Thursday (08/05): Citibanamex Survey Economists

On Friday (08/06): Gross Fixed Investment ¦ Vehicle Exports ¦ Vehicle Production

On Monday (08/09): Consumer Price Index ¦ Bi-weekly CPI

On Tuesday (08/10): Nominal Wages

On Wednesday (08/11): Industrial Production ¦ Manufacturing Production

On Thursday (08/12): Formal Job Creation Total ¦ Overnight Rate

On Monday (08/23): Retail Sales

On Tuesday (08/24): Bi-weekly CPI

On Wednesday (08/25): Gross Domestic Product ¦ Economic Activity ¦ Current Account Balance

On Thursday (08/26): Unemployment Rate ¦ Central Bank Monetary Policy Minutes

On Friday (08/27): Trade Balance ¦ BBG Mexico Survey

On Monday (08/30): Budget Balance

On Tuesday (08/31): Net Outstanding Loans ¦ International Reserves ¦ Central Bank Inflation Report

BRL

On Monday (08/02): Markit Brazil Manufacturing PMI ¦ Trade Balance ¦ Imports ¦ Exports

On Tuesday (08/03): FIPE Consumer Price Index ¦ Industrial Production ¦ Vehicle Sales

On Wednesday (08/04): Markit Brazil PMI Composite ¦ Markit Brazil PMI Services ¦ Selic Rate

On Friday (08/06): Vehicle Sales ¦ Vehicle Production ¦ Vehicle Exports

On Monday (08/09): FGV Inflation Report ¦

On Tuesday (08/10): FGV Consumer Price Index ¦ IBGE Inflation Report IPCA

On Wednesday (08/11): Retail Sales

On Thursday (08/12): IBGE Services Sector Volume

On Friday (08/13): Economic Activity

On Monday (08/16): FGV Consumer Price Index IPCs

On Friday (08/20): Tax Collections

On Wednesday (08/25): FGV Consumer Confidence ¦ Current Account Balance ¦ Foreign Direct Investment

On Thursday (08/26): FGV Construction Costs

On Friday (08/27): PPI Manufacturing ¦ Personal Loan Default Rate ¦ Total Outstanding Loans BBG Brazil Economic Survey ¦ Federal Total Debt ¦ Central Government Budget

On Monday (08/30): FGV Inflation IGPM

On Tuesday (08/31): National Unemployment Rate ¦ Primary budget Balance ¦ Nominal Balance Rate ¦ Net Debt % GDP