.png)

FX Risk in Private Equity: Managing Currency Exposure Across the Investment Lifecycle

From deal origination to LP distribution, FX risk touches every stage of a PE fund's life. Here's how top managers control it.

FX risk in private equity is the exposure that arises when a fund invests in companies or assets operating in a currency different from the fund's base or investors' reporting currencies. Private equity investments are held for years , typically 5 to 10 giving currency movements significant time to compound and materially alter both the headline return multiple and the IRR delivered to investors, independent of operational performance.

Why FX Risk Is Structurally Different in Private Equity

Private equity's long hold periods, illiquidity, and complex ownership structures make FX risk management fundamentally different from public equity or fixed income. Four structural factors define the challenge.

1. Long Hold Periods Amplify Currency Drift

Holding an investment for 7 years means currency moves compound over time. A 15% EUR depreciation against USD over a hold period doesn't just affect exit proceeds — it flows through interim NAV reporting, DPI metrics, and LP performance expectations throughout the fund's life.

2. Operating Currency ≠ Reporting Currency

Portfolio companies have their own functional currencies driven by where they earn and spend. A PE-owned company with EUR revenues inside a USD-reporting fund creates a permanent translation exposure that must be managed at the fund level throughout the hold period.

3. Illiquidity Limits Hedging Precision

You cannot perfectly hedge an asset you cannot sell. Exit timing in PE is discretionary, driven by market conditions and buyer appetite. Hedging instruments with defined maturities must be rolled — creating rollover risk — or sized conservatively to account for exit uncertainty.

4. Capital Calls and Distributions Create Transaction FX Risk

When a USD fund calls capital from EUR-denominated LPs to fund a GBP acquisition, three currencies interact in a single transaction. Each LP contribution, deal funding, and exit distribution creates a discrete FX transaction that must be actively managed.

The Three Layers of FX Risk in a PE Fund

Understanding exactly where FX risk lives in the PE fund structure is essential before designing a hedging approach.

.png)

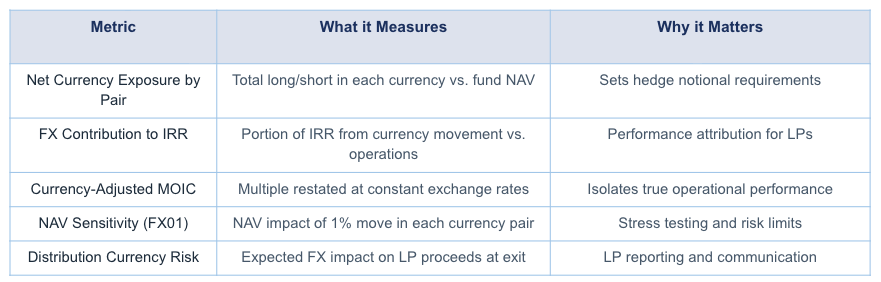

Quantifying FX Exposure in Private Equity Portfolios

FX Hedging Approaches in Private Equity

PE fund managers have a narrower toolkit than public fund managers, given the illiquid and long-dated nature of investments. Each approach represents a deliberate strategic choice — not a default.

1. Deliberate Unhedged Exposure

Many PE funds — particularly buyout and venture funds — take an explicit decision not to hedge, citing high costs, exit timing uncertainty, and the view that operational value creation should dominate currency effects over long hold periods. This is a legitimate strategy, but it must be an explicit, communicated policy, not a default.

2. Deal-Level Hedging at Entry

At acquisition, the fund enters an FX forward or option to fix the rate used to convert the purchase price from the deal currency to the fund base currency. This eliminates transaction FX risk on entry but does not address ongoing NAV translation exposure during the hold period.

3. NAV-Level FX Overlay

The fund maintains a rolling FX hedge — typically using FX forwards — sized to cover a defined percentage of the aggregate foreign currency NAV. The overlay is rebalanced quarterly as valuations change. This approach requires a centralised treasury function and active portfolio monitoring.

4. Portfolio Company-Level Hedging

The PE sponsor directs portfolio companies to implement their own FX hedging programmes, particularly for operationally significant currency mismatches. This is common in large-cap buyouts but less practical for smaller portfolio companies without treasury infrastructure.

5. Currency-Hedged LP Share Classes

The fund creates currency-specific share classes delivering returns in a designated currency to LPs. The fund runs the hedging centrally and allocates costs to the relevant share class NAV. Increasingly expected by institutional LPs in EUR, GBP, and JPY.

FX Risk at the Portfolio Company Level

A PE sponsor's value creation agenda must account for FX risk at the portfolio company level from day one. Due diligence and the first 100 days should address

FX Risk and Fund Performance Reporting

LPs increasingly demand currency-disaggregated performance reporting. Failing to provide it creates friction in LP relationships and can mask whether returns are driven by manager skill or currency movements.

Best practice includes currency-adjusted IRR and MOIC showing performance with and without FX effects, an FX attribution in the NAV bridge separating translation effects from operational value changes, and for funds with hedged share classes, a transparent presentation of hedging cost and its impact on distributions.