Fixed vs Floating Rates: Key Differences & Risk Management Strategies

Fixed vs floating rates determine how interest costs change over time and directly impact cash flows, profitability, and investment returns. For corporates and investment funds managing interest rate risk, choosing between fixed and floating rate exposure is critical to balancing cost certainty with market flexibility.

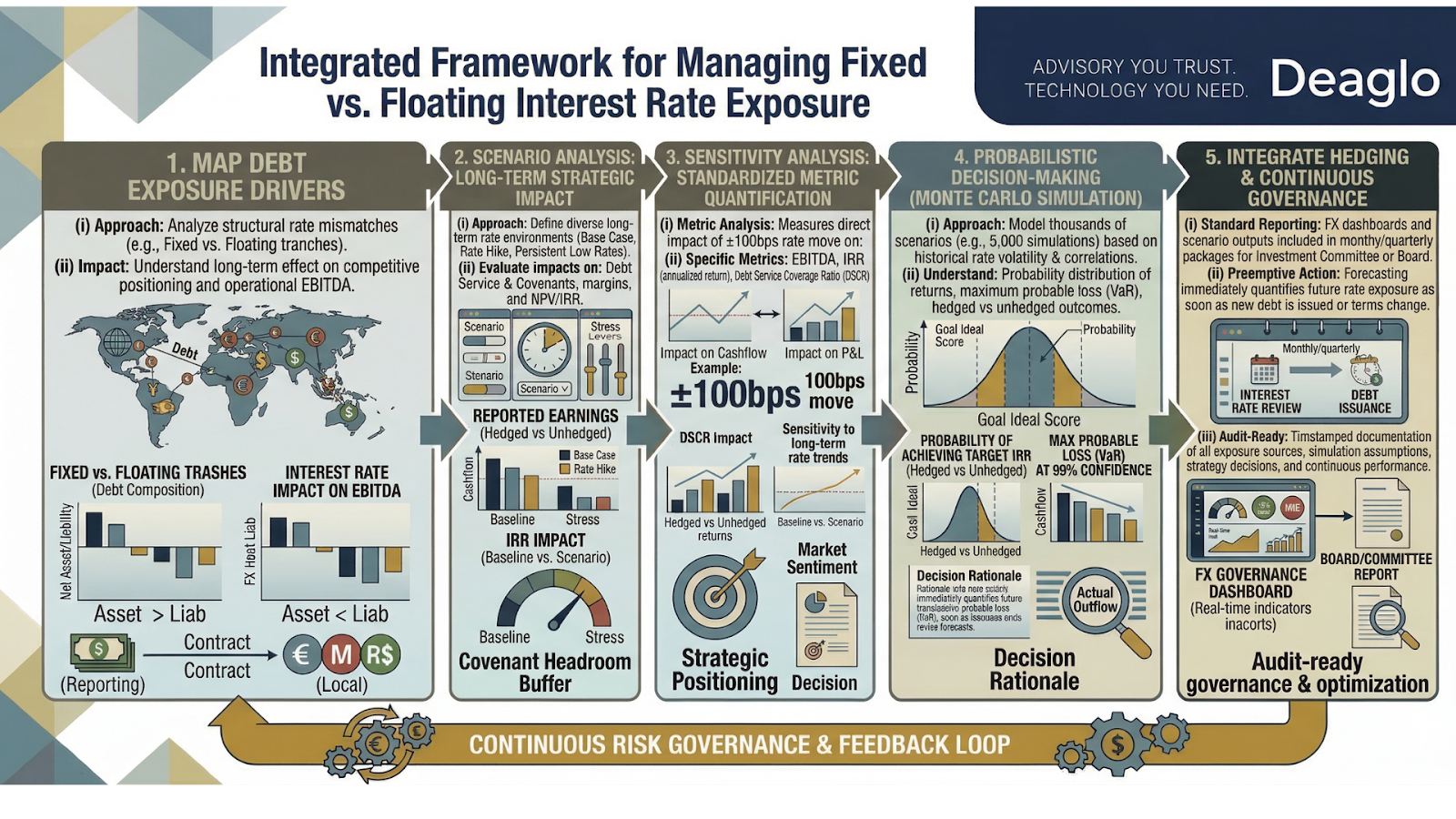

.png)

What Are Fixed vs Floating Rates?

