.png)

The Death of the Gold Hedge?

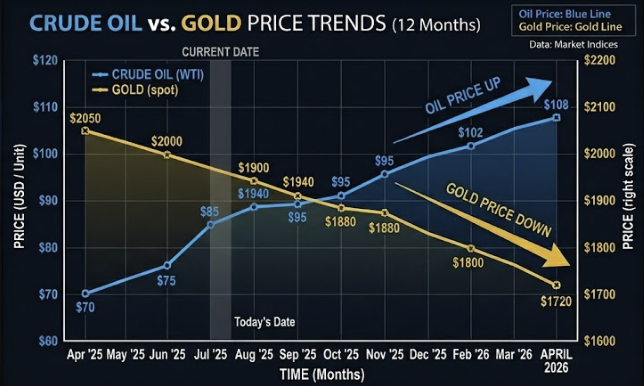

For decades, the "Geopolitical Playbook" was simple: when tensions escalate in the Middle East and oil prices spike, you buy Gold. However, the Q1-Q2 2026 market cycle has shredded this script. Despite Brent crude surging to $126/bbl and regional instability reaching a decade-high, Gold has retreated by 8% year-to-date.

We are currently witnessing the "Oil-Shock Paradox." This edition explores why the US Dollar has cannibalized Gold’s safe-haven status and what it means for corporate treasury and fund positioning over the next 3 to 6 months.

The Mechanics of the Paradox

Historically, Gold serves as a hedge against two things: Geopolitical risk and Inflation. Both are present today. So why the sell-off?

1. The Yield Gravity Well

The current oil shock is inherently inflationary, which has forced the Federal Reserve to signal a "higher-for-longer" stance, pushing the US 10-Year Treasury yield toward the 5.0% mark.

- The Opportunity Cost: In a world where risk-free US Treasuries offer a 5% nominal yield, the "zero-yield" nature of physical Gold becomes an expensive luxury.

- The Result: Institutional capital is rotating out of non-yielding bullion and into high-carry USD instruments.

2. USD as the "Ultimate Safe Haven"

In 2026, the US has solidified its position as a net energy exporter. This has fundamentally changed the USD's reaction to oil shocks.

- The Dynamic: Higher oil prices now improve the US terms of trade while devastating the trade balances of the Eurozone and Japan.

- The Shift: Investors are no longer fleeing to Gold for safety; they are fleeing to the Greenback. The USD is now a "Dual-Threat" asset—offering both safe-haven protection and high-yield momentum.

Corporate & Fund Implications

For Corporate Treasurers:

- USD Dominance: Expect continued upward pressure on the USD. For those with EUR or JPY denominated costs and USD revenue, the "natural hedge" is strengthening, but importers should consider locking in forward rates now before the energy-driven divergence widens.

- Inventory Costs: With Gold losing its luster as a macro hedge, using precious metals to offset general commodity volatility is proving ineffective. Focus on direct energy derivatives or USD-based hedges instead.

For Fund Managers:

- The Carry vs. Chaos Trade: The "Oil-Shock Paradox" suggests that "Carry" is currently beating "Chaos." Long USD/JPY or USD/EUR remains the preferred expression of the current geopolitical climate over long Gold positions.

- Liquidity Preference: During this period of volatility, liquidity is king. The depth of the US Treasury market is providing a more attractive "exit door" than the relatively thin physical gold market.

The Road Ahead: Will the Trend Reverse?

The "Death of Gold" may be exaggerated, but its rebirth requires a specific catalyst: Supply Stabilization.

As soon as oil supply chains normalize—or demand destruction kicks in—inflationary pressure will cool. This will lead to:

- A "pivot" or softening in Fed rhetoric.

- A compression of US Treasury yields.

- A weakening of the USD as the "energy premium" fades.

The Strategy: We anticipate Gold will remain under pressure for the next 90 days. However, as we approach Q4 2026, we look for a "Mean Reversion" play. Once the 10-year yield stabilizes and begins to retreat, Gold’s inverse correlation will likely return, making current levels an attractive long-term entry point for those with an 18-month horizon.

Conclusion: Navigating the New Defensive Hierarchy

The traditional correlation between geopolitical strife and Gold prices has not just weakened; it has been fundamentally rewritten by the energy-driven yield surge of 2026. For corporates and funds, the takeaway is clear: the US Dollar is currently the only asset providing both the liquidity of a safe haven and the "buffer" of a high-yielding instrument.

As we navigate the next 3 to 6 months, we advise a shift in defensive philosophy. While Gold has historically been the "ultimate insurance policy," in a regime of $120+ oil and 5% Treasury yields, USD liquidity is the superior hedge. The "Oil-Shock Paradox" will likely persist until we see a definitive peak in energy prices or a pivot in Federal Reserve rhetoric. Until then, we remain focused on high-carry currencies and USD-denominated cash equivalents to weather the volatility.

Key Watchpoints for Q3:

- The $126 Oil Ceiling: Any breach above this level will likely trigger further USD strength and Gold liquidation as "inflation-fighting" rate hikes become a certainty.

- Yield Curve Inversion: Monitor the 2s/10s spread; if the curve steepens alongside rising oil, the pressure on non-yielding assets like Gold will intensify.

We will continue to monitor these shifts as the energy landscape evolves. For a deeper dive into specific hedging structures for your portfolio, please reach out.