__________________________________________________________________________________

Hello, hola and olá international investment enthusiasts and welcome to edition #4 of R&D.

A new workout plan of smart economic exercise has got the Brazilian real and Colombian peso looking pretty ripped right now, even more so when volatility in the US has left the dollar struggling to even do those up-against-the-wall push ups that your Grandparents do.

But offshore investors aren’t convinced. They’ve been catfished before by hunky LATAM currencies so are understandably seeking comfort in the admittedly weedy arms of US funds. This month we’re looking at what forward thinking fund managers are doing to fix that.

But first, to all of human history.

__________________________________________________________________________________

What does the history of safe haven currencies tell us about today’s economic shifts?

Athenian drachma. Roman denarius. Spanish reals. British Sterling. Safe Haven Currencies all of them. Until they weren’t, of course.

When turmoil hits financial markets, investors scurry off for a place to hide, seeking to preserve their capital as asset prices are falling. This is where safe haven currencies, the US dollar, Swiss franc and Japanese yen, come in.

But what happens when the safe havens stop being so safe? And what does the decline of past safe havens tell us about the future of today’s?

Find out in The History and Future of Safe Haven Currencies.

__________________________________________________________________________________

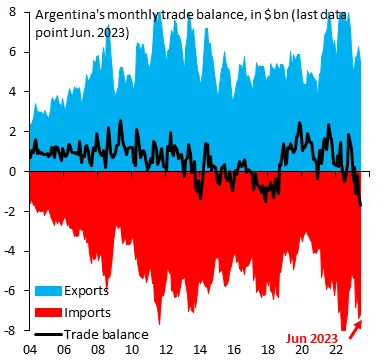

Charted Territory: Does Argentina need dollarization or a recession?

Source: Robin Brooks, IIF, via Twitter

Argentinian populist Presidential candidate (and sex coach) Javier Milei has said dollarization is the balm to his country’s economic woes. But Robin Brooks, Chief Economist at the Institute of International Finance, thinks this chart shows that’s crazy talk. Head of FX Risk Management at Deaglo, Matheus Zani, digs a little deeper:

Unless there is a rebound in exports due to a successful winter harvest and the selling off of existing inventories, the year is likely to conclude with a deficit. This deficit could solidify currency losses amounting to approximately US$7 billion for the year 2023, attributable to the trade balance.

What Argentina requires is the advancement of growth-oriented fiscal consolidation, coupled with a rigorous monetary policy and a streamlined foreign exchange system. These actions remain essential for effectively controlling the rise in domestic demand, improving the trade balance, restoring in

ternational reserves, regaining access to markets, and ensuring the durability of fiscal and external debt sustainability. Furthermore, it is imperative to introduce structural reforms that bolster Argentina's export capabilities and encourage the inflow of foreign direct investment.

__________________________________________________________________________________

Around the World in Headlines

We’ll start this month’s roundup in the US where former President Donald J Trump was indicted (again) for his attempts to overthrow the 2020 Presidential election, a feat he repeated again at the end of the month. Talking of dinosaurs, over in Peru, scientists examining the fossilized bones of an ancient whale declared it the heaviest animal to have ever existed, much to the relief of the current record holder, the blue whale, which had been feeling insecure about the title for millenia. In Pakistan, Imran Khan, the former Prime Minister and Cricket sensation was ‘locked for three’ for illegally selling state gifts, while all over the planet it continues to be far, far too hot with deadly wildfires, heat waves and natural disasters wreaking havoc the world over.

With planet earth becoming less hospitable by the hour, the Russians tried and failed to land on the moon (the first of two notable air crashes this month that the Russian state may or may not have been involved in), while the Indians made it to the much less touristy southern side and Richard Branson’s Virgin Galactic flew a group of millionaires and competition winners up to the outer edges of our atmosphere so they could watch the world burn from a different angle.

Featured: The Art of the Real 🇧🇷

The dollar is down, the Brazilian real and Colombian peso is up. This should be a golden age for private funds in Latin America. Despite this, many offshore investors are still wary of the impact currency volatility can have on returns, retreating instead to the perceived comfort of domestic funds and mature markets. This isn’t without good reason, says Matheus Zani, Head of FX Risk Management at Deaglo. “It’s not that fund managers in emerging markets aren’t able to deliver 20 or 30% returns on their investments, it’s that when they’re translated back into dollars or euros, the returns are significantly less. To stay competitive globally, emerging market managers must deliver similar or higher returns to attract investment.”

This is echoed by Vagner Perez, Partner at Reinvest, a global-focused firm based in the US. “In Latin America, General Partners (GPs) simply don't address the issue. Either because it's too complicated, too expensive, or too cumbersome. Or they believe that LPs are mature enough to understand the effects of currency, and therefore they should be hedging in themselves."

But, in an attempt to catch the eye of offshore investors, some fund managers across the continent are bucking the trend. The main goal is to stay attractive to overseas LPs but there are additional benefits, says Perez. In emerging markets, “executing hedging is not common practice among this type of asset class. There will definitely be a competitive advantage for any firm that can do it.” It also opens up more opportunities for investment in a wider geography of funds and companies, especially those that have previously been deemed too risky. “For example, Africa has been getting a lot of attention from investors. But African currencies, as in Latin America, due to political turmoil etc, are volatile,” he explains. Hedging allows investors to “lower their risk perception” and take advantage of all the “interesting opportunities and potential” in the region.

Hear more from Perez and Zani in LATAM VC and PE funds leading the way in emerging market FX hedging.

__________________________________________________________________________________

‘Raise and Deploy: The International Investing Podcast’ Episode 4 is now live!

This week, we spoke to Jive’s Managing Partner, Marcelo Martins, on how he broke into global investment management and successfully raised and deployed close to a billion dollars across Brazil. Marcelo shares his insights on investing into distressed debt, challenges raising money from international LPs, and how Jive accounts for the currency risk affecting their investors.

__________________________________________________________________________________