Fixed vs floating rates refer to two types of interest rate structures used in loans, debt instruments, and investments:

- Fixed rates remain constant over the life of the instrument

- Floating rates (or variable rates) change periodically based on benchmark rates such as SOFR, LIBOR (legacy), or central bank rates

Fixed rates provide certainty, while floating rates provide flexibility but introduce variability.

Why Fixed vs Floating Rate Exposure Matters

Choosing between fixed vs floating rates is a critical component of interest rate risk management for both corporates and investment funds operating across global markets. The structure of interest rates directly impacts cash flows, cost of capital, and investment returns, making it a key strategic decision.

For Corporates

Corporates use debt financing for operations, expansion, and acquisitions, creating exposure to interest rate movements.

- Fixed-rate debt provides predictable interest expenses, supporting stable cash flow and budgeting

- Floating-rate debt introduces variability in borrowing costs, linked to benchmark rates such as SOFR

Impact on Corporates:

Interest rate movements can lead to:

- Changes in cost of capital

- Volatility in cash flow and liquidity planning

Pressure on profitability and operating margins

This is particularly relevant for US corporates and global businesses exposed to shifting interest rate cycles.

For Investment Funds

Investment funds, including private equity, private credit, and infrastructure funds, structure financing at both the fund and portfolio company levels, creating exposure to fixed vs floating rate dynamics.

- Floating-rate debt is commonly used in leveraged transactions, linking interest costs to benchmark rates such as SOFR

Changes in interest rates directly affect financing costs, cash flows, and asset performance

Impact on Investment Funds:

Interest rate movements can lead to:

- Variability in cash flows from portfolio companies

- Changes in valuation and exit multiples

IRR sensitivity due to shifting financing costs - Impact on investor distributions and overall fund performance

This is particularly important for funds investing across North America, Europe, and emerging markets, where rate cycles can significantly influence deal outcomes.

Types of FX Cashflow Risk

FX cashflow risk arises from multiple sources across a company’s operations and investment lifecycle. For corporates and investment funds operating in global markets, exposures can stem from foreign currency revenues, costs, financing obligations, and investment cash flows.

Each type of exposure affects cash flow differently, ranging from export inflows and import payments to debt servicing and dividend distributions. Understanding these components is critical for identifying where currency risk exists and applying targeted FX risk management strategies.

For cross-border businesses and investors, mapping these exposure types enables better cash flow planning, hedging decisions, and financial stability across different currency environments.

Real-World Examples of Fixed vs Floating Rate Exposure

Fixed vs floating rate exposure is best understood through real-world scenarios where interest rate movements directly affect borrowing costs, cash flows, and investment returns for corporates and investment funds.

Corporate Example: Impact on Interest Expense

A US-based corporate has a $100 million loan and is evaluating fixed versus floating rate exposure:

- Fixed rate: 5% → $5 million annual interest cost

- Floating rate: SOFR (3%) + 2% → 5% initial interest cost

If interest rates rise:

- SOFR increases to 5% → total floating rate = 7%

- Annual interest expense rises to $7 million

Impact on Corporates:

- $2 million increase in interest expense

- Reduced profitability and operating margins

- Increased pressure on cash flow and liquidity

Key Insight: Floating-rate exposure introduces variability in borrowing costs, making interest rate risk management critical for US corporates and global businesses operating in rising rate environments.

Fund Example: Impact on Returns and IRR

A private equity fund finances an acquisition using floating-rate debt:

- Initial financing cost: 6%

- Interest rates increase → cost rises to 8%

Impact on Investment Funds:

- Lower free cash flow generated by the portfolio company

- Reduced IRR and investment returns

- Increased pressure on exit valuation and deal performance

Key Insight: For funds investing across North America, Europe, and emerging markets, rising interest rates can materially reduce returns, even when underlying asset performance remains strong.

