.png)

FX Risk in Private Credit: How Funds Can Protect Returns Across Borders

FX risk in private credit arises when a fund lends in a currency that differs from its base currency or its investors' reporting currency. Unlike public fixed income, private credit loans are illiquid, long-dated, and often lack the derivatives market depth needed for straightforward hedging — making currency exposure both harder to detect and costlier to manage.

Why FX Risk Is Uniquely Complex in Private Credit

Private credit fund managers face a distinct set of FX challenges not present in public markets. Four structural factors make the problem harder — and the stakes higher.

1. Long-Dated, Illiquid Loan Structures

Private loans typically run 3–7 years with limited secondary market activity. Hedging instruments — primarily FX forwards and cross-currency swaps — must be rolled periodically, creating rollover risk and basis risk between the hedging instrument and the underlying loan.

2. Uncertain Cash Flow Timing

Unlike public bonds with defined coupon schedules, private credit cash flows can be PIK (payment-in-kind), deferred, or subject to covenant renegotiation. This makes it nearly impossible to precisely match the notional and timing of a hedge to the underlying loan, leaving funds exposed to residual currency mismatches.

3. Multi-Currency Loan Books

Direct lending funds operating across Europe, North America, and Asia-Pacific often hold loans in GBP, EUR, USD, SEK, and NOK simultaneously. Managing FX exposure at a portfolio level requires robust treasury systems and a clearly defined hedging policy.

4. Investor Currency Preferences

Limited partners increasingly request currency-specific share classes — GBP-hedged, EUR-hedged, USD unhedged. Structuring, pricing, and managing these share classes adds a layer of operational complexity to FX risk management.

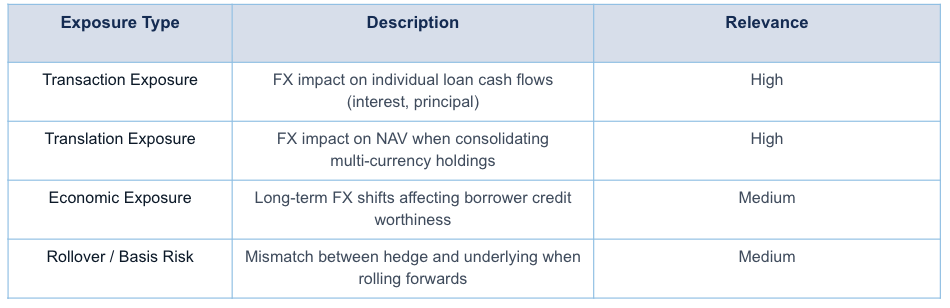

Types of FX Exposure in Private Credit Portfolios

How Private Credit Funds Measure FX Risk

Accurate measurement is the foundation of effective hedging. Best-practice private credit managers apply a multi-layered analytical framework before designing a hedging programme.

.png)

FX Hedging Strategies for Private Credit Funds

1. Rolling FX Forwards

The most common hedging instrument for private credit. The fund enters a forward contract to sell the foreign currency at a fixed rate on a set date — typically 3 or 6 months forward — then rolls the contract at maturity.

2. Cross-Currency Basis Swaps

Used for longer-duration hedges aligned with loan maturities. The fund swaps principal and interest cash flows in one currency for equivalent flows in another.

3. Currency Options

Preferred when cash flow timing is highly uncertain. Options provide the right — but not the obligation — to convert at a fixed rate.

4. Natural Hedging

Structuring liabilities (fund-level borrowing facilities) in the same currency as the loans. A EUR-denominated subscription facility funding EUR loans creates a natural offset.

.png)

The Carry Problem: FX Hedging Cost in Private Credit

One of the most material issues for private credit managers is hedging carry cost — the interest rate differential between currency pairs that determines the cost or benefit of a forward hedge.

For a GBP-based fund hedging USD loan exposure back to GBP, if US interest rates are higher than UK rates, the forward points are negative — meaning the fund pays away part of its USD yield to maintain the hedge. In a high-rate environment, this can cost 100–250 basis points per annum, materially compressing net returns.

Fund managers must communicate hedging costs transparently to LPs and model them into projected net returns. Headline USD yields in private credit may look attractive; the GBP-hedged equivalent will be meaningfully lower.

Building an FX Risk Policy for Private Credit Funds

A well-governed FX risk framework should be formally documented and approved at board or investment committee level. It must define:

.png)

Regulatory and Reporting Considerations

Private credit funds operating under AIFMD in the EU, or FCA rules in the UK, must disclose FX risk as a material risk factor in investor documents and annual reports. SFDR reporting may also require currency-disaggregated performance attribution for funds with sustainability characteristics.

Managers should ensure their fund administrator and prime broker infrastructure can support multi-currency NAV calculations, hedged share class accounting, and real-time FX exposure reporting.