Types of Interest Rate Exposure

Interest rate exposure can be categorized based on how changes in interest rates impact cash flows, borrowing costs, and investment returns. For corporates and investment funds operating across global markets, understanding these exposure types is essential for effective interest rate risk management.

How to Measure Fixed vs Floating Rate Exposure

Measuring fixed vs floating rate exposure is a critical part of interest rate risk management for corporates and investment funds operating across global markets. Because interest rate movements can significantly impact cash flows, borrowing costs, and investment returns, organizations must rely on forward-looking analysis to quantify their exposure.

Key Approaches

- Sensitivity analysis: Measures how changes in interest rates impact interest expense, cash flows, and profitability

- Scenario analysis: Evaluates outcomes under different rate environments, such as rising or falling interest rate cycles

- Cash flow modeling: Assesses the effect of rate changes on liquidity, debt servicing, and investment returns

- Stress testing: Identifies downside risk in extreme or rapidly changing interest rate conditions

These methods enable corporates and investment funds to quantify fixed and floating rate exposure, assess risk across different market environments, and make proactive financing and investment decisions.

Strategies to Manage Fixed vs Floating Rate Exposure

Managing fixed vs floating rate exposure requires a combination of hedging strategies and capital structure decisions to balance risk and flexibility. Corporates and investment funds can use tools such as interest rate swaps, caps, and collars, alongside optimizing their mix of fixed and floating debt, to control exposure to changing rate environments.

By incorporating duration management and scenario-based planning, organizations can align financing structures with cash flow needs and investment objectives. This approach enables more stable borrowing costs, improved liquidity planning, and optimized returns across different interest rate cycles.

The Role of Technology in Interest Rate Risk Management

Modern interest rate risk management requires more than static analysis—it depends on real-time analytics and forward-looking scenario modeling. For corporates and investment funds operating across global markets, technology enables a structured approach to managing fixed vs floating rate exposure and navigating changing rate environments.

Key capabilities include:

- A centralized view of debt and interest rate exposure across entities and portfolios

Real-time tracking of benchmark rate changes (e.g., SOFR, central bank rates) - Scenario simulation to assess the impact of rate movements on cash flows, interest expense, and IRR

- Strategy evaluation across different interest rate environments

By leveraging technology, organizations can move from reactive rate monitoring to proactive, data-driven interest rate risk management, improving financial planning and decision-making.

Deaglo Intelligence: Managing Fixed vs Floating Rate Exposure

Deaglo Intelligence enables corporates and investment funds to effectively manage fixed vs floating rate exposure through a unified, analytics-driven platform.

With Deaglo Intelligence, organizations can:

- Quantify fixed and floating rate exposure across portfolios and financing structures

- Simulate interest rate impacts on:

- Cash flows

- Interest expense

- Internal Rate of Return (IRR)

- Cash flows

- Compare hedging strategies using real pricing logic, not static assumptions

- Replace fragmented spreadsheets with a centralized decision platform

From reactive rate management to data-driven, forward-looking decision-making, enabling better control over borrowing costs, cash flow stability, and investment performance.

Best Practices for Managing Interest Rate Exposure

Managing interest rate exposure requires a strategic and forward-looking approach. By aligning the fixed vs floating rate mix with business and investment objectives, and using scenario analysis to anticipate changing rate environments, corporates and investment funds can better control borrowing costs and cash flow variability.

Continuous monitoring, integrated hedging strategies, and technology-driven analytics enable scalable, data-driven decision-making—helping organizations stabilize returns and optimize performance across interest rate cycles.

Conclusion

Fixed vs floating rates are a fundamental component of interest rate risk management for both corporates and investment funds operating across global markets. The choice between fixed and floating rate exposure directly influences cash flows, cost of capital, and investment returns across different interest rate cycles.

Organizations that adopt structured, data-driven, and forward-looking approaches to managing interest rate exposure will be better positioned to:

- Stabilize interest expenses in volatile rate environments

- Protect cash flows and operating margins

- Optimize returns across rising and falling rate cycles

- Make confident financing and investment decisions

As interest rate volatility continues to shape global markets, effective management of fixed vs floating rate exposure is essential for achieving financial stability and long-term performance.